Bank of America 2006 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

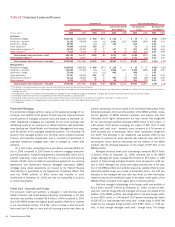

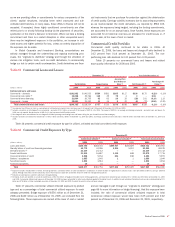

Table 12 Consumer Loans and Leases

December 31 Year Ended December 31

Outstandings Nonperforming

(1)

Accruing Past Due 90

Days or More

(2)

Net Charge-offs /

Losses

Net Charge-off /

Loss Ratios

(3)

(Dollars in millions) 2006 2005 2006 2005 2006 2005 2006 2005 2006 2005

Held basis

Residential mortgage

$241,181

$182,596

$ 660

$570

$ 118

$–

$39

$27

0.02%

0.02%

Credit card – domestic

61,195

58,548

n/a

n/a

1,991

1,197

3,094

3,652

4.85

6.76

Credit card – foreign

10,999

–

n/a

n/a

184

–

225

–

2.46

–

Home equity lines

74,888

62,098

249

117

–

–

51

31

0.07

0.05

Direct/Indirect consumer

(4)

68,224

45,490

44

37

347

75

524

248

0.88

0.55

Other consumer

(5)

9,218

6,725

77

61

38

15

303

275

2.83

3.99

Total consumer loans and leases – held

465,705

355,457

1,030

785

2,678

1,287

4,236

4,233

1.01

1.26

Securitizations impact (6)

110,151

12,523

2

–

2,407

23

3,371

434

3.22

3.34

Total consumer loans and leases – managed

$575,856

$367,980

$1,032

$785

$5,085

$1,310

$7,607

$4,667

1.45%

1.34%

Managed basis

Residential mortgage

$245,840

$188,380

$ 660

$570

$ 118

$–

$39

$27

0.02%

0.02%

Credit card – domestic

142,599

60,785

n/a

n/a

3,828

1,217

5,395

4,086

3.89

6.92

Credit card – foreign

27,890

–

n/a

n/a

608

–

980

–

3.95

–

Home equity lines

75,197

62,546

251

117

–

3

51

31

0.07

0.05

Direct/Indirect consumer

75,112

49,544

44

37

493

75

839

248

1.23

0.53

Other consumer

9,218

6,725

77

61

38

15

303

275

2.83

3.99

Total consumer loans and leases – managed

$575,856

$367,980

$1,032

$785

$5,085

$1,310

$7,607

$4,667

1.45%

1.34%

(1) The definition of nonperforming does not include consumer credit card and consumer non-real estate loans and leases.

(2) Accruing past due 90 days or more as a percentage of outstanding held and managed consumer loans and leases was 0.58 percent and 0.88 percent at December 31, 2006 and 0.36 percent and 0.36 percent at

December 31, 2005.

(3) Net charge-off/loss ratios are calculated as held net charge-offs or managed net losses divided by average outstanding held or managed loans and leases during the year for each loan and lease category.

(4) Outstandings include home equity loans of $12.8 billion and $8.1 billion at December 31, 2006 and 2005.

(5) Outstandings include foreign consumer loans of $6.2 billion and $3.8 billion and consumer finance loans of $2.8 billion and $2.8 billion at December 31, 2006 and 2005.

(6) For additional information on our managed portfolio and securitizations, refer to Note 9 of the Consolidated Financial Statements.

n/a = not applicable

Residential Mortgage

The residential mortgage portfolio makes up the largest percentage of our

consumer loan portfolio at 52 percent of held consumer loans and leases

and 43 percent of managed consumer loans and leases at December 31,

2006. Residential mortgages are originated for the home purchase and

refinancing needs of our customers in Global Consumer and Small Busi-

ness Banking and Global Wealth and Investment Management and repre-

sent 22 percent of the managed residential portfolio. The remaining 78

percent of the managed portfolio is in All Other, which includes Corporate

Treasury and Corporate Investments, and is comprised of purchased or

originated residential mortgage loans used to manage our overall ALM

activities.

On a held basis, outstanding loans and leases increased $58.6 bil-

lion in 2006 compared to 2005 driven by retained mortgage production

and bulk purchases. Nonperforming balances increased $90 million due to

portfolio seasoning. Loans past due 90 days or more and still accruing

interest of $118 million is related to repurchases pursuant to our servicing

agreements with Government National Mortgage Association (GNMA)

mortgage pools whose repayments are insured by the Federal Housing

Administration or guaranteed by the Department of Veterans Affairs. This

past due GNMA portfolio of $161 million was included in loans

held-for-sale at December 31, 2005 and was not reclassified to conform

to current presentation.

Credit Card – Domestic and Foreign

The consumer credit card portfolio is managed in Card Services within

Global Consumer and Small Business Banking. Outstandings in the held

domestic loan portfolio increased $2.6 billion in 2006 compared to 2005

due to the MBNA merger and organic growth partially offset by an increase

in net securitization activity. The $794 million increase in held domestic

loans past due 90 days or more and still accruing interest was driven by

portfolio seasoning, the trend toward more normalized delinquency levels

following bankruptcy reform and the addition of the MBNA portfolio, includ-

ing the adoption of MBNA collection practices and policies that have

historically led to higher delinquencies but lower losses. Net charge-offs

for the held domestic portfolio decreased $558 million to $3.1 billion, or

4.85 percent (5.00 percent excluding the impact of SOP 03-3) of total

average held credit card – domestic loans compared to 6.76 percent in

2005 primarily due to bankruptcy reform which accelerated charge-offs

into 2005. This decrease in net charge-offs was partially offset by new

advances on accounts for which previous loan balances were sold to the

securitization trusts, portfolio seasoning and the addition of the MBNA

portfolio. See the following discussion of the impact of SOP 03-3 on the

MBNA portfolio.

Managed domestic credit card outstandings increased $81.8 billion

to $142.6 billion at December 31, 2006, primarily due to the MBNA

merger. Managed net losses increased $1.3 billion to $5.4 billion, or 3.89

percent of total average managed domestic loans compared to 6.92 per-

cent in 2005. Managed net losses were higher primarily due to the addi-

tion of the MBNA portfolio and portfolio seasoning, partially offset by lower

bankruptcy-related losses as a result of bankruptcy reform. The 303 bps

decrease in the managed net loss ratio was driven by lower bankruptcy-

related losses and the beneficial impact of the higher credit quality of the

MBNA portfolio compared to the legacy Bank of America portfolio.

Held and managed outstandings in the foreign credit card portfolio of

$11.0 billion and $27.9 billion at December 31, 2006, as well as delin-

quencies, held net charge-offs and managed net losses, are related to the

addition of the MBNA portfolio. Net charge-offs for the held foreign portfo-

lio were $225 million, or 2.46 percent (3.05 percent excluding the impact

of SOP 03-3) of total average held credit card – foreign loans in 2006. Net

losses for the managed foreign portfolio were $980 million, or 3.95 per-

cent, of total average managed credit card – foreign loans. The foreign

64

Bank of America 2006