Bank of America 2006 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

During 2006 and 2005, we purchased AFS debt securities of $40.9

billion and $204.5 billion, sold $55.1 billion and $133.4 billion, and had

maturities and received paydowns of $22.4 billion and $39.5 billion. We

realized $(443) million and $1.1 billion in Gains (Losses) on Sales of Debt

Securities during 2006 and 2005. The value of our Accumulated OCI

related to AFS debt securities increased (improved) by $131 million (pre-

tax) during 2006 which was driven by the realized loss on the securities

sale partially offset by an increase in interest rates.

Accumulated OCI includes $2.9 billion in after-tax losses at

December 31, 2006, related to after-tax unrealized losses associated with

our AFS securities portfolio, including $3.1 billion of after-tax unrealized

losses related to AFS debt securities and $249 million of after-tax unreal-

ized gains related to AFS equity securities. Total market value of the AFS

debt securities was $192.8 billion at December 31, 2006, with a

weighted average duration of 4.1 years and primarily relates to our

mortgage-backed securities portfolio.

Changes to the Accumulated OCI amounts for the AFS securities

portfolio going forward will be driven by further interest rate or price

fluctuations, the collection of cash flows including prepayment and

maturity activity, and the passage of time.

Residential Mortgage Portfolio

During 2006 and 2005, we purchased $42.3 billion and $32.0 billion of

residential mortgages related to ALM activities and sold $11.0 billion and

$10.1 billion. We added $51.9 billion and $18.3 billion of originated resi-

dential mortgages to the balance sheet for 2006 and 2005. Additionally,

we received paydowns of $24.7 billion and $35.8 billion for 2006 and

2005. The ending balance at December 31, 2006 was $241.2 billion,

compared to $182.6 billion at December 31, 2005.

Interest Rate and Foreign Exchange Derivative

Contracts

Interest rate and foreign exchange derivative contracts are utilized in our

ALM activities and serve as an efficient tool to mitigate our interest rate

and foreign exchange risk. We use derivatives to hedge the changes in

cash flows or changes in market values on our balance sheet due to inter-

est rate and foreign exchange components. See Note 4 of the Con-

solidated Financial Statements for additional information on our hedging

activities.

Our interest rate contracts are generally non-leveraged generic inter-

est rate and foreign exchange basis swaps, options, futures and forwards.

In addition, we use foreign exchange contracts, including cross-currency

interest rate swaps and foreign currency forward contracts, to mitigate the

foreign exchange risk associated with foreign currency-denominated

assets and liabilities, as well as certain equity investments in foreign

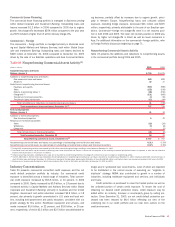

subsidiaries. Table 31 reflects the notional amounts, fair value, weighted

average receive fixed and pay fixed rates, expected maturity, and esti-

mated duration of our open ALM derivatives at December 31, 2006 and

2005.

The changes in our derivatives portfolio reflect actions taken for inter-

est rate and foreign exchange rate risk management. The decisions to

reposition our derivative portfolio are based upon the current assessment

of economic and financial conditions including the interest rate environ-

ment, balance sheet composition and trends, and the relative mix of our

cash and derivative positions. The notional amount of our net receive fixed

swap position (including foreign exchange contracts) decreased $10.5 bil-

lion to $12.3 billion at December 31, 2006 compared to $22.8 billion at

December 31, 2005. The decrease in the net receive fixed position is

primarily due to terminations and maturities within the portfolio during the

year. The notional amount of our foreign exchange basis swaps increased

$14.1 billion to $31.9 billion at December 31, 2006 compared to $17.8

billion at December 31, 2005. The notional amount of our option position

increased $186.0 billion to $243.3 billion at December 31, 2006, com-

pared to December 31, 2005. The increase in the notional amount of

options was due to the addition of caps used to reduce the sensitivity of

Net Interest Income to changes in market interest rates. Futures and for-

ward rate contracts are comprised primarily of $8.5 billion of forward pur-

chase contracts of mortgage loans at December 31, 2006 and $35.0

billion of forward purchase contracts of mortgage-backed securities and

mortgage loans at December 31, 2005. The forward purchase contracts

outstanding at December 31, 2006, settled in January 2007 with an aver-

age yield of 5.67 percent. The forward purchase contracts outstanding at

December 31, 2005, settled from January 2006 to April 2006, with an

average yield of 5.46 percent.

The following table includes derivatives utilized in our ALM activities,

including those designated as SFAS 133 accounting hedges and those

used as economic hedges. The fair value of net ALM contracts increased

from a loss of $386 million at December 31, 2005 to a gain of $1.5 bil-

lion at December 31, 2006. The increase was primarily attributable to

gains from changes in the value of foreign exchange basis swaps of $2.6

billion and receive fixed and pay fixed interest rate swaps of $1.3 billion,

partially offset by losses from changes in the values of foreign exchange

contracts of $1.2 billion, and option products of $1.0 billion. The increase

in the value of foreign exchange basis swaps was due to the strengthening

of most foreign currencies against the dollar during 2006. The increases

in the value of receive fixed interest rate swaps was due to terminations

partially offset by losses as a result of increases in market interest rates.

The increase in the value of pay fixed interest rate swaps was due to gains

from increases in market interest rates partially offset by terminations.

The decrease in the value of foreign exchange contracts was due primarily

to increases in foreign interest rates during 2006. The decrease in the

value of option products was primarily due to changes in the composition

of the option portfolio.

Bank of America 2006

79