Bank of America 2006 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Preferred Stock and redeemed its 382,450 shares, or $96 million, of

6.75% Perpetual Preferred Stock. Both classes were redeemed at their

stated value of $250 per share, plus accrued and unpaid dividends.

In September 2006, the Corporation completed the sale of its Brazil-

ian operations in exchange for approximately $1.9 billion in equity of

Banco Itaú Holding Financeira S.A. (Banco Itaú), Brazil’s second largest

nongovernment-owned banking company. The sale resulted in a $720 mil-

lion gain (pre-tax) that was recorded in Other Income. In August 2006, we

announced a definitive agreement to sell our operations in Chile and

Uruguay for stock in Banco Itaú and other consideration totaling

approximately $615 million. These transactions, as well as the previously

announced sale of our operations in Argentina, are expected to close in

early 2007.

MBNA Merger Overview

The Corporation acquired 100 percent of the outstanding stock of MBNA

Corporation (MBNA) on January 1, 2006, for $34.6 billion. In connection

therewith 1,260 million shares of MBNA common stock were exchanged

for 631 million shares of the Corporation’s common stock. Prior to the

MBNA merger, this represented approximately 16 percent of the Corpo-

ration’s outstanding common stock. MBNA shareholders also received

cash of $5.2 billion. The MBNA merger was a tax-free merger for the

Corporation. The acquisition expands the Corporation’s customer base

and its opportunity to deepen customer relationships across the full

breadth of the Corporation by delivering innovative deposit, lending and

investment products and services to MBNA’s customer base. Additionally,

the acquisition allows the Corporation to significantly increase its affinity

relationships through MBNA’s credit card operations and sell these credit

cards through our delivery channels (including the retail branch network).

MBNA’s results of operations were included in the Corporation’s results

beginning January 1, 2006. The purchase price has been allocated to the

assets acquired and the liabilities assumed based on their fair values at

the MBNA merger date. For more information related to the MBNA merger,

see Note 2 of the Corporation’s Consolidated Financial Statements.

Economic Overview

In 2006, the U.S. economic performance was healthy as real Gross

Domestic Product grew an estimated annualized 3.4 percent. Consumer

spending remained resilient despite significant declines in housing and

mortgage refinancing activities. Global economies recorded another solid

year of growth, led by robust expansion in Asia. Importantly, Germany and

Japan maintained their economic momentum as the U.S. weathered a soft

patch in growth. The FRB concluded two consecutive years of rate hikes in

June, raising its rate to 5.25 percent, as increases remained on hold in

the second half of the year. The yield curve remained inverted for much of

the second half of the year, reflecting the FRB’s rate increases, its

inflation-fighting credibility, and rising foreign capital inflows. In response

to the rate hikes and removal of monetary accommodation, housing sales

and construction fell sharply, median house prices flattened after surging

for a half decade, and mortgage refinancing activity fell sharply. However,

business investment remained strong, and solid increases in non-

residential construction partially offset the declines in housing. Consumer

spending, buoyed by rising personal incomes, relative low interest rates

and record-breaking wealth, continued to grow, ending the year on a strong

note. Dramatic declines in oil and energy prices in August through October

sharply reduced inflation, while core measures of inflation, excluding the

volatile energy and food components, rose through September. Core

inflation drifted modestly lower through year end, but remained above the

two percent upper bound of the FRB’s comfort range. With the exception of

housing, automobiles and related industries sustained healthy product

demand and modest pricing power provided businesses record profits. In

this environment, businesses continued to hire, and the unemployment

rate receded to 4.5 percent, well below its historic average.

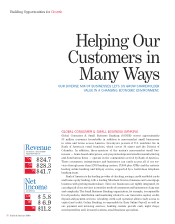

Performance Overview

Net Income reached $21.1 billion, or $4.59 per diluted common share in 2006, increases of 28 percent and 14 percent from $16.5 billion, or $4.04 per

diluted common share in 2005.

Table 1 Business Segment Total Revenue and Net Income

Total Revenue Net Income

(Dollars in millions) 2006 2005 2006 2005

Global Consumer and Small Business Banking

$41,691

$28,323

$11,171

$ 7,021

Global Corporate and Investment Banking

22,691

20,600

6,792

6,384

Global Wealth and Investment Management

7,779

7,316

2,403

2,316

All Other

2,086

684

767

744

Total FTE basis

(1)

74,247

56,923

21,133

16,465

FTE adjustment

(1)

(1,224)

(832)

––

Total Consolidated

$73,023

$56,091

$21,133

$16,465

(1) Total revenue for the business segments and All Other is on a fully taxable-equivalent (FTE) basis. For more information on a FTE basis, see Supplemental Financial Data beginning on page 41.

Global Consumer and Small Business Banking

Net Income increased $4.2 billion, or 59 percent, to $11.2 billion and

Total Revenue increased $13.4 billion, or 47 percent, to $41.7 billion in

2006 compared to 2005. These increases were driven by higher Net Inter-

est Income and Noninterest Income. Net Interest Income increased primar-

ily due to the MBNA merger and organic growth which increased Average

Loans and Leases. Noninterest Income increased primarily due to the

MBNA merger which resulted in an increase in Card Income driven by

increases in excess servicing income, cash advance fees, interchange

income and late fees. These increases were partially offset by higher

Noninterest Expense and Provision for Credit Losses, primarily driven by

the addition of MBNA. For more information on Global Consumer and

Small Business Banking, see page 45.

36

Bank of America 2006