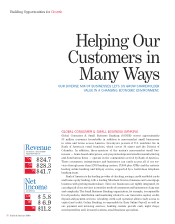

Bank of America 2006 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

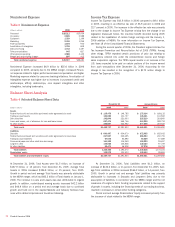

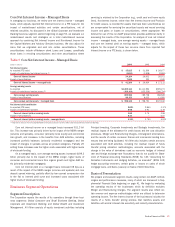

Federal Funds Sold and Securities Purchased under

Agreements to Resell

The Federal Funds Sold and Securities Purchased under Agreements to

Resell average balance increased $6.2 billion, or four percent, in 2006

compared to the prior year. The increase was from activities in the trading

businesses, primarily in interest rate and equity products, as a result of

expanded activities related to a variety of client needs.

Trading Account Assets

Trading Account Assets consist primarily of fixed income securities

(including government and corporate debt), equity and convertible instru-

ments. The average balance increased $11.8 billion to $145.3 billion in

2006, which was due to growth in client-driven market-making activities in

interest rate, credit and equity products. For additional information, see

Market Risk Management beginning on page 75.

Debt Securities

Available-for-sale (AFS) Debt Securities include fixed income securities

such as mortgage-backed securities, foreign debt, asset-backed secu-

rities, municipal debt, U.S. Government agencies and corporate debt. We

use the AFS portfolio primarily to manage interest rate risk and liquidity

risk and to take advantage of market conditions that create more econom-

ically attractive returns on these investments. The average balance in the

securities portfolio increased $5.4 billion from 2005 primarily due to the

increase in the AFS portfolio in the first half of the year partially offset by

the sale of mortgage-backed securities of $43.7 billion in the third quarter

of 2006. For additional information, see Market Risk Management begin-

ning on page 75.

Loans and Leases, Net of Allowance for Loan and

Lease Losses

Average Loans and Leases, net of Allowance for Loan and Lease Losses,

was $643.3 billion in 2006, an increase of 22 percent from 2005. The

consumer loan and lease portfolio increased $83.9 billion primarily due to

higher retained mortgage production and the MBNA merger. The commer-

cial loan and lease portfolio increased $31.3 billion due to organic growth

and the MBNA merger, including the business card portfolio. For a more

detailed discussion of the loan portfolio and the allowance for credit loss-

es, see Credit Risk Management beginning on page 62, and Notes 6 and

7 of the Consolidated Financial Statements.

Deposits

Average Deposits increased $40.6 billion to $673.0 billion in 2006 com-

pared to 2005 due to a $24.2 billion increase in average foreign interest-

bearing deposits and a $14.0 billion increase in average domestic

interest-bearing deposits primarily due to the assumption of liabilities in

connection with the MBNA merger. We categorize our deposits as core or

market-based deposits. Core deposits are generally customer-based and

represent a stable, low-cost funding source that usually react more slowly

to interest rate changes than market-based deposits. Core deposits

include savings, NOW and money market accounts, consumer CDs and

IRAs, and noninterest-bearing deposits. Core deposits exclude negotiable

CDs, public funds, other domestic time deposits and foreign interest-

bearing deposits. Average core deposits increased $11.0 billion to $574.6

billion in 2006, a two percent increase from the prior year. The increase

was distributed between consumer CDs and noninterest-bearing deposits

partially offset by decreases in NOW and money market deposits, and

savings. The increase in consumer CDs was impacted by the shift of

deposit balances from NOW and money market deposits and savings to

consumer CDs as a result of the favorable rates offered on consumer

CDs. Average market-based deposit funding increased $29.6 billion to

$98.4 billion in 2006 compared to 2005 due to increases of $24.2 billion

in foreign interest-bearing deposits and $5.3 billion in negotiable CDs,

public funds and other time deposits related to funding of growth in core

and market-based assets.

Federal Funds Purchased and Securities Sold under

Agreements to Repurchase

The Federal Funds Purchased and Securities Sold under Agreements to

Repurchase average balance increased $56.2 billion to $286.9 billion in

2006 as a result of expanded trading activities within interest rate and

equity products related to client activities.

Trading Account Liabilities

Trading Account Liabilities consist primarily of short positions in fixed

income securities (including government and corporate debt), equity and

convertible instruments. The average balance increased $7.0 billion to

$64.7 billion in 2006, which was due to growth in client-driven market-

making activities in equity products, partially offset by a reduction in inter-

est rate products. For additional information, see Market Risk

Management beginning on page 75.

Commercial Paper and Other Short-term Borrowings

Commercial Paper and Other Short-term Borrowings provide a funding

source to supplement Deposits in our ALM strategy. The average balance

increased $28.6 billion to $124.2 billion in 2006, mainly due to the

increase in Federal Home Loan Bank advances to fund core asset growth,

primarily in the ALM portfolio.

Long-term Debt

Period end and average Long-term Debt increased $45.2 billion and $32.4

billion. The increase resulted from the funding of core asset growth, the

addition of MBNA and the issuance of subordinated debt to support Tier 2

capital. For additional information, see Note 12 of the Consolidated Finan-

cial Statements.

Shareholders’ Equity

Period end and average Shareholders’ Equity increased $33.7 billion and

$30.6 billion primarily due to the issuance of stock related to the MBNA

merger. This increase along with Net Income and issuances of Preferred

Stock, was partially offset by cash dividends, net share repurchases of

Common Stock and redemption of Preferred Stock.

Bank of America 2006

39