Philips 2011 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2011 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

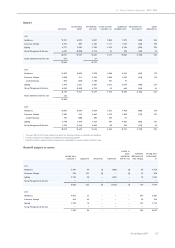

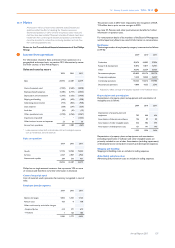

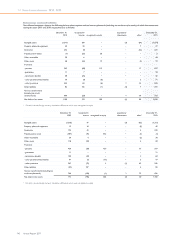

12 Group financial statements 12.10 - 12.10

136 Annual Report 2011

and the distinction between short-term and other long-term benefits

has been revised. The revisions further clarify the classification of

various costs involved in benefit plans like expenses and taxes.

The amendment will have a material impact on income from operations

and net income of the Company, resulting from the changes in

measurement and reporting of expected returns on plan assets (and

interest costs), which is currently reported under income from

operations.

The revised standard requires interest income or expense to be

calculated on the net balance recognized, with the rate used to discount

the defined benefit obligations.

There is no impact on the cash flow statement and the balance sheet,

since the Company already applies immediate recognition of actuarial

gains and losses. The impact on net income leads to lower amount

recognized in actuarial gains and losses in equity.

The impact was determined by applying the revised IAS 19R on current

post employment benefit plans, excluding long term plans not requiring

actuarial valuations and projecting it to 2013. The estimated negative

impacts on EBITA and income before tax for 2013 would be:

EBITA EUR (260) million

Financial income and expenses EUR (90) million

Income before tax EUR (350) million

IFRS 9 ‘Financial Instruments’

The standard introduces certain new requirements for classifying and

measuring financial assets and liabilities. IFRS 9 divides all financial assets

that are currently in the scope of IAS 39 into two classifications, those

measured at amortized cost and those measured at fair value. The

standard along with proposed expansion of IFRS 9 for classifying and

measuring financial liabilities, de-recognition of financial instruments,

impairment, and hedge accounting will be applicable from January 1,

2015, although entities are permitted to adopt earlier. This standard

has not yet been endorsed by the EU. The new standard will primarily

impact the accounting for the available-for-sale securities within Philips

and will, accordingly, change the timing and placement (profit or loss

versus other comprehensive income) of changes in the respective fair

value. The actual impact in the year it is applied cannot be estimated

on a reasonable basis.

IFRS 10 ‘Consolidated Financial Statements’

IFRS 10 replaces the consolidation requirements in SIC-12

Consolidation—Special Purpose Entities and IAS 27 Consolidated and

Separate Financial Statements. IFRS 10 changes the definition of control

so the same criteria are applied to all entities to determine control. The

revised definition of control focuses on the need to have both power

and variable returns before control is present. The new standard

includes guidance on control with less than half of the voting rights

(‘de-facto’ control), participating and protective voting rights and agent/

principal relationships. This new standard will be applicable from

January 1, 2013, but has not yet been endorsed by the EU. The

Company is currently evaluating the impact that this new standard will

have on the Company’s Consolidated financial statements.

The Company is currently assessing the potential other new standards,

amendments to standards and interpretations that are effective for

annual periods on or after January 1, 2012 and which the Company has

not early adopted. None of these are expected to have a material effect

on the Company’s Consolidated financial statements.