Bank of America 2006 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2006 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

|

|

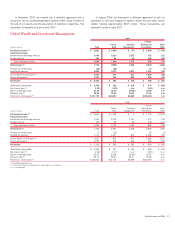

based on our determination that we are the primary beneficiary of the enti-

ties in accordance with FIN 46R. At December 31, 2006 and 2005, the

consolidated assets and liabilities of these conduits were reflected in AFS

Securities, Other Assets, and Commercial Paper and Other Short-term

Borrowings in Global Corporate and Investment Banking. At December 31,

2006 and 2005, we held $10.5 billion and $6.6 billion of assets of these

entities while our maximum loss exposure associated with these entities,

including unfunded lending commitments, was approximately $12.9 billion

and $8.3 billion. We manage our credit risk on the on-balance sheet

commitments by subjecting them to the same processes as the

off-balance sheet commitments.

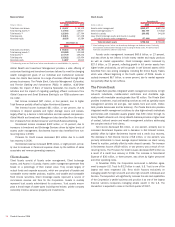

Commercial Paper Qualified Special Purpose

Entities

To manage our capital position and diversify funding sources, we will, from

time to time, sell assets to off-balance sheet entities that obtain financing

by issuing commercial paper or notes with similar repricing characteristics

to investors. These entities are Qualified Special Purpose Entities (QSPEs)

that have been isolated beyond our reach or that of our creditors, even in

the event of bankruptcy or other receivership. The accounting for these

entities is governed by SFAS 140, which provides that QSPEs are not

included in the consolidated financial statements of the seller. Assets

sold to the entities consist of high-grade corporate or municipal bonds,

collateralized debt obligations and asset-backed securities. These entities

issue collateralized commercial paper or notes with similar repricing char-

acteristics to third party market participants and enter into passive

derivative instruments with us. Assets sold to these entities typically have

an investment rating ranging from Aaa/AAA to Aa/AA. We may provide liq-

uidity, SBLCs or similar loss protection commitments to these entities, or

we may enter into derivatives with these entities in which we assume cer-

tain risks. The liquidity facility and derivatives have the same legal stand-

ing with the commercial paper.

The derivatives provide interest rate, currency and a pre-specified

amount of credit protection to the entity in exchange for the commercial

paper rate. These derivatives are provided for in the legal documents and

help to alleviate any cash flow mismatches. In some cases, if an asset’s

rating declines below a certain investment quality as evidenced by its

investment rating or defaults, we are no longer exposed to the risk of loss.

At that time, the commercial paper holders assume the risk of loss. In

other cases, we agree to assume all of the credit exposure related to the

referenced asset. Legal documents for each entity specify asset quality

levels that require the entity to automatically dispose of the asset once

the asset falls below the specified quality rating. At the time the asset is

disposed, we are required to reimburse the entity for any credit-related

losses depending on the pre-specified level of protection provided.

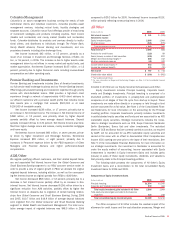

We manage any credit or market risk on commitments or derivatives

through normal underwriting and risk management processes. At

December 31, 2006 and 2005, we had off-balance sheet liquidity

commitments, SBLCs and other financial guarantees to these entities of

$7.6 billion and $7.1 billion, for which we received fees of $9 million and

$10 million for 2006 and 2005. Substantially all of these commitments

mature within one year and are included in Table 9. Derivative activity

related to these entities is included in Note 4 of the Consolidated Finan-

cial Statements.

We generally do not purchase any of the commercial paper issued by

these types of financing entities other than during the underwriting proc-

ess when we act as issuing agent nor do we purchase any of the commer-

cial paper for our own account. Derivative instruments related to these

entities are marked to market through the Consolidated Statement of

Income. SBLCs are initially recorded at fair value in accordance with FIN

45. Liquidity commitments and SBLCs subsequent to inception are

accounted for pursuant to SFAS 5 and are discussed further in Note 13 of

the Consolidated Financial Statements.

In addition, as a result of the MBNA merger on January 1, 2006, the

Corporation acquired interests in off-balance sheet credit card securitiza-

tion vehicles which issue both commercial paper and medium-term notes.

We hold subordinated interests issued by these entities, which are QSPEs,

but do not otherwise provide liquidity or other forms of loss protection to

these vehicles. For additional information on credit card securitizations,

see Note 9 of the Consolidated Financial Statements.

Credit and Liquidity Risks

Because we provide liquidity and credit support to the commercial paper

conduits and QSPEs described above, our credit ratings and changes

thereto will affect the borrowing cost and liquidity of these entities. In

addition, significant changes in counterparty asset valuation and credit

standing may also affect the liquidity of the commercial paper issuance.

Disruption in the commercial paper markets may result in the Corporation

having to fund under these commitments and SBLCs discussed above. We

seek to manage these risks, along with all other credit and liquidity risks,

within our policies and practices. See Notes 1 and 9 of the Consolidated

Financial Statements for additional discussion of off-balance sheet financ-

ing entities.

Other Off-Balance Sheet Financing Entities

To improve our capital position and diversify funding sources, we also sell

assets, primarily loans, to other off-balance sheet QSPEs that obtain

financing primarily by issuing term notes. We may retain a portion of the

investment grade notes issued by these entities, and we may also retain

subordinated interests in the entities which reduce the credit risk of the

senior investors. We may provide liquidity support in the form of foreign

exchange or interest rate swaps. We generally do not provide other forms

of credit support to these entities, which are described more fully in Note

9 of the Consolidated Financial Statements. In addition to the above, we

had significant involvement with VIEs other than the commercial paper

conduits. These VIEs were not consolidated because we will not absorb a

majority of the expected losses or expected residual returns and are there-

fore not the primary beneficiary of the VIEs. These entities are described

more fully in Note 9 of the Consolidated Financial Statements.

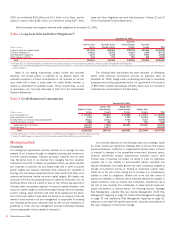

Obligations and Commitments

We have contractual obligations to make future payments on debt and

lease agreements. Additionally, in the normal course of business, we enter

into contractual arrangements whereby we commit to future purchases of

products or services from unaffiliated parties. Obligations that are legally

binding agreements whereby we agree to purchase products or services

with a specific minimum quantity defined at a fixed, minimum or variable

price over a specified period of time are defined as purchase obligations.

Included in purchase obligations are vendor contracts of $6.3 billion,

commitments to purchase securities of $9.1 billion and commitments to

purchase loans of $43.3 billion. The most significant of our vendor con-

tracts include communication services, processing services and software

contracts. Other long-term liabilities include our obligations related to the

Qualified Pension Plans, Nonqualified Pension Plans and Postretirement

Health and Life Plans (the Plans) as well as amounts accrued for

cardholder reward agreements. Obligations to the Plans are based on the

current and projected obligations of the Plans, performance of the Plans’

assets and any participant contributions, if applicable. During 2006 and

Bank of America 2006

57