Bank of America 2006 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

T

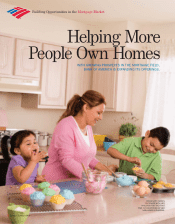

For years, 25-year-old Diana Soto of Phoenix yearned to get off the rental

treadmill. And then she had a reason to do so quickly: She and her two

young children outgrew their one-bedroom apartment. But she

calculated that she would not be able to afford her own home for years.

“I had to stop renting,” Soto recalled. “I thought that maybe, just maybe,

I could qualify to buy my place, but all people would tell me is, ‘No, you

can’t do that.’ ”

Then Soto met Bank of America Mortgage Loan Officer Herlinda Lopez,

who moved Soto off the home-ownership sidelines and into the game.

“My first thought was, ‘I’ve got to help make her dream come true,’ ”

said Lopez.

Lopez knew that help — the Community CommitmentTM mortgage —

was available to Soto and thousands of others looking to buy their first

homes, even people with low or moderate incomes and limited credit his-

tory. Besides having a reduced application fee, a Community Commitment

mortgage requires no traditional credit history, and owners can put down

as little as 1 percent of the purchase price for a down payment.

These loans have leveled the playing field in the real estate market, help-

ing lower-income customers afford homes. And by removing the hurdles to

home ownership for first-time buyers, Community Commitment mortgages

have created greater stability for the community as a whole.

To Soto, what mattered most was not only finding a loan program that

suited her financial circumstances, but also meeting a mortgage loan

officer who could help her learn the ropes in the mortgage market. “All the

time that I’m with Herlinda, I’m relaxed,” said Soto. “She kept telling me,

‘We can get this done.’ ” And they did.

Soto remembers walking into her new home for the first time. “I’m

thinking, I can’t believe I’m in my new house and that it’s mine,” she said.

“I worked hard all my life, and now I have my house. It’s incredible.”

Bank of America 2006 19

■ Mortgage Rewards™ saves a typical customer up to $2,000 in fees.

■ Community Commitment™ helps those with limited income or credit.

■ We guarantee the best value to our customers, or we pay them $250.

Our

Innovations

■ $2.8 trillion in U.S. mortgages to be originated

in 2007 industrywide

■ 10,000 associates in our banking centers

coast-to-coast are enabled to originate mortgages

■ $1.2 trillion domestic market for structured

mortgage products

The

Opportunity FLOYD S. ROBINSON,

LEFT, PRESIDENT,

CONSUMER REAL ESTATE;

IAN BANWELL, CHIEF

INVESTMENT OFFICER

Opportunities in the

Mortgage Market

The mortgage business is one of Bank of

America’s clearest organic growth opportunities.

In 2006, only 9.7 percent of our deposit

customers who got a mortgage got it with us.

By expanding products and eligibility,

eliminating fees and simplifying the mortgage

process, we are building understanding among

our 53 million customers that there are clear

advantages to getting a mortgage with us.

In 2006, Bank of America expanded

Mortgage RewardsTM to save home buyers on

average $2,000 in closing costs. With

Community CommitmentTM, w e h e lp mor e

low- and moderate-income customers achieve

home ownership. Through the innovative Best

Value Guarantee, if we approve a customer for

a mortgage and the customer chooses another

lender — for any reason — we pay the customer

$250. We are this confident in the quality of our

mortgage products and services.

“Home ownership is central to the Ameri-

can dream. Mortgage financing must be a key

strength for Bank of America to effectively serve

all the financial needs of our customers,” said

Floyd Robinson, president of Consumer Real

Estate. “We will take advantage of the strengths

we have across the bank to bring the best mort-

gage solutions to our customers.”

Over time, we will be able to distribute these

mortgages to the fixed-income market, too.

“It’s important for the balance sheet to have

self-originated assets,” said Chief Invest-

ment Officer Ian Banwell. “It takes maximum

advantage of our company’s significant ability

to gather deposits, and it facilitates greater

financial innovation for customers.”