Philips 2011 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2011 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

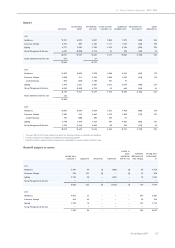

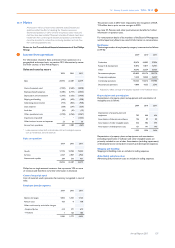

12 Group financial statements 12.10 - 12.10

Annual Report 2011 129

12.10 Significant accounting policies

The Consolidated financial statements have been prepared in

accordance with International Financial Reporting Standards (IFRS) as

endorsed by the European Union (EU). All standards and

interpretations issued by the International Accounting Standards Board

(IASB) and the IFRS Interpretations Committee effective year-end 2011

have been endorsed by the EU, except that the EU did not adopt some

paragraphs of IAS 39 applicable to certain hedge transactions. Philips

has no hedge transactions to which these paragraphs are applicable.

Consequently, the accounting policies applied by Philips also comply

fully with IFRS as issued by the IASB. These accounting policies have

been applied by group entities.

Certain comparative amounts in the Statement of income have been

reclassified to conform to the current year’s presentation. In addition,

the comparative Statement of income and statements of cash-flows

have been represented as if an operation discontinued during the

current year had been discontinued from the start of the comparative

years (See note 5, Discontinued operations and other assets classified

as held for sale and section 12.4, Consolidated statements of income,

of this Annual Report, section 12.7, Consolidated statements of cash

flows, of this Annual Report and section 12.9, Information by sector

and main country, of this Annual Report).

The Consolidated financial statements have been prepared under the

historical cost convention, unless otherwise indicated.

The Consolidated financial statements are presented in euros, which is

the Company’s presentation currency.

On February 23, 2012, the Board of Management authorized the

Consolidated financial statements for issue. The Consolidated financial

statements as presented in this report are subject to the adoption by

the Annual General Meeting of Shareholders.

Use of estimates

The preparation of the Consolidated financial statements in conformity

with IFRS requires management to make judgments, estimates and

assumptions that affect the application of accounting policies and the

reported amounts of assets, liabilities, income and expenses.

These estimates and assumptions affect the reported amounts of assets

and liabilities, the disclosure of contingent liabilities at the date of the

Consolidated financial statements, and the reported amounts of

revenues and expenses during the reporting period. We evaluate these

estimates and judgments on an ongoing basis and base our estimates

on experience, current and expected future conditions, third-party

evaluations and various other assumptions that we believe are

reasonable under the circumstances. The results of these estimates

form the basis for making judgments about the carrying values of assets

and liabilities as well as identifying and assessing the accounting

treatment with respect to commitments and contingencies. Actual

results may differ from these estimates.

Estimates significantly impact goodwill and other intangibles acquired,

tax on activities disposed, impairments, financial instruments, the

accounting for an arrangement containing a lease, revenue recognition

(multiple element arrangements), assets and liabilities from employee

benefit plans, other provisions and tax and other contingencies,

classification of assets and liabilities held for sale and the presentation

of items of profit and loss and cash-flows as continued or discontinued.

The fair values of acquired identifiable intangibles are based on an

assessment of future cash flows. Impairment analyses of goodwill and

indefinite-life intangible assets are performed annually and whenever a

triggering event has occurred to determine whether the carrying value

exceeds the recoverable amount. These analyses generally are based

on estimates of future cash flows.

The fair value of financial instruments that are not traded in an active

market is determined by using valuation techniques. The Company uses

its judgment to select from a variety of common valuation methods

including the discounted cash flow method and option valuation models

and to make assumptions that are mainly based on market conditions

existing at each balance sheet date.

Actuarial assumptions are established to anticipate future events and

are used in calculating pension and other postretirement benefit

expense and liability. These factors include assumptions with respect

to interest rates, expected investment returns on plan assets, rates of

increase in health care costs, rates of future compensation increases,

turnover rates, and life expectancy.

Basis of consolidation

The Consolidated financial statements include the accounts of

Koninklijke Philips Electronics N.V. (‘the Company’) and all subsidiaries

that fall under its power to govern the financial and operating policies

of an entity so as to obtain benefits from its activities. The existence

and effect of potential voting rights that are currently exercisable are

considered when assessing whether the Company controls another

entity. Subsidiaries are fully consolidated from the date that control

commences until the date that control ceases. All intercompany

balances and transactions have been eliminated in the Consolidated

financial statements. Unrealized losses are eliminated in the same way

as unrealized gains, but only to the extent that there is no evidence of

impairment.

Business combinations

Business combinations are accounted for using the acquisition method.

Under the acquisition method, the identifiable assets acquired, liabilities

assumed and any non-controlling interest in the acquiree are

recognized as at the acquisition date, which is the date on which control

is transferred to the Company. Control is the power to govern the

financial and operating policies of an entity so as to obtain benefits from

its activities. In assessing control, the Company takes into consideration

potential voting rights that currently are exercisable.

For acquisitions on or after January 1, 2010, the Company measures

goodwill at the acquisition date as:

• the fair value of the consideration transferred; plus

• the recognized amount of any non-controlling interest in the

acquiree;

• plus if the business combination is achieved in stages, the fair value

of the existing equity interest in the acquiree;

• less the net recognized amount (generally fair value) of the

identifiable assets acquired and liabilities assumed.

When the excess is negative, a bargain purchase gain is recognized

immediately in profit or loss (hereafter referred to as the Statement of

income).

The consideration transferred does not include amounts related to the

settlement of pre-existing relationships. Such amounts are generally

recognized in the Statement of income.

Costs related to the acquisition, other than those associated with the

issue of debt or equity securities, that the Company incurs in

connection with a business combination are expensed as incurred.

Acquisitions between January 1, 2004 and January 1, 2010

For acquisitions between January 1, 2004 and January 1, 2010, goodwill

represents the excess of the cost of the acquisition over the Company’s

interest in the recognized amount (generally fair value) of the

identifiable assets, liabilities and contingent liabilities of the acquiree.

Transaction costs, other than those associated with the issue of debt

or equity securities, that the Company incurred in connection with

business combinations were capitalized as part of the cost of the

acquisition.

Acquisitions of Non-controlling interests

Acquisitions of non-controlling interests are accounted for as

transactions with owners in their capacity as owners and therefore no

goodwill is recognized as a result. Adjustments to non-controlling

interests arising from transactions that do not involve the loss of

control are based on a proportionate amount of the net assets of the

subsidiary.

For changes to non-controlling interest without the loss of control, the

difference between such change and any consideration paid or received

is recognized directly in equity.

Loss of control

Upon the loss of control, the Company derecognizes the assets and

liabilities of the subsidiary, any non-controlling interests and the other

components of equity related to the subsidiary. Any surplus or deficit

arising on the loss of control is recognized in profit or loss. If the

Company retains any interest in the previous subsidiary, then such