Bank of America 2006 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

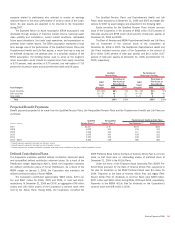

Note 15 – Regulatory Requirements and

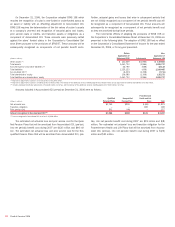

Restrictions

The Board of Governors of the Federal Reserve System (FRB) requires the

Corporation’s banking subsidiaries to maintain reserve balances based on

a percentage of certain deposits. Average daily reserve balances required

by the FRB were $5.6 billion and $6.4 billion for 2006 and 2005. Currency

and coin residing in branches and cash vaults (vault cash) are used to

partially satisfy the reserve requirement. The average daily reserve balan-

ces, in excess of vault cash, held with the FRB amounted to $27 million

and $361 million for 2006 and 2005.

The primary source of funds for cash distributions by the Corporation

to its shareholders is dividends received from its banking subsidiaries

Bank of America, N.A. and FIA Card Services, N.A. Effective June 10,

2006, MBNA America Bank, N.A. was renamed FIA Card Services, N.A.

Additionally, on October 20, 2006, Bank of America, N.A. (USA) merged

into FIA Card Services, N.A. In 2006, Bank of America Corporation

received $16.0 billion in dividends from its banking subsidiaries. In 2007,

Bank of America, N.A. and FIA Card Services, N.A. can declare and pay

dividends to Bank of America Corporation of $11.4 billion and $356 mil-

lion plus an additional amount equal to their net profits for 2007, as

defined by statute, up to the date of any such dividend declaration. The

other subsidiary national banks can initiate aggregate dividend payments

in 2007 of $68 million plus an additional amount equal to their net profits

for 2007, as defined by statute, up to the date of any such dividend decla-

ration. The amount of dividends that each subsidiary bank may declare in

a calendar year without approval by the Office of the Comptroller of the

Currency (OCC) is the subsidiary bank’s net profits for that year combined

with its net retained profits, as defined, for the preceding two years.

The FRB, the OCC and the Federal Deposit Insurance Corporation

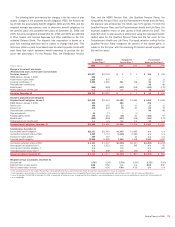

(collectively, the Agencies) have issued regulatory capital guidelines for

U.S. banking organizations. Failure to meet the capital requirements can

initiate certain mandatory and discretionary actions by regulators that

could have a material effect on the Corporation’s financial statements. At

December 31, 2006, the Corporation, Bank of America, N.A. and FIA Card

Services, N.A. were classified as “well-capitalized” under this regulatory

framework. At December 31, 2005, the Corporation, Bank of America N.A.

and Bank of America, N.A. (USA) were also classified as “well-capitalized.”

There have been no conditions or events since December 31, 2006 that

management believes have changed the Corporation’s, Bank of America,

N.A.’s and FIA Card Services, N.A.’s capital classifications.

The regulatory capital guidelines measure capital in relation to the

credit and market risks of both on and off-balance sheet items using vari-

ous risk weights. Under the regulatory capital guidelines, Total Capital

consists of three tiers of capital. Tier 1 Capital includes Common Share-

holders’ Equity, Trust Securities, minority interests and qualifying Preferred

Stock, less Goodwill and other adjustments. Tier 2 Capital consists of

Preferred Stock not qualifying as Tier 1 Capital, mandatory convertible

debt, limited amounts of subordinated debt, other qualifying term debt, the

allowance for credit losses up to 1.25 percent of risk-weighted assets and

other adjustments. Tier 3 Capital includes subordinated debt that is

unsecured, fully paid, has an original maturity of at least two years, is not

redeemable before maturity without prior approval by the FRB and includes

a lock-in clause precluding payment of either interest or principal if the

payment would cause the issuing bank’s risk-based capital ratio to fall or

remain below the required minimum. Tier 3 Capital can only be used to

satisfy the Corporation’s market risk capital requirement and may not be

used to support its credit risk requirement. At December 31, 2006 and

2005, the Corporation had no subordinated debt that qualified as Tier 3

Capital.

Certain corporate sponsored trust companies which issue Trust

Securities are not consolidated under FIN 46R. As a result, the Trust

Securities are not included on our Consolidated Balance Sheet. On

March 1, 2005, the FRB issued Risk-Based Capital Standards: Trust Pre-

ferred Securities and the Definition of Capital (the Final Rule) which allows

Trust Securities to continue to qualify as Tier 1 Capital with revised quanti-

tative limits that would be effective after a five-year transition period. As a

result, Trust Securities are included in Tier 1 Capital.

The FRB’s Final Rule limits restricted core capital elements to 15

percent for internationally active bank holding companies. Internationally

active bank holding companies are those with consolidated assets greater

than $250 billion or on-balance sheet exposure greater than $10 billion. In

addition, the FRB revised the qualitative standards for capital instruments

included in regulatory capital. At December 31, 2006, our restricted core

capital elements comprised 17.3 percent of total core capital elements.

We expect to be fully compliant with the revised limits prior to the

implementation date of March 31, 2009.

To meet minimum, adequately-capitalized regulatory requirements, an

institution must maintain a Tier 1 Capital ratio of four percent and a Total

Capital ratio of eight percent. A well-capitalized institution must generally

maintain capital ratios 200 bps higher than the minimum guidelines. The

risk-based capital rules have been further supplemented by a leverage

ratio, defined as Tier 1 Capital divided by adjusted quarterly average Total

Assets, after certain adjustments. The leverage ratio guidelines establish

a minimum of three percent. Banking organizations must maintain a lever-

age capital ratio of at least five percent to be classified as “well-

capitalized.” As of December 31, 2006, the Corporation was classified as

“well-capitalized” for regulatory purposes, the highest classification.

Net Unrealized Gains (Losses) on AFS Debt Securities, Net Unreal-

ized Gains on AFS Marketable Equity Securities, Net Unrealized Gains

(Losses) on Derivatives, and the impact of SFAS 158 included in Share-

holders’ Equity at December 31, 2006 and 2005, are excluded from the

calculations of Tier 1 Capital and leverage ratios. The Total Capital ratio

excludes all of the above with the exception of up to 45 percent of Net

Unrealized Gains on AFS Marketable Equity Securities.

136

Bank of America 2006