Bank of America 2006 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

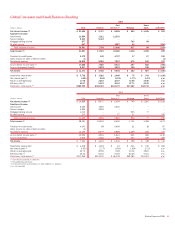

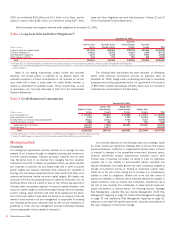

Balance Sheet

Average Balance

(Dollars in millions) 2006 2005

Total loans and leases $ 61,497 $ 54,102

Total earning assets

(1)

117,916 119,607

Total assets

(1)

125,663 127,394

Total deposits 115,071 117,338

Allocated equity 10,358 10,284

December 31

2006 2005

Total loans and leases

$ 66,034

$ 58,380

Total earning assets

(1)

129,589

121,269

Total assets

(1)

137,739

129,232

Total deposits

125,622

115,454

Allocated equity

11,007

12,813

(1) Total earning assets and Total Assets include asset allocations to match liabilities (i.e., deposits).

Global Wealth and Investment Management provides a wide offering of

customized banking and investment services tailored to meet the changing

wealth management goals of our individual and institutional customer

base. Our clients have access to a range of services offered through three

primary businesses: The Private Bank, Columbia Management (Columbia),

and Premier Banking and Investments (PB&I). In addition, ALM/Other

includes the impact of Banc of America Specialist, the results of ALM

activities and the impact of migrating qualifying affluent customers from

Global Consumer and Small Business Banking to our PB&I customer serv-

ice model.

Net Income increased $87 million, or four percent, due to higher

Total Revenue partially offset by higher Noninterest Expense.

Net Interest Income increased $61 million, or two percent, due to

increases in deposit spreads and higher Average Loans and Leases,

largely offset by a decline in ALM activities and loan spread compression.

Global Wealth and Investment Management also benefited from the migra-

tion of deposits from Global Consumer and Small Business Banking.

Noninterest Income increased $402 million, or 11 percent, due to

increases in Investment and Brokerage Services driven by higher levels of

assets under management. Noninterest Income also benefited from non-

recurring items in 2006.

Provision for Credit Losses decreased $33 million due to a credit

loss recovery in 2006.

Noninterest expense increased $295 million, or eight percent, primar-

ily due to increases in Personnel expense driven by the addition of sales

associates and revenue generating expenses.

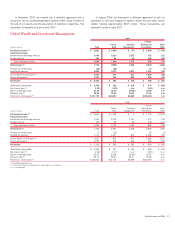

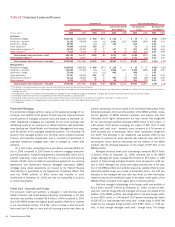

Client Assets

Client Assets consist of Assets under management, Client brokerage

assets, and Assets in Custody. Assets under management generate fees

based on a percentage of their market value. They consist largely of

mutual funds and separate accounts, which are comprised of taxable and

nontaxable money market products, equities, and taxable and nontaxable

fixed income securities. Client brokerage assets represent a source of

commission revenue and fees for the Corporation. Assets in custody

represent trust assets administered for customers. Trust assets encom-

pass a broad range of asset types including real estate, private company

ownership interest, personal property and investments.

Client Assets

December 31

(Dollars in millions) 2006 2005

Assets under management

$542,977

$482,394

Client brokerage assets

(1)

203,799

176,822

Assets in custody

100,982

94,184

Less: Client brokerage assets and Assets in custody

included in Assets under management

(57,446)

(44,931)

Total net client assets

$790,312

$708,469

(1) Client brokerage assets include non-discretionary brokerage and fee-based assets. Previously,

the Corporation reported Client brokerage assets excluding fee-based assets. The 2005 amounts

have been reclassified to reflect this adjustment.

Assets under management increased $60.6 billion, or 13 percent,

and was driven by net inflows in both money market and equity products

as well as market appreciation. Client brokerage assets increased by

$27.0 billion, or 15 percent, reflecting growth in full service assets from

higher broker productivity, as well as growth in self directed assets which

benefited from new pricing strategies including $0 Online Equity Trades

which were offered beginning in the fourth quarter of 2006. Assets in

custody increased $6.7 billion, or seven percent, due to market apprecia-

tion partially offset by net outflows.

The Private Bank

The Private Bank provides integrated wealth management solutions to high

net-worth individuals, middle-market institutions and charitable orga-

nizations with investable assets greater than $3 million. The Private Bank

provides investment, trust and banking services as well as specialty asset

management services (oil and gas, real estate, farm and ranch, timber-

land, private businesses and tax advisory). The Private Bank also provides

integrated wealth management solutions to ultra high-net-worth individuals

and families with investable assets greater than $50 million through its

Family Wealth Advisors unit. Family Wealth Advisors provides a higher level

of contact, tailored service and wealth management solutions addressing

the complex needs of their clients.

Net Income decreased $6 million, or one percent, primarily due to

increased Noninterest Expense and a decrease in Net Interest Income,

partially offset by higher Noninterest Income and a credit loss recovery.

The decrease in Net Interest Income of $8 million, or one percent, was

primarily attributable to lower average deposit balances as client money

flowed to equities, partially offset by wider deposit spreads. The increase

in Noninterest Income of $19 million, or two percent, was a result of non-

recurring items. The Provision for Credit Losses decreased $29 million as

a result of a credit loss recovery in 2006. The increase in Noninterest

Expense of $36 million, or three percent, was driven by higher personnel

and other operating costs.

In November 2006, the Corporation announced a definitive agree-

ment to acquire U.S. Trust for $3.3 billion in cash. U.S. Trust is one of the

largest and most respected U.S. firms which focuses exclusively on

managing wealth for high net-worth and ultra high net-worth individuals and

families. The acquisition will significantly increase the size and capabilities

of the Corporation’s wealth business and position it as one of the largest

financial services companies managing private wealth in the U.S. The

transaction is expected to close in the third quarter of 2007.

54

Bank of America 2006