Bank of America 2006 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

2005, we contributed $2.6 billion and $1.1 billion to the Plans, and we

expect to make at least $192 million of contributions during 2007. Debt,

lease and other obligations are more fully discussed in Notes 12 and 13

of the Consolidated Financial Statements.

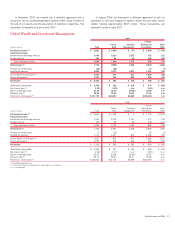

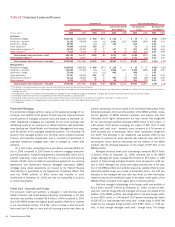

Table 8 presents total long-term debt and other obligations at December 31, 2006.

Table 8 Long-term Debt and Other Obligations (1)

December 31, 2006

(Dollars in millions)

Due in 1 year

or less

Due after 1 year

through 3 years

Due after

3 years through

5 years

Due after

5 years Total

Long-term debt and capital leases

$17,194 $44,962 $20,799 $63,045 $146,000

Purchase obligations

(2)

23,918 22,578 11,234 1,005 58,735

Operating lease obligations

1,375 2,410 1,732 5,951 11,468

Other long-term liabilities

464 676 290 835 2,265

Total

$42,951 $70,626 $34,055 $70,836 $218,468

(1) This table does not include the obligations associated with the Corporation’s Deposits. For more information on Deposits, see Note 11 of the Consolidated Financial Statements.

(2) Obligations that are legally binding agreements whereby we agree to purchase products or services with a specific minimum quantity defined at a fixed, minimum or variable price over a specified period of time are defined as

purchase obligations.

Many of our lending relationships contain funded and unfunded

elements. The funded portion is reflected on our balance sheet. The

unfunded component of these commitments is not recorded on our bal-

ance sheet until a draw is made under the credit facility; however, a

reserve is established for probable losses. These commitments, as well

as guarantees, are more fully discussed in Note 13 of the Consolidated

Financial Statements.

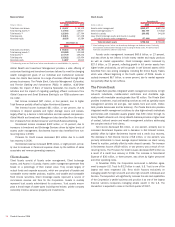

The following table summarizes the total unfunded, or off-balance

sheet, credit extension commitment amounts by expiration date. At

December 31, 2006, charge cards (nonrevolving card lines) to individuals

and government entities guaranteed by the U.S. government in the amount

of $9.6 billion (related outstandings of $193 million) were not included in

credit card line commitments in the table below.

Table 9 Credit Extension Commitments

December 31, 2006

(Dollars in millions)

Expires in 1 year

or less

Expires after

1 year through

3 years

Expires after

3 years through

5 years

Expires after

5 years Total

Loan commitments

(1)

$ 151,604 $60,660 $ 90,988 $ 34,953 $ 338,205

Home equity lines of credit

1,738 1,801 2,742 91,919 98,200

Standby letters of credit and financial guarantees

29,213 10,712 6,744 6,337 53,006

Commercial letters of credit

3,880 180 27 395 4,482

Legally binding commitments

186,435 73,353 100,501 133,604 493,893

Credit card lines

(2)

840,215 13,377 — — 853,592

Total

$1,026,650 $86,730 $100,501 $133,604 $1,347,485

(1) Included at December 31, 2006, are equity commitments of $2.8 billion related to obligations to further fund equity investments.

(2) As part of the MBNA merger, on January 1, 2006, the Corporation acquired $588.4 billion of unused credit card lines.

Managing Risk

Overview

Our management governance structure enables us to manage all major

aspects of our business through an integrated planning and review proc-

ess that includes strategic, financial, associate, customer and risk plan-

ning. We derive much of our revenue from managing risk from customer

transactions for profit. In addition to qualitative factors, we utilize quantita-

tive measures to optimize risk and reward trade offs in order to achieve

growth targets and financial objectives while reducing the variability of

earnings and minimizing unexpected losses. Risk metrics that allow us to

measure performance include economic capital targets, SVA targets and

corporate risk limits. By allocating economic capital to a business unit, we

effectively define that unit’s ability to take on risk. Review and approval of

business plans incorporates approval of economic capital allocation, and

economic capital usage is monitored through financial and risk reporting.

Country, trading, asset allocation and other limits supplement the alloca-

tion of economic capital. These limits are based on an analysis of risk and

reward in each business unit and management is responsible for tracking

and reporting performance measurements as well as any exceptions to

guidelines or limits. Our risk management process continually evaluates

risk and appropriate metrics needed to measure it.

Our business exposes us to the following major risks: strategic, liquid-

ity, credit, market and operational. Strategic Risk is the risk that adverse

business decisions, ineffective or inappropriate business plans or failure

to respond to changes in the competitive environment, business cycles,

customer preferences, product obsolescence, execution and/or other

intrinsic risks of business will impact our ability to meet our objectives.

Liquidity risk is the inability to accommodate liability maturities and

deposit withdrawals, fund asset growth and meet contractual obligations

through unconstrained access to funding at reasonable market rates.

Credit risk is the risk of loss arising from a borrower’s or counterparty’s

inability to meet its obligations. Market risk is the risk that values of

assets and liabilities or revenues will be adversely affected by changes in

market conditions, such as interest rate movements. Operational risk is

the risk of loss resulting from inadequate or failed internal processes,

people and systems or external events. The following sections, Strategic

Risk Management, Liquidity Risk and Capital Management, Credit Risk

Management beginning on page 59, Market Risk Management beginning

on page 75 and Operational Risk Management beginning on page 81,

address in more detail the specific procedures, measures and analyses of

the major categories of risk that we manage.

58

Bank of America 2006