Bank of America 2006 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

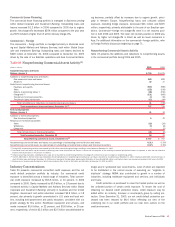

See Note 15 of the Consolidated Financial Statements for more

information on the Corporation’s regulatory requirements and restrictions.

The Corporation anticipates that the implementation, of FASB Staff

Position No. FAS 13-2, “Accounting for a Change or Projected Change in

the Timing of Cash Flows Relating to Income Taxes Generated by a Lever-

aged Lease Transaction,” will reduce Retained Earnings and associated

regulatory capital by approximately $1.4 billion after-tax as of January 1,

2007. The amount of the charge initially recorded will be recognized as

income over the remaining terms, generally 15 to 30 years, of the affected

leases. Further, this change in accounting will also result in an adverse

impact on earnings in the first two years subsequent to the change. The

Corporation expects that Net Income will be negatively impacted by approx-

imately $105 million in 2007. The Corporation anticipates that its Tier 1

and Total Capital Ratios will be negatively impacted by approximately 13

bps and its Tier 1 Leverage Ratio will be negatively impacted by approx-

imately 10 bps as a result of the initial adoption.

In November 2006, the Corporation announced a definitive agree-

ment to acquire U.S. Trust for $3.3 billion in cash. The transaction is

expected to close in the third quarter of 2007. The Corporation anticipates

that its Tier 1 and Total Capital Ratios will be negatively impacted by

approximately 35 bps and its Tier 1 Leverage Ratio will be negatively

impacted by approximately 25 bps upon the acquisition of U.S. Trust.

Basel II

In June 2004, Basel II was published with the intent of more closely align-

ing regulatory capital requirements with underlying risks. Similar to eco-

nomic capital measures, Basel II seeks to address credit risk, market risk,

and operational risk.

While economic capital is measured to cover unexpected losses, the

Corporation also maintains a certain threshold in terms of regulatory capi-

tal to adhere to legal standards of capital adequacy. These thresholds or

leverage ratios will continue to be utilized for the foreseeable future.

U.S. banks are required to implement Basel II within three years of

the date the final rules are published. Banks must successfully complete

four consecutive quarters of parallel calculations to be considered com-

pliant and to enter a three-year implementation period. The three-year

implementation period is subject to capital relief floors (limits) that are set

to help mitigate substantial decreases in an institution’s capital levels

when compared to current regulatory capital rules.

On September 25, 2006, the Agencies officially published several

documents providing updates to the Basel II Risk-Based Capital Standards

for the U.S. as well as new regulatory reporting requirements related to

these Risk-Based Capital Standards for review and comment by U.S.-

based banks and trade associations. These publications included pre-

viously published regulations and guidance as well as revised market risk

rules and a proposal including several new regulatory reporting templates.

These Capital Standards are expected to be finalized in 2007.

The Corporation continues its execution efforts to ensure prepared-

ness with Basel II requirements. The goal is to achieve full compliance

within the three-year implementation period. Further, the Corporation

anticipates being ready for all international reporting requirements that

occur before that time.

Dividends

Effective for the third quarter 2006 dividend, the Board increased the

quarterly cash dividend 12 percent from $0.50 to $0.56 per share. In

October 2006, the Board declared a fourth quarter cash dividend of $0.56

which was paid on December 22, 2006 to common shareholders of record

on December 1, 2006. In January 2007, the Board declared a quarterly

cash dividend of $0.56 per common share payable on March 23, 2007 to

shareholders of record on March 2, 2007.

In January 2007, the Board also declared three dividends in regards

to preferred stock. The first was a $1.75 regular cash dividend on the

Cumulative Redeemable Preferred Stock, Series B, payable April 25, 2007

to shareholders of record on April 11, 2007. The second was a regular

quarterly cash dividend of $0.38775 per depositary share on the Series D

Preferred Stock, payable March 14, 2007 to shareholders of record on

February 28, 2007. The third declared dividend was a regular quarterly

cash dividend of $0.40106 per depositary share of the Floating Rate

Non-Cumulative Preferred Stock, Series E, payable February 15, 2007 to

shareholders of record on January 31, 2007.

Common Share Repurchases

We will continue to repurchase shares, from time to time, in the open

market or in private transactions through our approved repurchase pro-

grams. We repurchased approximately 291.1 million shares of common

stock in 2006 which more than offset the 118.4 million shares issued

under employee stock plans.

In April 2006, the Board authorized a stock repurchase program of up

to 200 million shares of the Corporation’s common stock at an aggregate

cost not to exceed $12.0 billion to be completed within a period of 12 to

18 months of which the lesser of approximately $4.9 billion, or

63.1 million shares, remains available for repurchase under the program

at December 31, 2006.

In January 2007, the Board authorized a stock repurchase program of

an additional 200 million shares of the Corporation’s common stock at an

aggregate cost not to exceed $14.0 billion to be completed within a period

of 12 to 18 months. For additional information on common share

repurchases, see Note 14 of the Consolidated Financial Statements.

Preferred Stock

In November 2006, the Corporation authorized 85,100 shares and issued

81,000 shares, or $2.0 billion, of Bank of America Corporation Floating

Rate Non-Cumulative Preferred Stock, Series E with a par value of $0.01

per share.

In September 2006, the Corporation authorized 34,500 shares and

issued 33,000 shares, or $825 million, of Series D Preferred Stock with a

par value of $0.01 per share.

During July 2006, the Corporation redeemed its 6.75% Perpetual

Preferred Stock with a stated value of $250 per share and its Fixed/

Adjustable Rate Cumulative Preferred Stock with a stated value of $250

per share.

For additional information on the issuance and redemption of pre-

ferred stock, see Note 14 of the Consolidated Financial Statements.

Credit Risk Management

Credit risk is the risk of loss arising from the inability of a borrower or

counterparty to meet its obligations. Credit risk can also arise from opera-

tional failures that result in an advance, commitment or investment of

funds. We define the credit exposure to a borrower or counterparty as the

loss potential arising from all product classifications including loans and

leases, derivatives, trading account assets, assets held-for-sale, and

unfunded lending commitments that include loan commitments, letters of

credit and financial guarantees. For derivative positions, our credit risk is

measured as the net replacement cost in the event the counterparties with

contracts in a gain position to us fail to perform under the terms of those

contracts. We use the current mark-to-market value to represent credit

exposure without giving consideration to future mark-to-market changes.

62

Bank of America 2006