Bank of America 2006 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

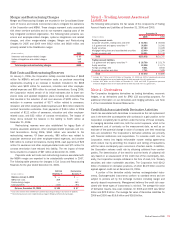

The following table presents the contract/notional amounts and

credit risk amounts at December 31, 2006 and 2005 of all the Corpo-

ration’s derivative positions. These derivative positions are primarily exe-

cuted in the over-the-counter market. The credit risk amounts take into

consideration the effects of legally enforceable master netting agree-

ments, and on an aggregate basis have been reduced by the cash

collateral applied against Derivative Assets. At December 31, 2006 and

2005, the cash collateral applied against Derivative Assets on the Con-

solidated Balance Sheet was $7.3 billion and $9.3 billion. In addition, at

December 31, 2006 and 2005, the cash collateral placed against

Derivative Liabilities was $6.5 billion and $7.6 billion.

December 31, 2006 December 31, 2005

(Dollars in millions)

Contract/

Notional

Credit

Risk

Contract/

Notional

Credit

Risk

Interest rate contracts

Swaps

$18,185,655 $ 9,601

$14,401,577 $11,085

Futures and forwards

2,283,579 103

2,113,717 –

Written options

1,043,933 –

900,036 –

Purchased options

1,308,888 2,212

869,471 3,345

Foreign exchange contracts

Swaps

451,462 4,241

333,487 3,735

Spot, futures and forwards

1,234,009 2,995

944,321 2,481

Written options

464,420 –

214,668 –

Purchased options

414,004 1,391

229,049 1,214

Equity contracts

Swaps

32,247 577

28,287 548

Futures and forwards

19,947 24

6,479 44

Written options

102,902 –

69,048 –

Purchased options

104,958 7,513

57,693 6,729

Commodity contracts

Swaps

4,868 1,129

8,809 2,475

Futures and forwards

13,513 2

5,533 –

Written options

9,947 –

7,854 –

Purchased options

6,796 184

3,673 546

Credit derivatives (1)

1,497,869 756

722,190 766

Credit risk before cash collateral

30,728

32,968

Less: Cash collateral applied

7,289

9,256

Total derivative assets

$23,439

$23,712

(1) The December 31, 2005 notional amount has been reclassified to conform with new regulatory guidance, which defined the notional as the contractual loss protection for structured basket transactions.

ALM Activities

Interest rate contracts and foreign exchange contracts are utilized in the

Corporation’s ALM activities. The Corporation maintains an overall interest

rate risk management strategy that incorporates the use of interest rate

contracts to minimize significant fluctuations in earnings that are caused

by interest rate volatility. The Corporation’s goal is to manage interest rate

sensitivity so that movements in interest rates do not significantly

adversely affect Net Interest Income. As a result of interest rate fluctua-

tions, hedged fixed-rate assets and liabilities appreciate or depreciate in

market value. Gains or losses on the derivative instruments that are linked

to the hedged fixed-rate assets and liabilities are expected to substantially

offset this unrealized appreciation or depreciation. Interest Income and

Interest Expense on hedged variable-rate assets and liabilities increase or

decrease as a result of interest rate fluctuations. Gains and losses on the

derivative instruments that are linked to these hedged assets and

liabilities are expected to substantially offset this variability in earnings.

Interest rate contracts, which are generally non-leveraged generic

interest rate and basis swaps, options and futures, allow the Corporation

to manage its interest rate risk position. Non-leveraged generic interest

rate swaps involve the exchange of fixed-rate and variable-rate interest

payments based on the contractual underlying notional amount. Basis

swaps involve the exchange of interest payments based on the contractual

underlying notional amounts, where both the pay rate and the receive rate

are floating rates based on different indices. Option products primarily

consist of caps, floors and swaptions. Futures contracts used for the

Corporation’s ALM activities are primarily index futures providing for cash

payments based upon the movements of an underlying rate index.

The Corporation uses foreign currency contracts to manage the for-

eign exchange risk associated with certain foreign currency-denominated

assets and liabilities, as well as the Corporation’s equity investments in

foreign subsidiaries. Foreign exchange contracts, which include spot and

forward contracts, represent agreements to exchange the currency of one

country for the currency of another country at an agreed-upon price on an

agreed-upon settlement date. Exposure to loss on these contracts will

increase or decrease over their respective lives as currency exchange and

interest rates fluctuate.

114

Bank of America 2006