Bank of America 2006 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

Managed Basis

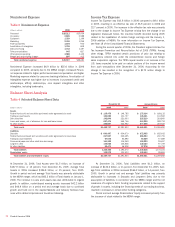

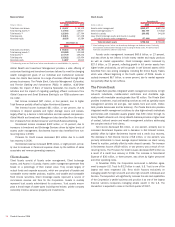

Managed Card Services Net Interest Income increased $10.9 billion to

$16.4 billion in 2006 compared to 2005. This increase was driven by the

addition of MBNA and organic growth which contributed to an increase in

total average managed outstandings.

Managed Card Services Noninterest Income increased $4.9 billion to

$8.5 billion in 2006 compared to 2005, largely resulting from the MBNA

merger and organic growth including increases in interchange income,

cash advance fees and late fees.

Managed Card Services net losses increased $3.0 billion to $7.2 bil-

lion or 3.78 percent of average Managed Card Services outstandings in

2006 compared to $4.2 billion, or 6.86 percent in 2005, primarily driven

by the addition of the MBNA portfolio and portfolio seasoning, partially

offset by lower bankruptcy-related losses. The 308 bps decrease in the

net loss ratio for Managed Card Services was driven by lower net losses

resulting from bankruptcy reform and the beneficial impact of the higher

credit quality of the MBNA portfolio compared to the legacy Bank of Amer-

ica portfolio. We expect managed net losses to trend towards more

normalized levels in 2007.

Managed Card Services total average outstandings increased $130.4

billion to $191.5 billion in 2006 compared to 2005. This increase was

driven by the addition of MBNA and organic growth.

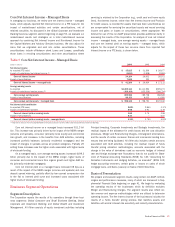

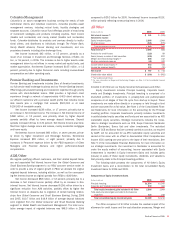

Held Basis

Net Income increased $4.6 billion to $5.6 billion in 2006 compared to

2005 due to revenue growth, partially offset by increases in Noninterest

Expense and Provision for Credit Losses.

Held Total Revenue increased $12.9 billion to $21.5 billion in 2006

compared to 2005 primarily due to the addition of MBNA and organic

growth. The MBNA merger increased excess servicing income, cash

advance fees, late fees, interchange income and all other income. Excess

servicing income benefited from lower net losses on the securitized loan

portfolio resulting from bankruptcy reform.

Held Provision for Credit Losses increased $728 million to $4.7 bil-

lion. This increase was primarily driven by the addition of the MBNA portfo-

lio and seasoning of the business card portfolio, partially offset by reduced

credit-related costs on the domestic consumer credit card portfolio. On the

domestic consumer credit card portfolio lower bankruptcy charge-offs

resulting from bankruptcy reform and the absence of the $210 million

provision recorded in 2005 to establish reserves for changes in credit card

minimum payment requirements were partially offset by portfolio

seasoning.

Card Services held net charge-offs were $3.9 billion, $112 million

higher than 2005, driven by the addition of the MBNA portfolio partially

offset by lower bankruptcy-related credit card net charge-offs. Credit card

held net charge-offs were $3.3 billion, or 4.55 percent of total average

held credit card loans, compared to $3.7 billion, or 6.76 percent, for

2005. This decrease was primarily driven by lower bankruptcy-related

charge-offs as 2005 included accelerated charge-offs resulting from bank-

ruptcy reform. The decrease was partially offset by the addition of the

MBNA portfolio, new advances on accounts for which previous loan balan-

ces were sold to the securitization trusts and portfolio seasoning.

Held total Noninterest Expense increased $4.9 billion to $7.8 billion

compared to the same period in 2005 primarily driven by the MBNA

merger which increased most expense items including Personnel, Market-

ing, and Amortization of Intangibles.

In connection with MasterCard’s initial public offering on May 24,

2006, the Corporation’s previous investment in MasterCard was

exchanged for new restricted shares. The Corporation recognized a net

pre-tax gain of approximately $36 million in all other income relating to the

shares that were required to be redeemed by MasterCard for cash and no

gain was recorded associated with the unredeemed shares. For shares

acquired as part of the MBNA merger, a purchase accounting adjustment

of $71 million was recorded as a reduction of Goodwill to record the fair

value of both the redeemed and unredeemed MasterCard shares. At

December 31, 2006, the Corporation had approximately 3.5 million

restricted shares of MasterCard that are accounted for at cost.

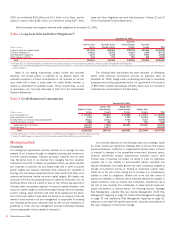

Mortgage

Mortgage generates revenue by providing an extensive line of mortgage

products and services to customers nationwide. Mortgage products are

available to our customers through a retail network of personal bankers

located in 5,747 banking centers, sales account executives in nearly 200

locations and through a sales force offering our customers direct tele-

phone and online access to our products. Additionally, we serve our cus-

tomers through a partnership with more than 6,500 mortgage brokers in

all 50 states. The mortgage product offerings for home purchase and

refinancing needs include fixed and adjustable rate loans. To manage this

portfolio, these products are either sold into the secondary mortgage

market to investors, while retaining the Bank of America customer

relationships, or are held on our balance sheet for ALM purposes.

The mortgage business includes the origination, fulfillment, sale and

servicing of first mortgage loan products. Servicing activities primarily

include collecting cash for principal, interest and escrow payments from

borrowers, and accounting for and remitting principal and interest pay-

ments to investors and escrow payments to third parties. Servicing income

includes ancillary income derived in connection with these activities such

as late fees.

Mortgage production within Global Consumer and Small Business

Banking was $76.7 billion in 2006 compared to $74.7 billion in 2005.

Net Income for Mortgage declined $116 million, or 29 percent, due

to a decrease in Total Revenue of $265 million to $1.4 billion, partially

offset by an $87 million decrease in Noninterest Expense. The decline in

Total Revenue was due to a decrease of $146 million in Net Interest

Income and a decrease of $142 million in Mortgage Banking Income. The

reduction in Net Interest Income was primarily driven by the impact of

spread compression. The decline in Mortgage Banking Income was primar-

ily due to margin compression which negatively impacted the pricing of

loans. This was partially offset by the favorable performance of the Mort-

gage Servicing Rights (MSRs) net of the derivatives used to economically

hedge changes in the fair values of the MSRs. Mortgage was not impacted

by the Corporation’s decision to retain a larger share of mortgage pro-

duction on the Corporation’s Balance Sheet, as Mortgage was compen-

sated for the decision on a management accounting basis with a

corresponding offset in All Other.

The Mortgage servicing portfolio includes loans serviced for others

and originated and retained residential mortgages. The servicing portfolio

at December 31, 2006 was $333.0 billion, $36.2 billion higher than

December 31, 2005, primarily driven by production and lower prepayment

rates. Included in this amount was $229.9 billion of loans serviced for

others.

48

Bank of America 2006