Bank of America 2006 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

smaller than the “natural share” we

should expect given the size of our

company. In the retail markets, that

natural share is defined somewhat

by our deposit share in a given geo-

graphic market. Examples of product

markets in which we have plenty of

room to run include mortgage, home

equity and small business lending.

I would add that the geographic

markets in which we have chosen to compete are the fastest

growing in the country, providing more opportunity for us to

grow our business.

While our wealth management business is large and grow-

ing, we have a huge opportunity embedded in our current client

base: clients who qualify for high service levels such as Premier

or Private Banking but who have not yet chosen to take their

relationship with us to that level. Outside our existing client

base, the opportunity is even larger.

One of the most important moves we made in 2006 to

pursue growth in the wealth management business was our

agreement to acquire U.S. Trust for $3.3 billion, a transaction

we expect to close in the third quarter of 2007. As one of the

oldest, largest and most respected private banks in the coun-

try, U.S. Trust will combine with The Private Bank of Bank

of America to create the leading private bank in the country.

Clients of both our organizations will benefit from a more

comprehensive set of products and services, and access to the

broadest financial services distribution network in America.

U.S. Trust brings to this partnership one of the strongest brands

in the industry, which we are looking very hard at retaining.

By focusing on these and other opportunities, we aim

to generate strong, consistent organic growth across all

our businesses.

Second: Is Bank of America’s growth to be fueled primarily

by acquisitions or by winning and expanding customer

relationships? Our answer: Wrong question.

A better question would be whether Bank of America is

capable of generating revenue and earnings growth organically

and through acquisition. And our answer is an emphatic “yes.”

The strongest companies are those that have the

resources, knowledge, judgment and skills to pursue multiple

paths to growth. For the past nine years, we have focused

primarily on generating organic growth through process

improvement, increasing customer satisfaction and product

innovation. At the same time, we have taken advantage of

select opportunities presented to us to enter new markets.

These acquisitions — Fleet, National Processing Inc., MBNA

and U.S. Trust, scheduled to close in 2007 — add customers,

capabilities and great new opportunities to grow the business.

Today, there is nothing more important than executing well

on our current organic growth strategy. Every other opportu-

nity pales in comparison to the opportunity we have with our

customers and prospects in our current markets. And yet, our

ability to pursue multiple paths to growth is a great strength

Bank of America 2006 5

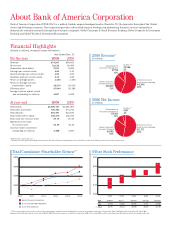

’06

Net

Income

’05

’04 $13 . 9

$16 . 5

$21 . 1

CREATING

SHAREHOLDER

VALUE

Total annualized

shareholder return

of 20% since

December 31,

2000

(in billions)