Bank of America 2006 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

resulting from bankruptcy reform and the absence of the $210 million

provision recorded in 2005 to establish reserves for changes in credit card

minimum payment requirements were partially offset by portfolio season-

ing. Consumer provision expense increased throughout the year as most

products trended toward more normalized credit cost levels due to portfo-

lio seasoning and an upward trend in bankruptcy-related charge-offs from

the unusually low levels experienced post bankruptcy reform. Credit costs

in Europe increased throughout the year due to seasoning of the credit

card portfolio and higher personal insolvencies in the United Kingdom. For

discussions of the impact of SOP 03-3, see Consumer Portfolio Credit Risk

Management beginning on page 63.

The commercial portion of the Provision for Credit Losses for 2006

was $243 million compared to negative $370 million in 2005. The

increase was driven by the absence in 2006 in Global Corporate and

Investment Banking of benefits from the release of reserves in 2005

related to an improved risk profile in Latin America and reduced

uncertainties associated with the FleetBoston credit integration. Also con-

tributing to the increase were both the addition of MBNA and seasoning of

the business card and small business portfolios in Global Consumer and

Small Business Banking, as well as lower recoveries in 2006 in Global

Corporate and Investment Banking. Partially offsetting these increases

were reductions in Global Corporate and Investment Banking commercial

reserves in 2006 as a stable economic environment throughout 2006

drove sustained favorable commercial credit market conditions.

The Provision for Credit Losses related to unfunded lending commit-

ments was $9 million in 2006 compared to negative $7 million in 2005.

Allowance for Credit Losses

Allowance for Loan and Lease Losses

The Allowance for Loan and Lease Losses is allocated based on two

components. We evaluate the adequacy of the Allowance for Loan and

Lease Losses based on the combined total of these two components.

The first component of the Allowance for Loan and Lease Losses

covers those commercial loans that are either nonperforming or impaired.

An allowance is allocated when the discounted cash flows (or collateral

value or observable market price) are lower than the carrying value of that

loan. For purposes of computing the specific loss component of the allow-

ance, larger impaired loans are evaluated individually and smaller impaired

loans are evaluated as a pool using historical loss experience for the

respective product type and risk rating of the loans.

The second component of the Allowance for Loan and Lease Losses

covers performing commercial loans and leases, and consumer loans. The

allowance for commercial loan and lease losses is established by product

type after analyzing historical loss experience by internal risk rating, cur-

rent economic conditions, industry performance trends, geographic or obli-

gor concentrations within each portfolio segment, and any other pertinent

information. The commercial historical loss experience is updated quar-

terly to incorporate the most recent data reflective of the current economic

environment. As of December 31, 2006, quarterly updating of historical

loss experience did not have a material impact on the Allowance for Loan

and Lease Losses. The allowance for consumer and certain homogeneous

commercial loan and lease products is based on aggregated portfolio

segment evaluations, generally by product type. Loss forecast models are

utilized that consider a variety of factors including, but not limited to, his-

torical loss experience, estimated defaults or foreclosures based on

portfolio trends, delinquencies, economic trends and credit scores. These

loss forecast models are updated on a quarterly basis in order to

incorporate information reflective of the current economic environment. As

of December 31, 2006, quarterly updating of the loss forecast models

increased the Allowance for Loan and Lease Losses due to portfolio sea-

soning and the trend toward more normalized loss levels. Included within

this second component of the Allowance for Loan and Lease Losses and

determined separately from the procedures outlined above are reserves

which are maintained to cover uncertainties that affect our estimate of

probable losses including the imprecision inherent in the forecasting

methodologies, as well as domestic and global economic uncertainty,

large single name defaults and event risk. During 2006, commercial

reserves were released as a stable economic environment throughout

2006 drove sustained favorable commercial credit market conditions.

We monitor differences between estimated and actual incurred loan

and lease losses. This monitoring process includes periodic assessments

by senior management of loan and lease portfolios and the models used

to estimate incurred losses in those portfolios.

Additions to the Allowance for Loan and Lease Losses are made by

charges to the Provision for Credit Losses. Credit exposures deemed to be

uncollectible are charged against the Allowance for Loan and Lease Loss-

es. Recoveries of previously charged off amounts are credited to the

Allowance for Loan and Lease Losses.

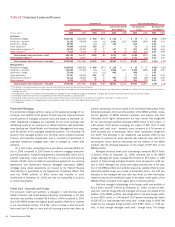

The Allowance for Loan and Lease Losses for the consumer portfolio

as presented in Table 27 was $5.6 billion at December 31, 2006, an

increase of $1.0 billion from December 31, 2005. This increase was

primarily attributable to the addition of MBNA.

The allowance for commercial loan and lease losses was $3.5 billion

at December 31, 2006, a $74 million decrease from December 31, 2005.

Commercial – foreign allowance levels decreased due to the sale of our

Brazilian operations. The increase in commercial – domestic allowance

levels was primarily attributable to the addition of MBNA partially offset by

the above mentioned reductions in commercial reserves in 2006.

Within the individual consumer and commercial product categories,

credit card – domestic allowance levels include reductions throughout

2006 from new securitizations and reductions as reserves established in

2005 for changes in minimum payment requirements were utilized to

absorb associated net charge-offs. Direct/indirect consumer allowance

levels increased as the Corporation discontinued new sales of receivables

into the Card Services unsecured lending securitization trusts. Commercial

– domestic allowance levels also increased as reserves were established

for new advances on business card accounts for which previous loan

balances were sold to the securitization trusts.

Reserve for Unfunded Lending Commitments

In addition to the Allowance for Loan and Lease Losses, we also estimate

probable losses related to unfunded lending commitments, such as letters

of credit and financial guarantees, and binding unfunded loan commit-

ments. Unfunded lending commitments are subject to individual reviews

and are analyzed and segregated by risk according to our internal risk rat-

ing scale. These risk classifications, in conjunction with an analysis of

historical loss experience, utilization assumptions, current economic con-

ditions and performance trends within specific portfolio segments, and any

other pertinent information result in the estimation of the reserve for

unfunded lending commitments. The reserve for unfunded lending

commitments is included in Accrued Expenses and Other Liabilities on the

Consolidated Balance Sheet.

We monitor differences between estimated and actual incurred credit

losses upon draws of the commitments. This monitoring process includes

periodic assessments by senior management of credit portfolios and the

models used to estimate incurred losses in those portfolios.

Bank of America 2006

73