Bank of America 2006 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Noninterest Expense

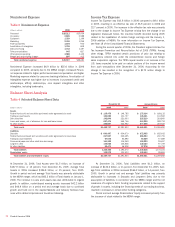

Table 3 Noninterest Expense

(Dollars in millions) 2006 2005

Personnel

$18,211

$15,054

Occupancy

2,826

2,588

Equipment

1,329

1,199

Marketing

2,336

1,255

Professional fees

1,078

930

Amortization of intangibles

1,755

809

Data processing

1,732

1,487

Telecommunications

945

827

Other general operating

4,580

4,120

Merger and restructuring charges

805

412

Total noninterest expense

$35,597

$28,681

Noninterest Expense increased $6.9 billion to $35.6 billion in 2006

compared to 2005, primarily due to the MBNA merger, increased Person-

nel expense related to higher performance-based compensation and higher

Marketing expense related to consumer banking initiatives. Amortization of

Intangibles expense was higher due to increases in purchased credit card

relationships, affinity relationships, core deposit intangibles and other

intangibles, including trademarks.

Income Tax Expense

Income Tax Expense was $10.8 billion in 2006 compared to $8.0 billion

in 2005, resulting in an effective tax rate of 33.9 percent in 2006 and

32.7 percent in 2005. The increase in the effective tax rate was primarily

due to the charge to Income Tax Expense arising from the change in tax

legislation discussed below, the one-time benefit recorded during 2005

related to the repatriation of certain foreign earnings and the January 1,

2006 addition of MBNA. For more information on Income Tax Expense,

see Note 18 of the Consolidated Financial Statements.

During the second quarter of 2006, the President signed into law the

Tax Increase Prevention and Reconciliation Act of 2005 (TIPRA). Among

other things, TIPRA repealed certain provisions of prior law relating to

transactions entered into under the extraterritorial income and foreign

sales corporation regimes. The TIPRA repeal results in an increase in the

U.S. taxes expected to be paid on certain portions of the income earned

from such transactions after December 31, 2006. Accounting for the

change in law resulted in the recognition of a $175 million charge to

Income Tax Expense in 2006.

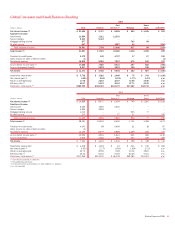

Balance Sheet Analysis

Table 4 Selected Balance Sheet Data

December 31 Average Balance

(Dollars in millions) 2006 2005 2006 2005

Assets

Federal funds sold and securities purchased under agreements to resell

$ 135,478

$ 149,785

$ 175,334

$ 169,132

Trading account assets

153,052

131,707

145,321

133,502

Debt securities

192,846

221,603

225,219

219,843

Loans and leases, net of allowance for loan and lease losses

697,474

565,746

643,259

528,793

All other assets

280,887

222,962

277,548

218,622

Total assets

$1,459,737

$1,291,803

$1,466,681

$1,269,892

Liabilities

Deposits

$ 693,497

$ 634,670

$ 672,995

$ 632,432

Federal funds purchased and securities sold under agreements to repurchase

217,527

240,655

286,903

230,751

Trading account liabilities

67,670

50,890

64,689

57,689

Commercial paper and other short-term borrowings

141,300

116,269

124,229

95,657

Long-term debt

146,000

100,848

130,124

97,709

All other liabilities

58,471

46,938

57,278

55,793

Total liabilities

1,324,465

1,190,270

1,336,218

1,170,031

Shareholders’ equity

135,272

101,533

130,463

99,861

Total liabilities and shareholders’ equity

$1,459,737

$1,291,803

$1,466,681

$1,269,892

At December 31, 2006, Total Assets were $1.5 trillion, an increase of

$167.9 billion, or 13 percent, from December 31, 2005. Average Total

Assets in 2006 increased $196.8 billion, or 15 percent, from 2005.

Growth in period end and average Total Assets was primarily attributable

to the MBNA merger, which had $83.3 billion of Total Assets on January 1,

2006. The increase in Loans and Leases was also attributable to organic

growth. In addition, market-based earning assets increased $42.2 billion

and $46.9 billion on a period end and average basis due to continued

growth and build out in the Capital Markets and Advisory Services busi-

ness within Global Corporate and Investment Banking.

At December 31, 2006, Total Liabilities were $1.3 trillion, an

increase of $134.2 billion, or 11 percent, from December 31, 2005. Aver-

age Total Liabilities in 2006 increased $166.2 billion, or 14 percent, from

2005. Growth in period end and average Total Liabilities was primarily

attributable to increases in Deposits and Long-term Debt, due to the

assumption of liabilities in connection with the MBNA merger and the net

issuances of Long-term Debt. Funding requirements related to the support

of growth in assets, including the financing needs of our trading business,

resulted in increases in certain other funding categories.

Period end and average Shareholders’ Equity increased primarily from

the issuance of stock related to the MBNA merger.

38

Bank of America 2006