Bank of America 2006 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

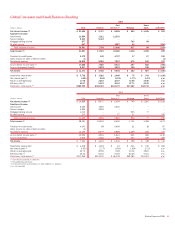

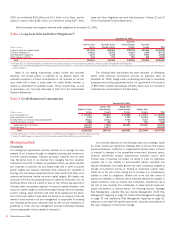

Balance Sheet

Average Balance

(Dollars in millions) 2006 2005

Total loans and leases

$243,282

$214,818

Total trading-related assets

338,364

314,568

Total market-based earning assets

(1)

369,164

322,236

Total earning assets

(2)

625,212

550,620

Total assets

(2)

706,906

633,253

Total deposits

205,652

189,860

Allocated equity

41,892

41,773

December 31

2006 2005

Total loans and leases

$246,490

$232,631

Total trading-related assets

309,321

291,267

Total market-based earning assets

(1)

347,572

305,374

Total earning assets

(2)

605,153

553,390

Total assets

(2)

689,248

633,362

Total deposits

216,875

198,352

Allocated equity

40,025

43,985

(1) Total market-based earning assets represents earning assets from the Capital Markets and Advisory

Services business.

(2) Total earning assets and Total Assets include asset allocations to match liabilities (i.e., deposits).

Global Corporate and Investment Banking provides a wide range of finan-

cial services to both our issuer and investor clients that range from busi-

ness banking clients to large international corporate and institutional

investor clients using a strategy to deliver value-added financial products

and advisory solutions. Global Corporate and Investment Banking’s prod-

ucts and services are delivered from three primary businesses: Business

Lending, Capital Markets and Advisory Services, and Treasury Services,

and are provided to our clients through a global team of client relationship

managers and product partners. In addition, ALM/Other includes the

results of ALM activities and our Latin America and Hong Kong based retail

and commercial banking businesses, parts of which were sold in 2006.

Our clients are supported through offices in 26 countries that are divided

into four distinct geographic regions: U.S. and Canada; Asia; Europe, Mid-

dle East, and Africa; and Latin America. For more information on our for-

eign operations, see Foreign Portfolio beginning on page 71.

Net Income increased $408 million, or six percent, in 2006. Driving

the increase were Trading Account Profits, Investment Banking Income,

and gains from the sale of our Brazilian operations and Asia Commercial

Banking business. These increases were partially offset by declines in Net

Interest Income and Gains on Sales of Debt Securities and increases in

Provision for Credit Losses and Noninterest Expense.

Although Global Corporate and Investment Banking experienced over-

all growth in Average Loans and Leases of $28.5 billion, or 13 percent,

and an increase in Average Deposits of $15.8 billion, or eight percent, Net

Interest Income declined primarily due to the impact of ALM activities,

spread compression in the loan portfolio and the impact of the sale of our

Brazilian operations in the third quarter of 2006. This decline was partially

offset by wider spreads in our Treasury Services deposit base as we effec-

tively managed pricing in a rising interest rate environment.

Noninterest Income increased $2.6 billion, or 27 percent, in 2006.

The increase in Noninterest Income was driven largely by the increase in

Trading Account Profits, Investment Banking Income, and the gain on the

sale of our Brazilian operations and Asia Commercial Banking business.

The increases in Trading Account Profits and Investment Banking Income

were driven by continued strength in debt underwriting, sales and trading,

and a favorable market environment. The sale of our Brazilian operations

and Asia Commercial Banking business generated $720 million and $165

million gains (pre-tax), respectively, and were reflected in all other income.

Provision for Credit Losses was negative $6 million in 2006 com-

pared to negative $291 million in 2005. The change in the Provision for

Credit Losses was primarily due to the absence in 2006 of benefits from

the release of reserves in 2005 related to an improved risk profile in Latin

America and reduced uncertainties associated with the FleetBoston Finan-

cial Corporation (FleetBoston) credit integration as well as lower commer-

cial recoveries in 2006. This increase was partially offset by benefits in

2006 from reductions in commercial reserves as a stable economic envi-

ronment throughout 2006 drove sustained favorable commercial credit

market conditions.

Noninterest Expense increased $865 million, or eight percent, mainly

due to higher Personnel expense, including performance-based incentive

compensation primarily in Capital Markets and Advisory Services and

Other General Operating costs.

Business Lending

Business Lending provides a wide range of lending-related products and

services to our clients through client relationship teams along with various

product partners. Products include commercial and corporate bank loans

and commitment facilities which cover our business banking clients, mid-

dle market commercial clients and our large multinational corporate cli-

ents. Real estate lending products are issued primarily to public and

private developers, homebuilders and commercial real estate firms. Leas-

ing and asset-based lending products offer our clients innovative financing

solutions. Products also include indirect consumer loans which allow us to

offer financing through automotive, marine, motorcycle and recreational

vehicle dealerships across the U.S. Business Lending also contains the

results for the economic hedging of our risk to certain credit counter-

parties utilizing various risk mitigation tools such as Credit Default Swaps

(CDS) and may also include the results of other products to help reduce

hedging costs.

Net Income decreased $365 million, or 14 percent, primarily due to

decreases in Net Interest Income and Noninterest Income, combined with

an increase in Noninterest Expense. These items were partially offset by a

decrease in the Provision for Credit Losses. The decrease in Net Interest

Income of $220 million or five percent, was driven by the impact of lower

spreads on all loan products which was partially offset by loan growth.

Average Loans and Leases increased 12 percent primarily due to growth in

the commercial and indirect consumer loan portfolio. The decrease in

Noninterest Income was due to an increase in credit mitigation costs as

spreads continued to tighten and lower equity gains in all other income.

Provision for Credit Losses was $3 million in 2006 compared to $67 mil-

lion in 2005. The low level of Provision for Credit Losses in 2006 was

driven by benefits in 2006 from reductions in commercial reserves as a

stable economic environment throughout 2006 drove sustained favorable

commercial credit market conditions. These benefits were in part offset by

lower commercial recoveries in 2006. Benefits from the release of

reserves related to reduced uncertainties associated with the FleetBoston

credit integration contributed to the low level of Provision for Credit Losses

in 2005. The increase in Noninterest Expense was primarily driven by

increased expenses associated with Personnel, technology, and Pro-

fessional Fees.

Capital Markets and Advisory Services

Capital Markets and Advisory Services provides products, advisory serv-

ices and financing globally to our institutional investor clients in support of

their investing and trading activities. We also work with our commercial

and corporate issuer clients to provide debt and equity underwriting and

distribution capabilities, merger-related advisory services and risk

management solutions using interest rate, equity, credit and commodity

derivatives, foreign exchange, fixed income and mortgage-related products.

Bank of America 2006

51