Bank of America 2006 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

|

|

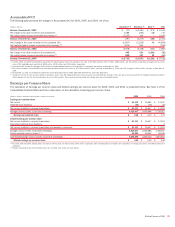

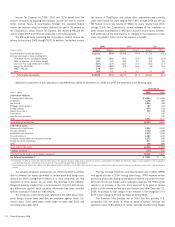

Amounts recognized in the Consolidated Financial Statements at December 31, 2006 and 2005 were as follows:

December 31, 2006

(Dollars in millions)

Qualified

Pension Plans

Nonqualified

Pension Plans

Postretirement

Health and Life

Plans

Other assets

$ 4,113 $ – $ –

Accrued expenses and other liabilities

– (1,345) (1,459)

Net amount recognized at December 31

$ 4,113 $(1,345) $(1,459)

December 31, 2005

(Dollars in millions)

Qualified

Pension Plans

Nonqualified

Pension Plans

Postretirement

Health and Life

Plans

Prepaid benefit cost

$4,237

$— $—

Accrued benefit cost

—

(897) (981)

Additional minimum liability

—

(187) —

SFAS 87 Accumulated OCI adjustment

(1)

— 187 —

Net amount recognized at December 31 $4,237 $ (897) $ (981)

(1) Amount recognized in Accumulated OCI net of tax is $118 million.

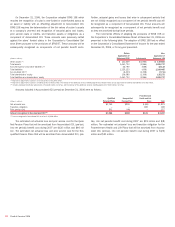

Net periodic benefit cost for 2006, 2005 and 2004 included the following components:

Qualified

Pension Plans

Nonqualified

Pension Plans

Postretirement

Health and Life Plans

(Dollars in millions) 2006 2005 2004 2006 2005 2004 2006 2005 2004

Components of net periodic benefit cost

Service cost

$ 306

$ 261 $ 257

$13

$11 $27

$13

$11 $ 9

Interest cost

676

643 623

78

61 62

86

78 76

Expected return on plan assets

(1,034)

(983) (915)

–

––

(10)

(14) (16)

Amortization of transition obligation

–

––

–

––

31

31 32

Amortization of prior service cost (credits)

41

44 55

(8)

(8) 3

–

–1

Recognized net actuarial loss

229

182 92

20

24 14

12

80 74

Recognized loss due to settlements and curtailments

–

––

–

9–

–

––

Net periodic benefit cost

$ 218

$ 147 $ 112

$ 103

$ 97 $ 106

$ 132

$ 186 $ 176

Weighted average assumptions used to determine net cost for

years ended December 31

Discount rate

(1)

5.50%

5.75% 6.25%

5.50%

5.75% 6.25%

5.50%

5.75% 6.25%

Expected return on plan assets

8.00

8.50 8.50

n/a

n/a n/a

8.00

8.50 8.50

Rate of compensation increase

4.00

4.00 4.00

4.00

4.00 4.00

n/a

n/a n/a

(1) In connection with the FleetBoston merger, their plans were remeasured on April 1, 2004, using a discount rate of 6.00 percent.

n/a = not applicable

Net periodic postretirement health and life expense was determined

using the “projected unit credit” actuarial method. Gains and losses for all

benefits except postretirement health care are recognized in accordance

with the standard amortization provisions of the applicable accounting

standards. For the Postretirement Health Care Plans, 50 percent of the

unrecognized gain or loss at the beginning of the fiscal year (or at sub-

sequent remeasurement) is recognized on a level basis during the year.

Assumed health care cost trend rates affect the postretirement bene-

fit obligation and benefit cost reported for the Postretirement Health Care

Plans. The assumed health care cost trend rate used to measure the

expected cost of benefits covered by the Postretirement Health Care Plans

was 9.0 percent for 2007, reducing in steps to 5.0 percent in 2012 and

later years. A one-percentage-point increase in assumed health care cost

trend rates would have increased the service and interest costs and the

benefit obligation by $3 million and $51 million in 2006, $3 million and

$51 million in 2005, and $4 million and $56 million in 2004. A

one-percentage-point decrease in assumed health care cost trend rates

would have lowered the service and interest costs and the benefit obliga-

tion by $3 million and $44 million in 2006, $3 million and $43 million in

2005, and $3 million and $48 million in 2004.

Plan Assets

The Qualified Pension Plans have been established as retirement vehicles

for participants, and trusts have been established to secure benefits

promised under the Qualified Pension Plans. The Corporation’s policy is to

invest the trust assets in a prudent manner for the exclusive purpose of

providing benefits to participants and defraying reasonable expenses of

administration. The Corporation’s investment strategy is designed to pro-

vide a total return that, over the long-term, increases the ratio of assets to

liabilities. The strategy attempts to maximize the investment return on

assets at a level of risk deemed appropriate by the Corporation while

complying with ERISA and any applicable regulations and laws. The

investment strategy utilizes asset allocation as a principal determinant for

establishing the risk/reward profile of the assets. Asset allocation ranges

are established, periodically reviewed, and adjusted as funding levels and

liability characteristics change. Active and passive investment managers

are employed to help enhance the risk/return profile of the assets. An

additional aspect of the investment strategy used to minimize risk (part of

the asset allocation plan) includes matching the equity exposure of

participant-selected earnings measures. For example, the common stock

of the Corporation held in the trust is maintained as an offset to the

140

Bank of America 2006