Bank of America 2006 Annual Report Download - page 121

Download and view the complete annual report

Please find page 121 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

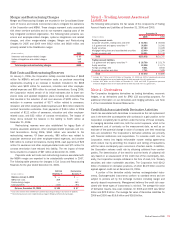

Note 8 – Mortgage Servicing Rights

Effective January 1, 2006, the Corporation adopted SFAS 156 and

accounts for consumer-related MSRs at fair value with changes in fair

value recorded in the Consolidated Statement of Income in Mortgage

Banking Income. The Corporation economically hedges these MSRs with

certain derivatives such as options and interest rate swaps. Prior to Jan-

uary 1, 2006, consumer-related MSRs were accounted for on a lower of

cost or market basis and hedged with derivatives that qualified for SFAS

133 hedge accounting.

The following table presents activity for consumer-related MSRs for

2006 and 2005.

(Dollars in millions) 2006 2005

Balance, January 1

$2,658

$2,358

MBNA balance, January 1, 2006

9

–

Additions

572

860

Sales of MSRs

(71)

(176)

Impact of customer payments

(713)

–

Amortization

–

(612)

Other changes in MSR market value

(1)

414

228

Balance, December 31 (2)

$2,869

$2,658

(1) For 2006, amount reflects changes in discount rates and prepayment speed assumptions, mostly due to changes in interest rates. For 2005, amount reflects $291 million related to change in value attributed to SFAS 133

hedged MSRs, and $63 million of impairments.

(2) Before the adoption of SFAS 156, there was an impairment allowance of $257 million at December 31, 2005.

Commercial-related MSRs are accounted for using the amortization

method (i.e., lower of cost or market). Commercial-related MSRs were

$176 million and $148 million at December 31, 2006 and 2005 and are

not included in the table above.

The key economic assumptions used in valuations of MSRs included

modeled prepayment rates and resultant weighted-average lives of the

MSRs and the option adjusted spread (OAS) levels. An OAS model runs

multiple interest rate scenarios and projects prepayments specific to each

one of those interest rate scenarios.

As of December 31, 2006, the fair value of consumer-related MSRs

was $2.9 billion, and the modeled weighted-average lives of MSRs related

to fixed and adjustable rate loans (including hybrid Adjustable Rate Mort-

gages) were 4.98 years and 3.19 years. The following table presents the

sensitivity of the weighted-average lives and fair value of MSRs to changes

in modeled assumptions.

December 31, 2006

Change in

Weighted-average lives Change in

Fair value

(Dollars in millions) Fixed Adjustable

Prepayment rates

Impact of 10% decrease

0.33 years

0.26 years $ 135

Impact of 20% decrease

0.70

0.58 289

Impact of 10% increase

(0.29)

(0.23) (120)

Impact of 20% increase

(0.55)

(0.42) (227)

OAS level

Impact of 100 bps decrease

n/a

n/a 109

Impact of 200 bps decrease

n/a

n/a 227

Impact of 100 bps increase

n/a

n/a (101)

Impact of 200 bps increase

n/a

n/a (195)

n/a = not applicable

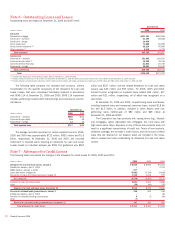

Note 9 – Securitizations

The Corporation securitizes assets and may continue to hold a portion or

all of the securities, subordinated tranches, interest-only strips, sub-

ordinated interests in accrued interest and fees on the securitized receiv-

ables, and, in some cases, cash reserve accounts, all of which are known

as retained interests, which are carried at fair value or amounts that

approximate fair value. Those assets may be serviced by the Corporation

or by third parties.

Mortgage-related Securitizations

The Corporation securitizes a portion of its residential mortgage loan origi-

nations in conjunction with or shortly after loan closing. In addition, the

Corporation may, from time to time, securitize commercial mortgages and

first residential mortgages that it originates or purchases from other enti-

ties. In 2006 and 2005, the Corporation converted a total of $65.5 billion

(including $15.5 billion originated by other entities) and $95.1 billion

(including $15.9 billion originated by other entities), of commercial mort-

gages and first residential mortgages into mortgage-backed securities

issued through Fannie Mae, Freddie Mac, Government National Mortgage

Association, Bank of America, N.A. and Banc of America Mortgage Secu-

rities. At December 31, 2006 and 2005, the Corporation retained $5.5

billion (including $4.2 billion issued prior to 2006) and $7.2 billion

(including $2.4 billion issued prior to 2005) of these securities. At

December 31, 2006, these retained interests were valued using quoted

market prices.

In 2006, the Corporation reported $341 million in gains on loans

converted into securities and sold, of which gains of $329 million were

from loans originated by the Corporation and $12 million were from loans

originated by other entities. In 2005, the Corporation reported $575 mil-

lion in gains on loans converted into securities and sold, of which gains of

$592 million were from loans originated by the Corporation and losses of

$17 million were from loans originated by other entities. At December 31,

2006 and 2005, the Corporation had recourse obligations of $412 million

and $471 million with varying terms up to seven years on loans that had

been securitized and sold.

Bank of America 2006

119