Bank of America 2006 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

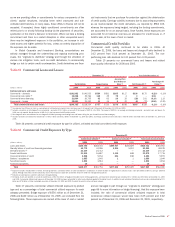

Table 17 Commercial Utilized Criticized Exposure (1,2)

December 31, 2006 December 31, 2005

(Dollars in millions) Amount Percent

(3)

Amount Percent

(3,4)

Commercial – domestic

$5,210 2.41%

$4,954 2.59%

Commercial real estate

815 1.78

723 1.63

Commercial lease financing

504 2.31

611 2.95

Commercial – foreign

582 1.05

797 1.48

Total commercial utilized criticized exposure

$7,111 2.09%

$7,085 2.28%

(1) Criticized exposure corresponds to the Special Mention, Substandard and Doubtful asset categories defined by regulatory authorities.

(2) Exposure includes standby letters of credit, financial guarantees, commercial letters of credit and bankers’ acceptances for which the bank is legally bound to advance funds under prescribed conditions, during a specified

period. Although funds have not been advanced, most of these exposure types are considered utilized for credit risk management purposes.

(3) Ratios are calculated as commercial utilized criticized exposure divided by total commercial utilized exposure for each exposure category.

(4) Commercial – domestic and Total commercial criticized exposure ratios for December 31, 2005 have been reclassified to reflect cash collateral applied to Derivative Assets that are in total commercial utilized credit exposure.

Commercial – Domestic

At December 31, 2006, approximately 80 percent of the commercial—

domestic portfolio was included in Business Lending (business banking,

middle market and large multinational corporate loans and leases) and

Capital Markets and Advisory Services (acquisition and bridge financing),

both within Global Corporate and Investment Banking. Outstanding loans

and leases in Global Corporate and Investment Banking increased $11.6

billion to $130.0 billion at December 31, 2006 compared to

December 31, 2005 driven by organic growth. Nonperforming loans and

leases declined by $45 million to $460 million driven by overall improve-

ments in the portfolio. Net charge-offs were up $72 million from 2005 due

to a lower level of recoveries. Criticized utilized exposure, excluding bridge

exposure, remained essentially flat at $4.6 billion.

The remaining 20 percent of the commercial—domestic portfolio is in

Global Wealth and Investment Management (business-purpose loans for

wealthy individuals) and Global Consumer and Small Business Banking

(business card and small business loans). Outstanding loans and leases

increased $9.8 billion to $32.0 billion at December 31, 2006 compared

to December 31, 2005 driven primarily by growth in Global Consumer and

Small Business Banking. Growth was centered in the business card portfo-

lio, including the addition of MBNA, and the small business portfolio.

Nonperforming loans and leases increased $48 million to $124 million

due to seasoning of the small business portfolio and the addition of

MBNA, both within Global Consumer and Small Business Banking. Loans

past due 90 days or more and still accruing interest increased $153 mil-

lion to $215 million primarily attributable to the business card portfolio.

The increase was driven by the adoption of MBNA collection practices that

have historically led to higher delinquencies but lower losses, the addition

of the MBNA business card portfolio and portfolio seasoning. Net charge-

offs were up $94 million from 2005 due to a $134 million increase in

Global Consumer and Small Business Banking, partially offset by a 2006

credit loss recovery in Global Wealth and Investment Management. The

increase in net charge-offs in Global Consumer and Small Business Bank-

ing was due to the addition of MBNA and seasoning of the small business

and business card portfolios. Criticized utilized exposure increased $265

million to $561 million driven by an increase in the business card portfolio

resulting primarily from the addition of MBNA.

Commercial Real Estate

The commercial real estate portfolio is managed in Business Lending

within Global Corporate and Investment Banking and consists of loans

issued primarily to public and private developers, homebuilders and

commercial real estate firms. Outstanding loans and leases increased

$492 million in 2006 compared to 2005. The increase was driven

by business generated predominantly with existing clients across multiple

property types. Utilized criticized exposure increased $92 million to $815

million driven by a $147 million increase in the utilized criticized loan and

lease portfolio, attributable to the deterioration of a number of relatively

small credits in a variety of property types, the largest of which is resi-

dential. The increase was partially offset by improvements centered in

hotels/motels and multiple use commercial properties.

Table 18 presents outstanding commercial real estate loans by geo-

graphic region and property type diversification, excluding those commer-

cial loans and leases secured by owner-occupied real estate. Commercial

loans and leases secured by owner-occupied real estate are made on the

general creditworthiness of the borrower where real estate is obtained as

additional security and the ultimate repayment of the credit is not depend-

ent on the sale, lease and rental, or refinancing of the real estate. For

purposes of this table, commercial real estate reflects loans dependent on

the sale of the real estate as the primary source of repayment. The

increase in residential property type loans was driven by higher utilizations

in the for-sale housing sector due to increased construction and land cost.

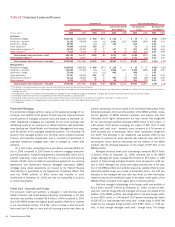

Table 18 Outstanding Commercial Real Estate Loans

December 31

(Dollars in millions) 2006 2005

By Geographic Region (1)

California

$ 7,781

$ 7,615

Northeast

6,368

6,337

Southeast

5,097

4,370

Florida

3,898

4,507

Southwest

3,787

3,658

Midwest

2,271

2,595

Northwest

2,053

2,048

Midsouth

2,006

1,485

Other

870

873

Geographically diversified

(2)

1,549

1,693

Non-U.S.

578

585

Total

$36,258

$35,766

By Property Type

Residential

$ 8,151

$ 7,601

Office buildings

4,823

4,984

Apartments

4,277

4,461

Land and land development

3,956

3,715

Shopping centers/retail

3,955

4,165

Industrial/warehouse

3,247

3,031

Multiple use

1,257

996

Hotels/motels

1,185

790

Resorts

180

183

Other

(3)

5,227

5,840

Total

$36,258

$35,766

(1) Distribution is based on geographic location of collateral. Geographic regions are in the U.S. unless

otherwise noted.

(2) The geographically diversified category is comprised primarily of unsecured outstandings to real estate

investment trusts and national homebuilders whose portfolios of properties span multiple geographic

regions.

(3) Represents loans to borrowers whose primary business is commercial real estate, but the exposure is

not secured by the listed property types.

68

Bank of America 2006