Bank of America 2006 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

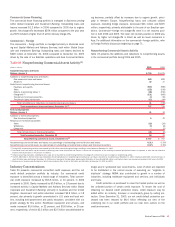

The following graph shows daily trading-related revenue and VAR for 2006.

Trading Risk and Return

Daily Trading-related Revenue and VAR

-100

-80

-60

-40

-20

0

20

40

60

80

100

12/31/05 3/31/06 6/30/06 9/30/06 12/31/06

(Dollars in Millions)

Daily

Trading -

related

Revenue

VA R

Table 28 presents average, high and low daily VAR for the twelve months ended December 31, 2006 and 2005.

Table 28 Trading Activities Market Risk

Twelve Months Ended December 31

2006 2005

VAR VAR

(Dollars in millions) Average High

(1)

Low

(1)

Average High

(1)

Low

(1)

Foreign exchange $ 8.2 $22.9 $ 3.1 $ 5.6 $12.1 $ 2.6

Interest rate 18.5 50.0 7.3 24.7 58.2 10.8

Credit 26.8 36.7 18.4 22.7 33.4 14.4

Real estate/mortgage 8.4 12.7 4.7 11.4 20.7 6.5

Equities 18.8 39.6 9.9 18.1 35.1 9.6

Commodities 6.1 9.9 3.4 6.6 10.6 3.5

Portfolio diversification (45.5) – – (47.3) – –

Total market-based trading portfolio (2) $ 41.3 $59.8 $26.0 $ 41.8 $67.0 $26.8

(1) The high and low for the total portfolio may not equal the sum of the individual components as the highs or lows of the individual portfolios may have occurred on different trading days.

(2) See Commercial Portfolio Credit Risk Management on page 66 for a discussion of the VAR related to the credit derivatives that economically hedge the loan portfolio.

Stress Testing

Because the very nature of a VAR model suggests results can exceed our

estimates, we also “stress test” our portfolio. Stress testing estimates

the value change in our trading portfolio that may result from abnormal

market movements. Various types of stress tests are run regularly against

the overall trading portfolio and individual businesses. Historical scenarios

simulate the impact of price changes which occurred during a set of

extended historical market events. The results of these scenarios are

reported daily to senior management. During 2006, the largest losses

among these scenarios ranged from $7 million to $591 million. Hypo-

thetical scenarios evaluate the potential impact of extreme but plausible

events. These scenarios are developed to address perceived vulner-

abilities in the market and in our portfolios, and are periodically updated.

Senior management reviews and evaluates results of these scenarios

monthly. During 2006, the largest losses among these scenarios ranged

from $441 million to $734 million. Worst-case losses, which represent the

most extreme losses in our daily VAR calculation, are reported daily.

Finally, desk-level stress tests are performed daily for individual busi-

nesses. These stress tests evaluate the potential adverse impact of large

moves in the market risk factors to which those businesses are most

sensitive.

Interest Rate Risk Management for Nontrading

Activities

Interest rate risk represents the most significant market risk exposure to

our nontrading exposures. Our overall goal is to manage interest rate risk

so that movements in interest rates do not adversely affect core net inter-

est income – managed basis. Interest rate risk is measured as the poten-

tial volatility in our core net interest income – managed basis caused by

changes in market interest rates. Client facing activities, primarily lending

and deposit-taking, create interest rate sensitive positions on our balance

sheet. Interest rate risk from these activities, as well as the impact of

changing market conditions, is managed through our ALM activities.

Simulations are used to estimate the impact on core net interest

income – managed basis using numerous interest rate scenarios, balance

sheet trends and strategies. These simulations evaluate how the above

Bank of America 2006

77