BB&T 2011 Annual Report Download

Download and view the complete annual report

Please find the complete 2011 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

Annual Report Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

For the fiscal year ended:

December 31, 2011

Commission File Number: 1-10853

BB&T CORPORATION

(Exact name of Registrant as specified in its Charter)

North Carolina 56-0939887

(State of Incorporation) (I.R.S. Employer Identification No.)

200 West Second Street

Winston-Salem, North Carolina 27101

(Address of principal executive offices) (Zip Code)

(336) 733-2000

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Securities Exchange Act of 1934:

Title of each class

Name of each exchange

on which registered

Common Stock, $5 par value New York Stock Exchange

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities

Act. YES ÍNO ‘

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the

Act YES ‘NO Í

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the

Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file

such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ÍNO ‘

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if

any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of

this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and

post such files). Yes ÍNo ‘

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained

herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements

incorporated by references in Part III of this Form 10-K or any amendment to this Form 10-K. Í

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer,

or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting

company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ÍAccelerated filer ‘

Non-accelerated filer ‘(Do not check if a smaller reporting company) Smaller reporting company ‘

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the

Act). YES ‘NO Í

At January 31, 2012, the Corporation had 697,228,764 shares of its Common Stock, $5 par value, outstanding. The

aggregate market value of voting stock held by nonaffiliates of the Corporation is approximately $18.6 billion (based on

the closing price of such stock as of June 30, 2011).

Table of contents

-

Page 1

... fiscal year ended: Commission File Number: 1-10853 December 31, 2011 BB&T CORPORATION (Exact name of Registrant as specified in its Charter) North Carolina (State of Incorporation) 56-0939887 (I.R.S. Employer Identification No.) 200 West Second Street Winston-Salem, North Carolina (Address of... -

Page 2

...Officers and Corporate Governance Executive Compensation Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters Certain Relationships and Related Transactions, and Director Independence Principal Accounting Fees and Services PART IV Item 15 Exhibits, Financial... -

Page 3

..." in the Registrant's Proxy Statement for the 2012 Annual Meeting of Shareholders. For information regarding the registrant's securities authorized for issuance under equity compensation plans, refer to "Equity Compensation Plan Information" in Part II. The other information required by Item 12 is... -

Page 4

... of BB&T's customers to access the financial services BB&T offers; expected cost savings associated with completed mergers and acquisitions may not be fully realized or realized within the expected time frames; and deposit attrition, customer loss and/or revenue loss following completed mergers and... -

Page 5

... Real Estate Capital, LLC, based in Charlotte, North Carolina, which specializes in arranging and servicing commercial mortgage loans; Lendmark Financial Services, Inc., located in Covington, Georgia, which offers alternative consumer loans to clients unable to meet Branch Bank's normal credit... -

Page 6

...; and facilitates the origination, trading and distribution of fixed-income securities and equity products in both the public and private capital markets. It also has a public finance department that provides investment banking, financial advisory services and debt underwriting services to a variety... -

Page 7

...finance Home equity lending Home mortgage lending Insurance Investment brokerage services Mobile/online banking Payment solutions Retail deposit services Sales finance Small business lending Wealth management/private banking Commercial Services: Asset management Association services Capital markets... -

Page 8

... provide market diversification; any credit-related issues would need to be addressed; and acquisitions must meet BB&T's financial criteria - earnings per share should be accretive in Year 1, excluding merger-related charges, but including full run rate synergies; the internal rate of return should... -

Page 9

... large financial companies to avoid market disruption; applying the same leverage and risk-based capital requirements that apply to insured depository institutions to most bank holding companies, savings and loan holding companies and systemically important nonbank financial companies; limiting the... -

Page 10

...holding company has not maintained a satisfactory CRA rating, the company will not be able to commence any new financial activities or acquire a company that engages in such activities, although the company will still be allowed to engage in activities closely related to banking and make investments... -

Page 11

...period of time, not to exceed five years; and subject to certain deposit market-share limitations. After a bank has established branches in a state through an interstate merger transaction, the bank may establish and acquire additional branches at any location in the state where a bank headquartered... -

Page 12

... from dividends paid to BB&T by Branch Bank. The Banks are subject to laws and regulations that limit the amount of dividends they can pay. In addition, BB&T and the Banks are subject to various regulatory restrictions relating to the payment of dividends, including requirements to maintain capital... -

Page 13

...preferred stock and a limited amount of the allowance for credit losses. This is called "Tier 2 capital." Tier 1 capital and Tier 2 capital combined are referred to as total regulatory capital. The Federal Reserve requires bank holding companies that engage in trading activities to adjust their risk... -

Page 14

... of assessment rates for certain institutions. Under the current system, premiums are assessed quarterly. In addition, insured deposits have been required to pay a pro rata portion of the interest due on the obligations issued by the Financing Corporation ("FICO") to fund the closing and disposal... -

Page 15

... population. These laws include the Equal Credit Opportunity Act, the Fair Credit Reporting Act, the Truth in Lending Act, the Home Mortgage Disclosure Act, the Real Estate Settlement Procedures Act, and their respective state law counterparts. The Dodd-Frank Act created a new, independent federal... -

Page 16

... with customers that overdraw their accounts more than six times during a rolling 12-month period. The additional guidance also imposes daily limits on overdraft charges, requires institutions to review and modify check-clearing procedures, prominently distinguish account balances from available... -

Page 17

... Ethics for Directors or Senior Financial Officers on BB&T's web site at www.BBT.com/Investor. NYSE Certification The annual certification of BB&T's Chief Executive Officer required to be furnished to the NYSE pursuant to Section 303A.12(a) of the NYSE Listed Company Manual was previously filed with... -

Page 18

...Enterprise Risk Manager Donna C. Goodrich Senior Executive Vice President and Deposit Services Manager Robert E. Greene Senior Executive Vice President and Administrative Group Manager Clarke R. Starnes III Senior Executive Vice President and Chief Risk Officer 35 56 Enterprise Risk Manager since... -

Page 19

...with falling home prices and increasing foreclosures and unemployment, resulted in significant write-downs of asset values by many financial institutions, including government-sponsored entities and major commercial and investment banks. These write-downs, initially of mortgage-backed securities but... -

Page 20

... an agreement with the Federal Deposit Insurance Corporation ("FDIC") to acquire certain assets and assume substantially all of the deposits and certain liabilities of Colonial Bank, an Alabama state-chartered bank headquartered in Montgomery, Alabama ("Colonial"). As a result, Branch Bank acquired... -

Page 21

...loans acquired in the Colonial transaction, the negative economic aspects of these risks are mitigated as a result of the FDIC loss sharing agreements. BB&T's liquidity could be impaired by an inability to access the capital markets, an unforeseen outflow of cash or a reduction in the credit ratings... -

Page 22

... regulation of the financial services industry, addressing, among other things, systemic risk, capital adequacy, deposit insurance assessments, consumer financial protection, interchange fees, derivatives, lending limits, and changes among the bank regulatory agencies. During 2011, federal agencies... -

Page 23

... its products and services in order to maintain market share. There is intense competition among commercial banks in BB&T's market area. In addition, BB&T competes with other providers of financial services, such as savings and loan associations, credit unions, consumer finance companies, securities... -

Page 24

... from BB&T's actual or alleged conduct in any number of activities, including lending practices, corporate governance and acquisitions, activities related to asset sales and balance sheet management and from actions taken by government regulators and community organizations in response to those... -

Page 25

... an acquired company may cause BB&T not to realize expected revenue increases, cost savings, increases in geographic or product presence and/or other projected benefits from the acquisition. The integration could result in higher than expected deposit attrition, loss of key employees, disruption... -

Page 26

... office space used as the Corporation's headquarters in Winston-Salem, North Carolina. At December 31, 2011, Branch Bank operated 1,779 branch offices in North Carolina, South Carolina, Virginia, Maryland, Georgia, West Virginia, Tennessee, Kentucky, Alabama, Florida, Texas, Indiana and Washington... -

Page 27

... Floating Rate Junior Subordinated Debentures due 2077 Company's 6.75% junior subordinated debentures due 2036 underlying the 6.75% capital securities of BB&T Capital Trust II Share Repurchases BB&T has periodically repurchased shares of its own common stock. In accordance with North Carolina law... -

Page 28

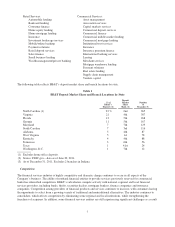

... comparing the total returns (assuming reinvestment of dividends) of BB&T Common Stock, the S&P 500 Index, and an Industry Peer Group Index. The graph assumes $100 invested on December 31, 2006 in BB&T Common Stock and in each of the indices. In 2011, the financial holding companies in the Industry... -

Page 29

...Year Cumulative Total Return* Among BB&T Corporation, the S&P 500 Index, and BB&T's Peer Group 150 Dollars 100 50 0 12/06 12/07 12/08 12/09 12/10 12/11 BB&T Corporation S&P 500 BB&T's Peer Group * $100 invested on 12/31/06 in stock or index, including reinvestment of dividends. Fiscal year... -

Page 30

... stock Net income available to common shareholders Per Common Share: Average shares outstanding: Basic Diluted Earnings: Basic Diluted Cash dividends declared (2) Book value Average Balances: Securities, at amortized cost Loans and leases (3) Other assets Total assets Deposits Long-term debt... -

Page 31

... with less exposure to higher-risk real estate loans Strong performance in specialized lending, large corporate banking, wealth management, payment services, direct retail lending and mortgage production Continued to enhance risk management structure Challenges BB&T's business has become more... -

Page 32

... and complex benefits administration. Atlantic Risk is a commercial property and casualty and employee benefits broker that provides risk management consulting and a full array of business insurance products and services. Precept serves middle-market and large corporate clients, ranging from 50... -

Page 33

... liabilities are financial instruments carried at fair value. This includes securities available for sale, trading securities, derivatives, certain loans held for sale, residential mortgage servicing rights and venture capital investments. At December 31, 2011, the percentage of total assets and... -

Page 34

.... The pricing service uses observable inputs when available including benchmark yields, reported trades, broker-dealer quotes, issuer spreads, benchmark securities, bids and offers. These values take into account recent market activity as well as other market observable data such as interest rate... -

Page 35

... future cash flows or the discount rate for each reporting unit. Pension and Postretirement Benefit Obligations BB&T offers various pension plans and postretirement benefit plans to employees. The calculation of the obligations and related expenses under these plans requires the use of actuarial... -

Page 36

... to the higher yield assets acquired in the Colonial acquisition and lower funding costs. Management expects the net interest margin to be in the 3.85% to 3.95% range in the first quarter of 2012 due to runoff of the covered loan portfolio, lower investment yields, and an overall lower interest rate... -

Page 37

... income for 2011 on loans and securities acquired in the Colonial acquisition increased $149 million compared to 2010, which was offset by a decrease in FDIC loss share income. The majority of the increase is related to loans and reflects higher expected cash flows based on the quarterly cash flow... -

Page 38

... of decreased loss projections on covered loans. The following table sets forth the major components of net interest income and the related annualized yields and rates for 2011, 2010 and 2009, as well as the variances between the periods caused by changes in interest rates versus changes in volumes... -

Page 39

... for sale and securities held to maturity. Includes Federal funds sold, securities purchased under resale agreements or similar arrangements, interest-bearing deposits with banks, trading securities, FHLB stock and other earning assets. Loan fees, which are not material for any of the periods shown... -

Page 40

... 2009 Insurance income $ Service charges on deposits Mortgage banking income Investment banking and brokerage fees and commissions Checkcard fees Bankcard fees and merchant discounts Trust and investment advisory revenues Income from bank-owned life insurance FDIC loss share income, net Securities... -

Page 41

... in noninterest revenue was due to fewer securities gains, lower income related to the FDIC loss share receivable, lower service charges on deposit accounts and lower mortgage banking revenues, while bankcard fees and merchant discounts and trust and investment advisory revenues grew compared to the... -

Page 42

...held for sale portfolio in connection with management's nonperforming loan disposition strategy. Noninterest revenue sources have been negatively impacted by many regulatory initiatives over the past several years, including changes to Regulation E, posting order of client transactions and limits on... -

Page 43

... improved performance and production-related businesses. Pension and employee benefits expense was up $21 million, largely due to higher pension expense. Management expects pension expense to be approximately $70 million higher in 2012 due to the change in the discount rate. Total personnel expense... -

Page 44

... and the sale of duplicate facilities and equipment; and other merger-related and restructuring charges or credits, which include expenses necessary to convert and combine the acquired branches and operations of merged companies, direct media advertising related to the acquisitions, asset and supply... -

Page 45

...tax rate and a discussion of uncertain tax positions and other tax matters. Segment Results BB&T's operations are divided into six reportable business segments: Community Banking, Residential Mortgage Banking, Dealer Financial Services, Specialized Lending, Insurance Services, and Financial Services... -

Page 46

... billion in 2011, primarily due to higher losses on commercial loans held for sale, lower overdraft fees, and lower checkcard fees. This decline in noninterest income was offset by increases in merchant discounts, deposit account service charges, account analysis fees, and credit card interchange... -

Page 47

... the sale of problem loans in connection with management's nonperforming loan disposition strategy. Noninterest income in Residential Mortgage Banking declined $109 million, or 23.9%, to $348 million in 2011. This decrease was due to lower mortgage loan sale volumes and margins than the prior year... -

Page 48

... and administrative solutions firm with offices in Irvine and San Ramon, California; Liberty Benefit Insurance Services, a full-service employee benefits broker located in San Jose, California; and Atlantic Risk Management Corporation, a commercial property and casualty and employee benefits broker... -

Page 49

...overall funds management objectives; (ii) to provide eligible securities to secure public funds, trust deposits as prescribed by law and other borrowings; and (iii) to earn the maximum return on funds invested that is commensurate with meeting the requirements of (i) and (ii). Branch Bank invests in... -

Page 50

... 31, 2011, the available-for-sale securities portfolio also includes $1.6 billion of securities that were acquired from the FDIC as part of the Colonial acquisition. These securities are covered by FDIC loss sharing agreements and include $1.3 billion of non-agency mortgage-backed securities and... -

Page 51

...a rising rate environment and achieve a better mix of earning assets. In connection with this strategy, management reduced the balance sheet by approximately $8 billion through the sale of securities. During the third and fourth quarters of 2010, management executed a strategy to further de-risk the... -

Page 52

... federal income tax rate of 35%. Yields for available-for-sale securities are calculated based on the amortized cost of the securities. (2) For purposes of the maturity table, mortgage-backed securities, which are not due at a single maturity date, have been included in maturity groupings based on... -

Page 53

..., sales finance, revolving credit, residential mortgage and other lending subsidiaries. In addition, BB&T has a portfolio of loans that were acquired in the Colonial acquisition that are covered by FDIC loss sharing agreements. BB&T lends to a diverse customer base that is substantially located... -

Page 54

... December 31, 2011 Commercial, Financial and Agricultural Loans Real Estate: Construction and Land Development Loans (Dollars in millions) Total Fixed Rate: 1 year or less (1) 1-5 years After 5 years Total Variable Rate: 1 year or less (1) 1-5 years After 5 years Total Total loans and leases... -

Page 55

... Loan and Lease Portfolio Based on Lines of Business December 31, 2011 2010 2009 (Dollars in millions) 2008 2007 Commercial loans and leases Direct retail lending Sales finance Revolving credit Residential mortgage Other lending subsidiaries Other acquired Total loans and leases held for investment... -

Page 56

..., 2011 Balance % of total Balance (Dollars in millions) 2010 % of total Commercial loans and leases: Commercial and industrial Commercial real estate - other Commercial real estate - residential ADC Direct retail lending Sales finance Revolving credit Residential mortgage Other lending subsidiaries... -

Page 57

... level charge-offs related to the acquired loans are not recognized in the financial statements until the cumulative amounts exceed the original loss projections on a pool basis, the net charge-off ratio for the acquired loans is not consistent with the net charge-off ratio for other loan portfolios... -

Page 58

... real estate (3) Other foreclosed property Total nonperforming assets (excluding covered assets) (1)(2)(3) Loans 90 days or more past due and still accruing: Commercial loans and leases Direct retail lending Sales finance loans Revolving credit loans Residential mortgage loans (4)(5) Other lending... -

Page 59

... foreclosed real estate totaling $378 million, $313 million and $160 million at December 31, 2011, 2010 and 2009, respectively, that are covered by FDIC loss sharing agreements. (4) Excludes mortgage loans guaranteed by GNMA that BB&T does not have the obligation to repurchase that are 90 days or... -

Page 60

... of these ratios and they may not be comparable to other periods presented or to other portfolios that were not impacted by acquisition accounting. Nonperforming assets, which includes foreclosed real estate, repossessions, nonaccrual loans and certain restructured loans, totaled $2.8 billion... -

Page 61

... family residential and commercial real estate, had an average holding period of 11 months. Loans 90 days or more past due and still accruing interest, excluding government guaranteed loans and loans covered by FDIC loss share agreements, totaled $202 million at December 31, 2011, compared with $295... -

Page 62

... a new loan. Alternatively, such loans may be considered for reclassification in years subsequent to the date of the re-modification based on the passage of time as described in the preceding paragraph. In connection with consumer loan restructurings, a nonperforming loan will be returned to... -

Page 63

... 30-89 Days (1) 90 Days Or More (1) (Dollars in millions) Current Status Total Performing restructurings: Commercial: Commercial and industrial Commercial real estate - other Commercial real estate residential ADC Direct retail lending Sales finance Revolving credit Residential mortgage (2) Other... -

Page 64

... category Amount Amount Amount Amount Amount (Dollars in millions) Balances at end of period applicable to: Commercial loans and leases $ 1,053 Direct retail lending 232 Sales finance 38 Revolving credit 112 Residential mortgage 365 Other lending subsidiaries 197 Covered 149 Unallocated 110... -

Page 65

... 31, 2011 2010 2009 (Dollars in millions) 2008 2007 Allowance For Credit Losses Beginning balance Provision for credit losses (excluding covered loans) Provision for covered loans Charge-offs: Commercial loans and leases (1) Direct retail lending Sales finance Revolving credit Residential mortgage... -

Page 66

... 24 Real Estate Lending Portfolio Credit Quality and Geographic Distribution Commercial Real Estate Loan Portfolio (1) (2) As of / For the Period Ended December 31, 2011 Commercial Real Estate - Residential ADC Builder / Construction Land / Land Development Condos / Townhomes Total ADC (Dollars in... -

Page 67

Applicable ratios are annualized. (1) Commercial real estate loans (CRE) are defined as loans to finance non-owner occupied real property where the primary repayment source is the sale or rental/lease of the real property. Definition is based on internal classification. Excludes covered loans and in... -

Page 68

...-Date Direct Retail 1-4 Family and Lot/Land Real Estate Loans and Lines By State of Origination Total Outstandings (Dollars in millions) North Carolina Virginia Other Total $ 4,435 3,009 5,842 13,286 1.18 % 0.66 1.16 1.05 1.99 % 0.89 2.39 1.92 1.68 % 0.61 1.83 1.50 $ Applicable ratios... -

Page 69

... checking accounts, savings accounts, money market deposit accounts, certificates of deposit and individual retirement accounts. Deposit account terms vary with respect to the minimum balance required, the time period the funds must remain on deposit and service charge schedules. Interest rates paid... -

Page 70

... year-end 2010. In addition, interest checking and money market and savings accounts represented a higher percentage of total deposits, while certificates of deposit and foreign office deposits declined. The growth in deposits was largely driven by commercial and public funds clients, as some higher... -

Page 71

...in a manner that aids in the management of interest rate risk and liquidity. Shareholders' Equity Shareholders' equity totaled $17.5 billion at December 31, 2011, an increase of $982 million, or 6.0%, from year-end 2010. BB&T's book value per common share at December 31, 2011 was $24.98, compared to... -

Page 72

... value of the available for sale securities portfolio, partially offset by declines of $235 million related to pensions and other post-retirement benefit plans and $112 million in unrecognized losses on cash flow hedges. BB&T's tangible shareholders' equity available to common shareholders was $11... -

Page 73

... loan portfolio. BB&T's commercial lending program is generally targeted to serve small-to-middle market businesses with sales of $250 million or less. In addition, BB&T's Corporate Banking Group provides lending solutions to large corporate clients. Traditionally, lending to small and mid-sized... -

Page 74

... home equity lines of credit. Direct retail loans are subject to the same rigorous lending policies and procedures as described above for commercial loans and are underwritten with note amounts and credit limits that ensure consistency with the Corporation's risk philosophy. Sales Finance Loan... -

Page 75

... by loss sharing agreements are primarily commercial real estate loans and residential mortgage loans. Refer to Note 3 "Loans and Leases" in the "Notes to Consolidated Financial Statements" in this report for additional disclosures related to BB&T's covered loans. Liquidity risk Liquidity risk is... -

Page 76

...to manage economic risk related to securities, commercial loans, mortgage servicing rights and mortgage banking operations, long-term debt and other funding sources. BB&T also uses derivatives to facilitate transactions on behalf of its clients. As of December 31, 2011, BB&T had derivative financial... -

Page 77

... earnings to changes in interest rates. The Simulation model projects net interest income and interest rate risk for a rolling two-year period of time. Simulation takes into account the current contractual agreements that BB&T has made with its customers on deposits, borrowings, loans, investments... -

Page 78

... of loan commitments. In addition to the level of liquid assets, such as cash, cash equivalents and securities available for sale, many other factors affect the ability to meet liquidity needs, including access to a variety of funding sources, maintaining borrowing capacity in national money markets... -

Page 79

... capital markets through issuance of senior or subordinated bank notes and institutional certificates of deposit, access to the FHLB system, dealer repurchase agreements and repurchase agreements with commercial clients, access to the overnight and term Federal funds markets, use of a Cayman branch... -

Page 80

...to these projects, of which $76 million had been funded. BB&T's risk exposure relating to such commitments is generally limited to the amount of investments and loan commitments made. Refer to Note 1 "Summary of Significant Accounting Policies" in the "Notes to Consolidated Financial Statements" for... -

Page 81

... risk exposure relating to such commitments is generally limited to the amount of investments and future funding commitments made. Merger and acquisition agreements of businesses other than financial institutions occasionally include additional incentives to the acquired entities to offset the loss... -

Page 82

... Ratio Tangible Capital Ratio Tier 1 Common Equity Ratio 8.50 % 11.50 % 6.50 % 5.50 % 7.00 % Payments of cash dividends to BB&T's shareholders and repurchases of common shares are the methods used to manage any excess capital generated. In addition, management closely monitors the Parent Company... -

Page 83

... tax assets and unconsolidated investments. Refer to Table 37 for a reconciliation of how BB&T calculates the Tier 1 common equity ratio under the proposed Basel III capital guidelines. Table 36 Capital Ratios December 31, 2011 2010 (Dollars in millions, except per share data) Risk-based: Tier... -

Page 84

... III Capital Ratios (1) December 31, 2011 (Dollars in millions) Tier 1 common equity under Basel I definition Adjustments: Other comprehensive income related to AFS securities, defined benefit pension and other postretirement employee benefit plans Deduction for net defined benefit pension asset... -

Page 85

... to quarterly periods in the years ended December 31, 2011 and 2010. Table 38 Quarterly Financial Summary-Unaudited 2011 Fourth Quarter Third Quarter Second First Fourth Third Quarter Quarter Quarter Quarter (Dollars in millions, except per share data) 2010 Second Quarter First Quarter Consolidated... -

Page 86

... on that evaluation, the Chief Executive Officer and Chief Financial Officer concluded that the Corporation's disclosure controls and procedures are effective. There was no change in the Corporation's internal control over financial reporting that occurred during the fourth quarter of 2011 that has... -

Page 87

... or timely detection of unauthorized acquisition, use, or disposition of the company's assets that could have a material effect on the financial statements. Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of... -

Page 88

BB&T CORPORATION AND SUBSIDIARIES CONSOLIDATED BALANCE SHEETS December 31, 2011 and 2010 (Dollars in millions, except per share data, shares in thousands) 2011 Assets Cash and due from banks Interest-bearing deposits with banks Federal funds sold and securities purchased under resale agreements or ... -

Page 89

... AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF INCOME Years Ended December 31, 2011, 2010 and 2009 (Dollars in millions, except per share data, shares in thousands) 2011 Interest Income Interest and fees on loans and leases Interest and dividends on securities Interest on other earning assets Total... -

Page 90

... Net change in other comprehensive income (loss) Total comprehensive income (loss) (Note 12) Stock transactions: In purchase acquisitions (1) In connection with equity awards, net of repurchases In connection with dividend reinvestment plan In connection with 401(k) plan In common stock offerings... -

Page 91

...premises and equipment Proceeds from sales of foreclosed property or other real estate held for sale Other, net Net cash from investing activities Cash Flows From Financing Activities: Net change in deposits Net change in federal funds purchased, securities sold under repurchase agreements and short... -

Page 92

...and public entities. Branch Bank offers, either directly, or through its subsidiaries, lease financing to businesses and municipal governments; factoring; discount brokerage services, annuities and mutual funds; life insurance, property and casualty insurance, health insurance and commercial general... -

Page 93

... the market price of the stock as of the closing of the acquisition. In connection with mergers and acquisitions, BB&T may issue options to purchase shares of its common stock in exchange for options to purchase shares of the acquired entities that are outstanding at the time the merger is completed... -

Page 94

...income on trading account securities is included in interest and dividends from other earning assets. Loans Held for Sale BB&T accounts for new originations of prime residential mortgage and commercial mortgage loans held for sale at fair value. BB&T accounts for the derivatives used to economically... -

Page 95

... foreclosed property. Foreclosed property consists of real estate and other assets acquired as a result of customers' loan defaults. BB&T's policies related to when loans are placed on nonaccrual status conform to guidelines prescribed by bank regulatory authorities. The majority of commercial loans... -

Page 96

... includes direct retail lending, revolving credit, mortgage, sales finance and other loans originated by certain retail-oriented subsidiaries, and was identified based on the delinquency-based approach used to estimate the allowance for these loans. The covered and other acquired portfolio segment... -

Page 97

...sheet date. In connection with this process, BB&T establishes reserves related to these loans that are calculated using an expected cash flow approach. These discounted cash flow analyses incorporate adjustments to future cash flows that reflect management's best estimate of the default risk related... -

Page 98

...foreign exchange contracts and options written and purchased. BB&T uses derivatives primarily to manage economic risk related to securities, commercial loans, mortgage servicing rights and mortgage banking operations, long-term debt and other funding sources. BB&T also uses derivatives to facilitate... -

Page 99

... periods of time. To the extent that BB&T's interest rate lock commitments relate to loans that will be held for sale upon funding, they are also accounted for as derivatives, with gains or losses included in mortgage banking income. Gains and losses on other derivatives used to manage economic risk... -

Page 100

... rates that would be used by market participants based on the risks involved. Gains and losses incurred on loans sold to third party investors are included in mortgage banking income in the Consolidated Statements of Income. BB&T also periodically securitizes mortgage loans that it intends to hold... -

Page 101

.... It eliminates differences between GAAP and International Financial Reporting Standards issued by the International Accounting Standards Board. New disclosures required by the guidance include: quantitative information about the significant unobservable inputs used for Level 3 measurements... -

Page 102

... $ 500 13,037 33 528 14,098 $ Amortized Cost Gross Unrealized Gains Losses Fair Value (Dollars in millions) Securities available for sale: GSE securities Mortgage-backed securities issued by GSE States and political subdivisions Non-agency mortgage-backed securities Other securities Covered... -

Page 103

..., respectively, were pledged to secure municipal deposits, securities sold under agreements to repurchase, other borrowings, and for other purposes as required or permitted by law. BB&T had certain investments in marketable debt securities and mortgage-backed securities issued by Fannie Mae and... -

Page 104

..., at the dates presented: Less than 12 months Fair Unrealized Value Losses December 31, 2011 12 months or more Fair Unrealized Value Losses (Dollars in millions) Total Unrealized Losses Fair Value Securities available for sale: GSE securities $ Mortgage-backed securities issued by GSE States and... -

Page 105

...evaluates credit impairment related to mortgage-backed securities through the use of cash flow modeling. These models give consideration to long-term macroeconomic factors applied to current security default rates, prepayment rates and recovery rates and security-level performance. During 2011, OTTI... -

Page 106

...31, 2011 and 2010: December 31, 2011 2010 (Dollars in millions) Loans and leases, net of unearned income: Commercial: Commercial and industrial Commercial real estate - other Commercial real estate - residential ADC (1) Direct retail lending Sales finance Revolving credit Residential mortgage Other... -

Page 107

...credit losses for certain acquired loan pools. The following table provides a summary of BB&T's nonperforming assets and loans 90 days or more past due and still accruing as of December 31, 2011 and 2010: December 31, 2011 2010 (Dollars in millions) Nonaccrual loans and leases: Held for investment... -

Page 108

...: December 31, 2011 2010 (Dollars in millions) Performing restructurings: Commercial: Commercial and industrial Commercial real estate - other Commercial real estate - residential ADC Direct retail lending Sales finance Revolving credit Residential mortgage (1)(2) Other lending subsidiaries Total... -

Page 109

... Ending Balance (Dollars in millions) Commercial: Commercial and industrial Commercial real estate - other Commercial real estate - residential ADC Other lending subsidiaries Retail: Direct retail lending Revolving credit Residential mortgage Sales finance Other lending subsidiaries Covered and... -

Page 110

... Loans Acquired With Deteriorated Credit Quality Total (Dollars in millions) Commercial: Commercial and industrial Commercial real estate - other Commercial real estate - residential ADC Other lending subsidiaries Retail: Direct retail lending Revolving credit Residential mortgage Sales finance... -

Page 111

... Loans Acquired With Deteriorated Credit Quality Total (Dollars in millions) Commercial: Commercial and industrial Commercial real estate - other Commercial real estate - residential ADC Other lending subsidiaries Retail: Direct retail lending Revolving credit Residential mortgage Sales finance... -

Page 112

... for investment. Covered and other acquired loans are excluded from this analysis because their related allowance is determined by loan pool performance due to the application of the accretion method. December 31, 2011 Commercial Real Estate Other Commercial Real Estate Residential ADC Other Lending... -

Page 113

... Covered Loans Current (Dollars in millions) Commercial: Commercial and industrial $ 35,746 $ Commercial real estate - other 10,273 Commercial real estate - residential ADC 1,671 Other lending subsidiaries 3,589 Retail: Direct retail lending Revolving credit Residential mortgage (2) Sales finance... -

Page 114

... Direct retail lending Residential mortgage (1) Sales finance Other lending subsidiaries With An Allowance Recorded: Commercial: Commercial and industrial Commercial real estate - other Commercial real estate - residential ADC Other lending subsidiaries Retail: Direct retail lending Revolving credit... -

Page 115

... Rate (2) Structure Increase To Allowance (Dollars in millions) Commercial: Commercial and industrial Commercial real estate - other Commercial real estate - residential ADC Other lending subsidiaries Retail: Direct retail lending Revolving credit Residential mortgage Sales finance Other lending... -

Page 116

... Ended December 31, 2011 (Dollars in millions) Commercial: Commercial and industrial Commercial real estate - other Commercial real estate - residential ADC Other lending subsidiaries Retail: Direct retail lending Revolving credit Residential mortgage Sales finance Other lending subsidiaries $ 39... -

Page 117

... for the years ended December 31, 2011 and 2010 are reflected in the table below. To date, there have been no goodwill impairments recorded by BB&T. Community Banking Residential Mortgage Banking Dealer Financial Services Specialized Lending Insurance Services Financial Services Total (Dollars in... -

Page 118

...date have been immaterial. BB&T also issues standard representations and warranties related to mortgage loan sales to government-sponsored entities. Although these agreements often do not specify limitations, BB&T does not believe that any payments related to these warranties would materially change... -

Page 119

...the effect of the change. Commercial Mortgage Banking Activities BB&T also arranges and services commercial real estate mortgages through Grandbridge Real Estate Capital, LLC ("Grandbridge") the commercial mortgage banking subsidiary of Branch Bank. During the years ended December 31, 2011, 2010 and... -

Page 120

...% 0.34 A summary of BB&T's deposits is presented in the accompanying table: December 31, 2011 2010 (Dollars in millions) Noninterest-bearing deposits Interest checking Money market and savings Certificates and other time deposits Foreign office deposits - interest-bearing Total deposits $ 25,684... -

Page 121

... provisions. BB&T determined that it was appropriate to amortize the remaining debt issuance costs and related discounts or premiums, including fair value hedge adjustments, over the period from March 2011 to the current expected redemption date for each of the impacted debt securities. 121 -

Page 122

... junior subordinated debt as originated by BB&T and its subsidiaries and predecessor companies as of the dates presented: December 31, Issuer Issuance Date 2011 2010 (Dollars in millions) Stated Maturity Final Maturity Interest Rate Redemption Period BB&T Capital Trust I BB&T Capital Trust II... -

Page 123

... share units based on the price of BB&T's common stock on the grant date less the present value of expected dividends that are foregone during the vesting period. BB&T recorded $98 million, $79 million and $62 million in equity-based compensation in 2011, 2010 and 2009, respectively. In connection... -

Page 124

...by loss sharing agreements with the FDIC. Refer to the Securities footnote to these financial statements for additional information. As of December 31, 2011 and 2010, unrealized net losses on securities available for sale included $57 million and $115 million, respectively, of pre-tax losses related... -

Page 125

... net holding gains (losses) arising during the period on securities available for sale Reclassification adjustment for (gains) losses on securities available for sale included in net income Net change in amounts attributable to the FDIC under the loss share agreements Net change in unrecognized... -

Page 126

... follows: Years Ended December 31, 2011 2010 2009 (Dollars in millions) Federal income taxes at statutory rate of 35% Increase (decrease) in provision for income taxes as a result of: Addition to Federal tax reserves, net State income taxes, net of Federal tax benefit Federal tax credits Interest... -

Page 127

... 31, 2011 2010 (Dollars in millions) Deferred tax assets: Allowance for loan and lease losses Net unrealized loss on securities available for sale Postretirement plans Equity-based compensation Loan/Securities basis difference Foreclosed property write-downs Net unrealized loss on cash flow hedges... -

Page 128

...of the mergers, and, under these circumstances, credit is usually given to these employees for years of service at the acquired institution for vesting and eligibility purposes. Defined Benefit Retirement Plans BB&T provides a defined benefit retirement plan qualified under the Internal Revenue Code... -

Page 129

...Plan Years Ended December 31, 2011 2010 Nonqualified Pension Plans Years Ended December 31, 2011 2010 (Dollars in millions) Change in Plan Assets: Fair value of plan assets, January 1, Actual return on plan assets Employer contributions Benefits paid Fair value of plan assets, December 31, Funded... -

Page 130

...and size in order to reduce risk and to produce incremental return. Within approved guidelines and restrictions, investment managers have wide discretion over the timing and selection of individual investments. BB&T periodically reviews its asset allocation and investment policy and makes changes to... -

Page 131

... securities is 3.6 million shares of BB&T common stock valued at $92 million at December 31, 2011. (2) This category included a common/commingled fund that is comprised of assets from several accounts, pooled together, to reduce management and administration costs. (3) The total fair value of plan... -

Page 132

... BB&T also has commitments to fund certain affordable housing investments and contingent liabilities related to certain sold loans. Commitments to extend, originate or purchase credit are primarily lines of credit to businesses and consumers and have specified rates and maturity dates. Many of these... -

Page 133

... projections, any payments made in relation to these agreements are not expected to be material to BB&T's results of operations, financial position or cash flows. In connection with the Colonial acquisition, Branch Bank entered into loss sharing agreements with the FDIC related to certain assets... -

Page 134

...to $237 million. Branch Bank is subject to laws and regulations that limit the amount of dividends it can pay. In addition, both BB&T and Branch Bank are subject to various regulatory restrictions relating to the payment of dividends, including requirements to maintain capital at or above regulatory... -

Page 135

... benefit of clients, primarily at BB&T's broker/dealer subsidiaries. NOTE 17. Parent Company Financial Statements Parent Company Condensed Balance Sheets December 31, 2011 and 2010 2011 2010 (Dollars in millions) Assets: Cash and due from banks Securities available for sale at fair value Securities... -

Page 136

Parent Company Condensed Income Statements Years Ended December 31, 2011, 2010 and 2009 2011 2010 (Dollars in millions) 2009 Income: Dividends from banking subsidiaries Dividends from other subsidiaries Interest and other income from subsidiaries Other income Total income Expenses: Interest expense... -

Page 137

... Net cash from investing activities Cash Flows From Financing Activities: Net increase in long-term debt Net decrease in short-term borrowed funds Net increase in advances from subsidiaries Net proceeds from common stock issued Retirement of preferred stock and warrant Cash dividends paid on common... -

Page 138

...Basis 12/31/2011 Level 1 Level 2 (Dollars in millions) Level 3 Assets: Trading securities Securities available for sale: GSE securities Mortgage-backed securities issued by GSE States and political subdivisions Non-agency mortgage-backed securities Other securities Covered securities Loans held for... -

Page 139

...Basis 12/31/2010 Level 1 Level 2 (Dollars in millions) Level 3 Assets: Trading securities Securities available for sale: GSE securities Mortgage-backed securities issued by GSE States and political subdivisions Non-agency mortgage-backed securities Other securities Covered securities Loans held for... -

Page 140

... loan held for sale. Residential mortgage servicing rights: BB&T estimates the fair value of residential mortgage servicing rights ("MSRs") using an option adjusted spread ("OAS") valuation model to project MSR cash flows over multiple interest rate scenarios, which are then discounted at risk... -

Page 141

.... Fair Value Measurements Using Significant Unobservable Inputs States & Political Other Trading Subdivisions Securities Residential Venture Mortgage Capital and Servicing Net Similar Rights Derivatives Investments Year Ended December 31, 2011 Covered Securities (Dollars in millions) Balance... -

Page 142

... and transfers out of Levels 1, 2 and 3 as of the end of a reporting period. During the year ended December 31, 2011, BB&T transferred certain state and political subdivision securities out of Level 3 as a result of management's decision to reclassify them from available for sale to held to maturity... -

Page 143

...of orderly transactions in the current market. For commercial loans and leases, internal credit risk models are used to adjust discount rates for risk migration and expected losses. For residential mortgage and other consumer loans, internal prepayment risk models are used to adjust contractual cash... -

Page 144

... default rates for loan products with similar risks. The fair values of commitments to fund affordable housing investments are estimated using the net present value of future commitments. The following is a summary of the carrying amounts and fair values of those financial assets and liabilities... -

Page 145

...option trades Pay fixed swaps Pay fixed swaps Total Not Designated as Hedges: Client-related and other risk management: Interest rate contracts: Receive fixed swaps Pay fixed swaps Other swaps Option trades Futures contracts Risk participations Foreign exchange contracts Total 3 month LIBOR funding... -

Page 146

..., index or referenced interest rate. There are five areas of risk management: balance sheet management, mortgage banking operations, mortgage servicing rights, net investment in a foreign subsidiary and client-related and other risk management activities. No portion of the change in fair value of... -

Page 147

... subsequent to the interest rate lock and funding date. BB&T's risk management strategy related to its interest rate lock commitment derivatives and loans held for sale includes using mortgage-based derivatives such as forward commitments and options in order to mitigate market risk. For MSRs, BB... -

Page 148

... market makers with strong credit ratings. Further, BB&T has netting agreements with the dealers with which it does business. Because of these factors, BB&T's credit risk exposure related to derivative dealers at December 31, 2011 and 2010 was not material. NOTE 20. Computation of Earnings Per Share... -

Page 149

... Mortgage Banking, Dealer Financial Services, Specialized Lending, Insurance Services, and Financial Services. These operating segments have been identified based on BB&T's organizational structure. The segments require unique technology and marketing strategies and offer different products... -

Page 150

... corporate expense. Income taxes are allocated to the various segments based on taxable income and statutory rates applicable to the segment. Community Banking Community Banking serves individual and business clients by offering a variety of loan and deposit products and other financial services... -

Page 151

..., asset management, employee benefits services, corporate banking and corporate trust services to individuals, corporations, institutions, foundations and government entities. Financial Services also offers clients investment alternatives, including discount brokerage services, equities, fixed-rate... -

Page 152

... substantial majority of the loan portfolio acquired in the Colonial acquisition is covered by loss sharing agreements with the FDIC, and is managed outside of the Community Banking segment. The assets and related interest income from this loan portfolio have an expected finite business life and are... -

Page 153

...Provision (benefit) for income taxes Segment net income (loss) Identifiable segment assets (period end) (1) $ $ $ 2 6 8 - 1,040 - 796 42 61 149 45 104 2,352 $ $ $ 2010 3 6 9 - 1,033 - 785 45 57 155 52 103 2,294 $ $ $ 2009 5 $ - 5 - 1,032 - 765 49 51 172 62 110 2,312 $ $ 2011 Financial Services 2010... -

Page 154

... N. Bible Daryl N. Bible Senior Executive Vice President and Chief Financial Officer (Principal Financial Officer) /s/ Cynthia B. Powell Cynthia B. Powell Executive Vice President and Corporate Controller (Principal Accounting Officer) A Majority of the Directors of the Registrant are included... -

Page 155

... /s/ John P. Howe III, M.D. John P. Howe III, M.D. Director /s/ Valeria Lynch Lee Valeria Lynch Lee Director /s/ Nido R. Qubein Nido R. Qubein Director /s/ Thomas E. Skains Thomas E. Skains Director /s/ Thomas N. Thompson Thomas N. Thompson Director /s/ Edwin H. Welch, Ph.D. Edwin H. Welch, Ph... -

Page 156

... Exhibit No. Description Location 2.1 Purchase and Assumption Agreement Whole Bank All Deposits, among the Federal Deposit Insurance Corporation, receiver of Colonial Bank, Montgomery, Alabama, the Federal Deposit Insurance Corporation and Branch Banking and Trust Company, dated as of August 14... -

Page 157

...Restated 2004 Stock Incentive Plan (5-Year Vesting). Form of Employee Nonqualified Stock Option Agreement for the BB&T Corporation Amended and Restated 2004 Stock Incentive Plan (4-Year Vesting). 10.9* Incorporated herein by reference to Exhibit 10.6 of the Quarterly Report on Form 10-Q, filed May... -

Page 158

...Description Location 10.16* Form of Restricted Stock Unit Agreement for the BB&T Corporation Amended and Restated 2004 Stock Incentive Plan (5-Year Vesting). Form of Restricted Stock Unit Agreement for the BB&T Corporation Amended and Restated 2004 Stock Incentive Plan (4-Year Vesting). Not used... -

Page 159

... Amended and Restated Employment Agreement by and among BB&T Corporation, Branch Banking and Trust Co. and C. Leon Wilson, III. Statement re computation of earnings per share. Statement re computation of ratios. Subsidiaries of the Registrant. Proxy Statement for the Annual Meeting of Shareholders... -

Page 160

.... 32 Filed herewith. 101.CAL 101.DEF 101.INS 101.LAB 101.PRE 101.SCH * †Filed herewith. Filed herewith. Filed herewith. Filed herewith. Filed herewith. Filed herewith. Management compensatory plan or arrangement. Exhibit filed with the Securities and Exchange Commission and available upon... -

Page 161

... financial information; and Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant's internal control over financial reporting. b) Date: February 27, 2012 /s/ Kelly S. King Kelly S. King Chairman and Chief Executive Officer -

Page 162

...; and Any fraud, whether or not material, that involves management or other employees who have a significant role in the registrant's internal control over financial reporting. b) Date: February 27, 2012 /s/ Daryl N. Bible Daryl N. Bible Senior Executive Vice President and Chief Financial Officer -

Page 163

... Executive Officer and Chief Financial Officer of BB&T Corporation (the "Company"), do hereby certify that (1) The Annual Report on Form 10-K for the fiscal year ended December 31, 2011 (the "Form 10-K") of the Company fully complies with the requirements of Section 13(a) or 15(d) of the Securities...