Bank of America 2006 Annual Report Download - page 147

Download and view the complete annual report

Please find page 147 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155

|

|

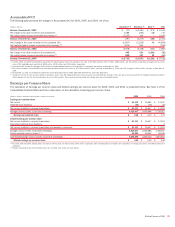

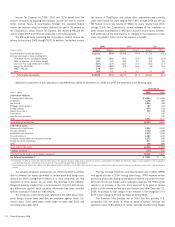

subsidiaries, provided certain criteria are met. Management elected to

apply the Act for 2005 and recorded a one-time tax benefit of $70 million

for the year ended December 31, 2005.

At December 31, 2006 and 2005, federal income taxes had not

been provided on $4.4 billion and $1.4 billion of undistributed earnings of

foreign subsidiaries, earned prior to 1987 and after 1997 that have been

reinvested for an indefinite period of time. If the earnings were distributed,

an additional $573 million and $249 million of tax expense, net of credits

for foreign taxes paid on such earnings and for the related foreign with-

holding taxes, would have resulted in 2006 and 2005.

Note 19 – Fair Value of Financial Instruments

SFAS No. 107, “Disclosures About Fair Value of Financial Instruments”

(SFAS 107), requires the disclosure of the estimated fair value of financial

instruments. The fair value of a financial instrument is the amount at

which the instrument could be exchanged in a current transaction between

willing parties, other than in a forced or liquidation sale. Quoted market

prices, if available, are utilized as estimates of the fair values of financial

instruments. Since no quoted market prices exist for certain of the Corpo-

ration’s financial instruments, the fair values of such instruments have

been derived based on management’s assumptions, the estimated

amount and timing of future cash flows and estimated discount rates. The

estimation methods for individual classifications of financial instruments

are described more fully below. Different assumptions could significantly

affect these estimates. Accordingly, the net realizable values could be

materially different from the estimates presented below. In addition, the

estimates are only indicative of the value of individual financial instru-

ments and should not be considered an indication of the fair value of the

combined Corporation.

The provisions of SFAS 107 do not require the disclosure of the fair

value of lease financing arrangements and nonfinancial instruments,

including Goodwill and Intangible Assets such as purchased credit card,

affinity, and trust relationships.

Short-term Financial Instruments

The carrying value of short-term financial instruments, including cash and

cash equivalents, time deposits placed, federal funds sold and purchased,

resale and repurchase agreements, commercial paper and other short-

term investments and borrowings, approximates the fair value of these

instruments. These financial instruments generally expose the Corporation

to limited credit risk and have no stated maturities or have short-term

maturities and carry interest rates that approximate market.

Financial Instruments Traded in the Secondary

Market and Strategic Investments

Held-to-maturity securities, AFS debt and marketable equity securities,

trading account instruments, long-term debt traded actively in the secon-

dary market and strategic investments have been valued using quoted

market prices. The fair values of trading account instruments, securities

and strategic investments are reported in Notes 3 and 5 of the Con-

solidated Financial Statements.

Derivative Financial Instruments

All derivatives are recognized on the Consolidated Balance Sheet at fair

value, net of cash collateral held and taking into consideration the effects

of legally enforceable master netting agreements that allow the Corpo-

ration to settle positive and negative positions with the same counterparty

on a net basis. For exchange-traded contracts, fair value is based on

quoted market prices. For non-exchange traded contracts, fair value is

based on dealer quotes, pricing models or quoted prices for instruments

with similar characteristics. The fair value of the Corporation’s derivative

assets and liabilities is presented in Note 4 of the Consolidated Financial

Statements.

Loans

Fair values were estimated for groups of similar loans based upon type of

loan and maturity. The fair value of loans was determined by discounting

estimated cash flows using interest rates approximating the Corporation’s

current origination rates for similar loans and adjusted to reflect the

inherent credit risk. Where quoted market prices were available, primarily

for certain residential mortgage loans and commercial loans, such market

prices were utilized as estimates for fair values.

Substantially all of the foreign loans reprice within relatively short

timeframes. Accordingly, for foreign loans, the net carrying values were

assumed to approximate their fair values.

Deposits

The fair value for deposits with stated maturities was calculated by dis-

counting contractual cash flows using current market rates for instruments

with similar maturities. The carrying value of foreign time deposits approx-

imates fair value. For deposits with no stated maturities, the carrying

amount was considered to approximate fair value and does not take into

account the significant value of the cost advantage and stability of the

Corporation’s long-term relationships with depositors.

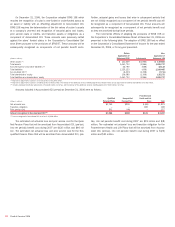

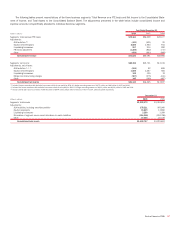

The book and fair values of certain financial instruments at

December 31, 2006 and 2005 were as follows:

December 31

2006 2005

(Dollars in millions) Book Value Fair Value Book Value Fair Value

Financial assets

Loans

(1)

$675,544 $679,738

$545,238 $542,626

Financial liabilities

Deposits

693,497 693,041

634,670 633,928

Long-term debt

146,000 148,120

100,848 101,446

(1) Presented net of the Allowance for Loan and Lease Losses.

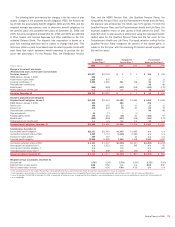

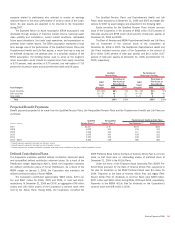

Note 20 – Business Segment Information

The Corporation reports the results of its operations through three busi-

ness segments: Global Consumer and Small Business Banking, Global

Corporate and Investment Banking, and Global Wealth and Investment

Management. The Corporation may periodically reclassify business seg-

ment results based on modifications to its management reporting method-

ologies and changes in organizational alignment.

Global Consumer and Small Business Banking provides a diversified

range of products and services to individuals and small businesses

through its primary businesses: Deposits, Card Services, Mortgage and

Home Equity. Global Corporate and Investment Banking serves domestic

and international issuer and investor clients, providing financial services,

specialized industry expertise and local delivery through its primary busi-

nesses: Business Lending, Capital Markets and Advisory Services, and

Treasury Services. These businesses provide traditional bank deposit and

loan products to large corporations and institutional clients, capital-raising

solutions, advisory services, derivatives capabilities, equity and debt sales

and trading for clients, as well as treasury management and payment serv-

ices. Global Wealth and Investment Management offers investment serv-

ices, estate management, financial planning services, fiduciary

management, credit and banking expertise, and diversified asset

management products to institutional clients, as well as affluent and high-

net-worth individuals through its primary businesses: The Private Bank,

Columbia Management and Premier Banking and Investments.

Bank of America 2006

145