Bank of America 2006 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

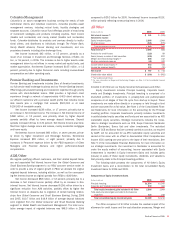

The credit risk amounts take into consideration the effects of legally

enforceable master netting agreements and cash collateral. Our consumer

and commercial credit extension and review procedures take into account

funded and unfunded credit exposures. For additional information on

derivatives and credit extension commitments, see Notes 4 and 13 of the

Consolidated Financial Statements.

For credit risk purposes, we evaluate our consumer businesses on

both a held and managed basis (a non-GAAP measure). Managed basis

treats securitized loan receivables as if they were still on the balance

sheet. We evaluate credit performance on a managed basis as the receiv-

ables that have been securitized are subject to the same underwriting

standards and ongoing monitoring as the held loans. In addition to the

discussion of credit quality statistics of both held and managed loans

included in this section, refer to the Card Services discussion beginning on

page 46. For additional information on our managed portfolio and securiti-

zations, refer to Note 9 of the Consolidated Financial Statements.

We manage credit risk based on the risk profile of the borrower or

counterparty, repayment sources, the nature of underlying collateral, and

other support given current events, conditions and expectations. We

classify our portfolios as either consumer or commercial and monitor

credit risk separately as discussed below.

Consumer Portfolio Credit Risk Management

Credit risk management for the consumer portfolio begins with initial under-

writing and continues throughout a borrower’s credit cycle. Statistical

techniques in conjunction with experiential judgment are used in all

aspects of portfolio management including product pricing, risk appetite,

setting credit limits, operating processes and metrics to quantify and

balance risks and returns. In addition, credit decisions are statistically

based with tolerances set to decrease the percentage of approvals as the

risk profile increases. Statistical models are built using detailed behavioral

information from external sources such as credit bureaus and/or internal

historical experience. These models are a critical component of our con-

sumer credit risk management process and are used in the determination

of both new and existing credit decisions, portfolio management strategies

including authorizations and line management, collection practices and

strategies, determination of the allowance for credit losses, and economic

capital allocations for credit risk.

For information on our accounting policies regarding delinquencies,

nonperforming status and charge-offs for the consumer portfolio, see

Note 1 of the Consolidated Financial Statements.

Management of Consumer Credit Risk

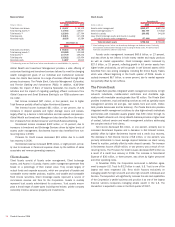

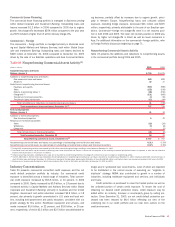

Concentrations

Consumer credit risk exposure is managed geographically and through our

various product offerings with a goal that concentrations of credit exposure

do not result in undesirable levels of risk. We purchase credit protection

on certain portions of our portfolio that is designed to enhance our overall

risk management strategy. At December 31, 2006 and 2005, we had

mitigated a portion of our credit risk on approximately $131.0 billion and

$110.4 billion of consumer loans, including both residential mortgage and

indirect automotive loans, through the purchase of credit protection. Our

regulatory risk-weighted assets were reduced as a result of these trans-

actions because we transferred a portion of our credit risk to unaffiliated

parties. At December 31, 2006 and 2005, these transactions had the

cumulative effect of reducing our risk-weighted assets by $36.4 billion and

$30.6 billion, and resulted in increases of 30 bps and 28 bps in our Tier 1

Capital ratio at December 31, 2006 and 2005.

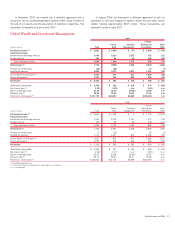

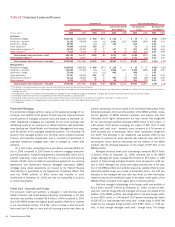

Consumer Credit Portfolio

Table 12 presents our held and managed consumer loans and leases and

related asset quality information for 2006 and 2005. Overall, consumer

credit quality remained sound in 2006 as performance was favorably

impacted by lower bankruptcy-related charge-offs.

Bank of America 2006

63