Bank of America 2006 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Note 6 – Outstanding Loans and Leases

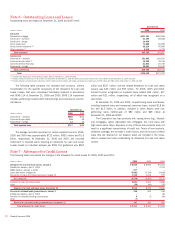

Outstanding loans and leases at December 31, 2006 and 2005 were:

December 31

(Dollars in millions) 2006 2005

Consumer

Residential mortgage

$241,181

$182,596

Credit card – domestic

61,195

58,548

Credit card – foreign

10,999

–

Home equity lines

74,888

62,098

Direct/Indirect consumer

(1)

68,224

45,490

Other consumer

(2)

9,218

6,725

Total consumer

465,705

355,457

Commercial

Commercial – domestic

161,982

140,533

Commercial real estate

(3)

36,258

35,766

Commercial lease financing

21,864

20,705

Commercial – foreign

20,681

21,330

Total commercial

240,785

218,334

Total

$706,490

$573,791

(1) Includes home equity loans of $12.8 billion and $8.1 billion at December 31, 2006 and 2005.

(2) Includes foreign consumer loans of $6.2 billion and $3.8 billion at December 31, 2006 and 2005 and consumer finance loans of $2.8 billion for both December 31, 2006 and 2005.

(3) Includes domestic commercial real estate loans of $35.7 billion and $35.2 billion, and foreign commercial real estate loans of $578 million and $585 million at December 31, 2006 and 2005.

The following table presents the recorded loan amounts, without

consideration for the specific component of the Allowance for Loan and

Lease Losses, that were considered individually impaired in accordance

with SFAS 114 at December 31, 2006 and 2005. SFAS 114 impairment

includes performing troubled debt restructurings and excludes all commer-

cial leases.

December 31

(Dollars in millions) 2006 2005

Commercial – domestic

$586

$613

Commercial real estate

118

49

Commercial – foreign

13

34

Total impaired loans

$717

$696

The average recorded investment in certain impaired loans for 2006,

2005 and 2004 was approximately $722 million, $852 million and $1.6

billion, respectively. At December 31, 2006 and 2005, the recorded

investment in impaired loans requiring an Allowance for Loan and Lease

Losses based on individual analysis per SFAS 114 guidelines was $567

million and $517 million, and the related Allowance for Loan and Lease

Losses was $43 million and $55 million. For 2006, 2005 and 2004,

Interest Income recognized on impaired loans totaled $36 million, $17

million and $21 million, respectively, all of which was recognized on a

cash basis.

At December 31, 2006 and 2005, nonperforming loans and leases,

including impaired loans and nonaccrual consumer loans, totaled $1.8 bil-

lion and $1.5 billion. In addition, included in Other Assets were non-

performing loans held-for-sale of $80 million and $69 million at

December 31, 2006 and 2005.

The Corporation has loan products with varying terms (e.g., interest-

only mortgages, option adjustable rate mortgages, etc.) and loans with

high loan-to-value ratios. Exposure to any of these loan products does not

result in a significant concentration of credit risk. Terms of loan products,

collateral coverage, the borrower’s credit history, and the amount of these

loans that are retained on our balance sheet are included in the Corpo-

ration’s assessment when establishing its Allowance for Loan and Lease

Losses.

Note 7 – Allowance for Credit Losses

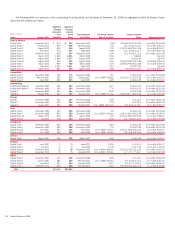

The following table summarizes the changes in the allowance for credit losses for 2006, 2005 and 2004:

(Dollars in millions) 2006 2005 2004

Allowance for loan and lease losses, January 1

$ 8,045

$ 8,626 $ 6,163

FleetBoston balance, April 1, 2004

–

– 2,763

MBNA balance, January 1, 2006

577

––

Loans and leases charged off

(5,881)

(5,794) (4,092)

Recoveries of loans and leases previously charged off

1,342

1,232 979

Net charge-offs

(4,539)

(4,562) (3,113)

Provision for loan and lease losses

5,001

4,021 2,868

Other

(68)

(40) (55)

Allowance for loan and lease losses, December 31

9,016

8,045 8,626

Reserve for unfunded lending commitments, January 1

395

402 416

FleetBoston balance, April 1, 2004

–

–85

Provision for unfunded lending commitments

9

(7) (99)

Other

(7)

––

Reserve for unfunded lending commitments, December 31

397

395 402

Total allowance for credit losses

$ 9,413

$ 8,440 $ 9,028

118

Bank of America 2006