Bank of America 2006 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

-

152

-

153

-

154

-

155

|

|

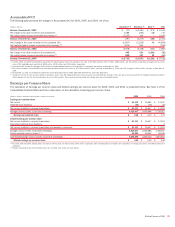

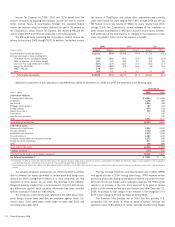

On December 31, 2006, the Corporation adopted SFAS 158 which

requires the recognition of a plan’s over-funded or under-funded status as

an asset or liability with an offsetting adjustment to Accumulated OCI.

SFAS 158 requires the determination of the fair values of a plan’s assets

at a company’s year-end and recognition of actuarial gains and losses,

prior service costs or credits, and transition assets or obligations as a

component of Accumulated OCI. These amounts were previously netted

against the plans’ funded status in the Corporation’s Consolidated Bal-

ance Sheet pursuant to the provisions of SFAS 87. These amounts will be

subsequently recognized as components of net periodic benefit costs.

Further, actuarial gains and losses that arise in subsequent periods that

are not initially recognized as a component of net periodic benefit cost will

be recognized as a component of Accumulated OCI. Those amounts will

subsequently be recognized as a component of net periodic benefit cost

as they are amortized during future periods.

The incremental effects of adopting the provisions of SFAS 158 on

the Corporation’s Consolidated Balance Sheet at December 31, 2006 are

presented in the following table. The adoption of SFAS 158 had no effect

on the Corporation’s Consolidated Statement of Income for the year ended

December 31, 2006, or for any year presented.

(Dollars in millions)

Before

Application of

Statement 158 Adjustments

After

Application of

Statement 158

Other assets

(1)

$ 121,649 $(1,966) $ 119,683

Total assets

1,461,703 (1,966) 1,459,737

Accrued expenses and other liabilities

(2)

42,790 (658) 42,132

Total liabilities

1,325,123 (658) 1,324,465

Accumulated OCI

(3)

(6,403) (1,308) (7,711)

Total shareholders’ equity

136,580 (1,308) 135,272

Total liabilities and shareholders’ equity

1,461,703 (1,966) 1,459,737

(1) Represents adjustments to plans in an asset position of $(1,966) million.

(2) Represents adjustments to plans in a liability position of $301 million, the reversal of the additional minimum liability adjustment of $(190) million and an adjustment to deferred tax liabilities of $(769) million.

(3) Includes employee benefit plan adjustments of $(1,428) million, net of tax, and the reversal of the additional minimum liability adjustment of $120 million, net of tax.

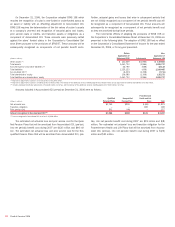

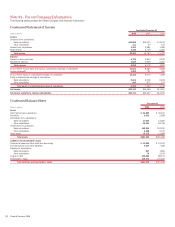

Amounts included in Accumulated OCI (pre-tax) at December 31, 2006 were as follows:

(Dollars in millions)

Qualified

Pension Plans

Nonqualified

Pension Plans

Postretirement

Health and Life

Plans Total

Net actuarial loss

$1,765 $224 $ (68) $1,921

Transition obligation

– – 189 189

Prior service cost

201 (44) – 157

Amount recognized in Accumulated OCI (1)

$ 1,966 $180 $121 $ 2,267

(1) Amount recognized in Accumulated OCI net of tax is $1,428 million.

The estimated net actuarial loss and prior service cost for the Quali-

fied Pension Plans that will be amortized from Accumulated OCI, (pre-tax),

into net periodic benefit cost during 2007 are $130 million and $46 mil-

lion. The estimated net actuarial loss and prior service cost for the Non-

qualified Pension Plans that will be amortized from Accumulated OCI, (pre-

tax), into net periodic benefit cost during 2007 are $19 million and $(8)

million. The estimated net actuarial loss and transition obligation for the

Postretirement Health and Life Plans that will be amortized from Accumu-

lated OCI, (pre-tax), into net periodic benefit cost during 2007 is $(22)

million and $31 million.

138

Bank of America 2006