Bank of America 2006 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

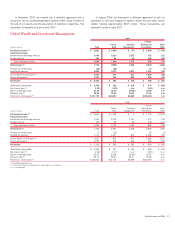

The management accounting reporting process derives segment and

business results by utilizing allocation methodologies for revenue,

expense and capital. The Net Income derived for the businesses are

dependent upon revenue and cost allocations using an activity-based cost-

ing model, funds transfer pricing, other methodologies, and assumptions

management believes are appropriate to reflect the results of the busi-

ness.

The Corporation’s ALM activities maintain an overall interest rate risk

management strategy that incorporates the use of interest rate contracts

to minimize significant fluctuations in earnings that are caused by interest

rate volatility. The Corporation’s goal is to manage interest rate sensitivity

so that movements in interest rates do not significantly adversely affect

Net Interest Income. The results of the business segments will fluctuate

based on the performance of corporate ALM activities. Some ALM activ-

ities are recorded in the businesses (i.e., Deposits) such as external

product pricing decisions, including deposit pricing strategies, as well as

the effects of our internal funds transfer pricing process and other ALM

actions such as portfolio positioning. The net effects of other ALM activ-

ities are reported in each of the Corporation’s segments under ALM/Other.

In addition, any residual effect of the funds transfer pricing process is

retained in All Other.

Certain expenses not directly attributable to a specific business

segment are allocated to the segments based on pre-determined means.

The most significant of these expenses include data processing costs,

item processing costs and certain centralized or shared functions. Data

processing costs are allocated to the segments based on equipment

usage. Item processing costs are allocated to the segments based on the

volume of items processed for each segment. The costs of certain central-

ized or shared functions are allocated based on methodologies which

reflect utilization.

Equity is allocated to business segments and related businesses

using a risk-adjusted methodology incorporating each unit’s credit, market,

interest rate and operational risk components. The nature of these risks is

discussed further beginning on page 62. ROE is calculated by dividing Net

Income by average allocated equity. SVA is defined as cash basis earnings

on an operating basis less a charge for the use of capital (i.e., equity).

Cash basis earnings on an operating basis is defined as Net Income

adjusted to exclude Merger and Restructuring Charges and Amortization of

Intangibles. The charge for capital is calculated by multiplying 11 percent

(management’s estimate of the shareholders’ minimum required rate of

return on capital invested) by average total common shareholders’ equity

at the corporate level and by average allocated equity at the business

segment level. Average equity is allocated to the business level using a

methodology identical to that used in the ROE calculation. Management

reviews the estimate of the rate used to calculate the capital charge

annually. The Capital Asset Pricing Model is used to estimate our cost of

capital.

See Note 20 of the Consolidated Financial Statements for additional

business segment information, selected financial information for the busi-

ness segments and reconciliations to consolidated Total Revenue and Net

Income amounts.

44

Bank of America 2006