BB&T 2011 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2011 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

-

158

-

159

-

160

-

161

-

162

-

163

|

|

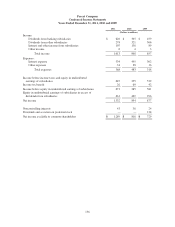

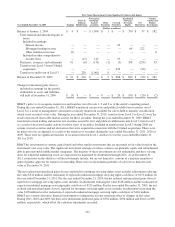

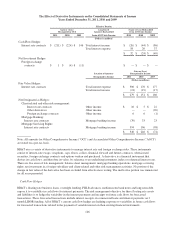

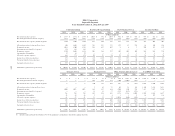

The Effect of Derivative Instruments on the Consolidated Statements of Income

Years Ended December 31, 2011, 2010 and 2009

Effective Portion

Gain or (Loss)

Recognized in OCI

Location of

Amounts Reclassified

(Gain) or Loss Reclassified

from AOCI into Income

2011 2010 2009 from AOCI into Income 2011 2010 2009

(Dollars in millions)

Cash Flow Hedges:

Interest rate contracts $ (211) $ (224) $ 146 Total interest income $ (26) $ (44) $ (86)

Total interest expense 58 20 37

$ 32 $ (24) $ (49)

Net Investment Hedges:

Foreign exchange

contracts $ 1 $ (4) $ (11) $ — $ — $ —

Gain or (Loss)

Location of Amounts Recognized in Income

Recognized in Income 2011 2010 2009

(Dollars in millions)

Fair Value Hedges:

Interest rate contracts Total interest expense $ 300 $ 170 $ 177

Total interest income (21) (19) (17)

$ 279 $ 151 $ 160

Not Designated as Hedges:

Client-related and other risk management:

Interest rate contracts Other income $ 10 $ 5 $ 22

Other derivatives Other income — — (20)

Foreign exchange contracts Other income 6 6 (1)

Mortgage Banking:

Interest rate contracts Mortgage banking income (70) 33 23

Mortgage Servicing Rights:

Interest rate contracts Mortgage banking income 394 196 (98)

$ 340 $ 240 $ (74)

Note: All amounts for Other Comprehensive Income (“OCI”) and Accumulated Other Comprehensive Income (“AOCI”)

are stated on a pre-tax basis.

BB&T uses a variety of derivative instruments to manage interest rate and foreign exchange risks. These instruments

consist of interest-rate swaps, swaptions, caps, floors, collars, financial forward and futures contracts, when-issued

securities, foreign exchange contracts and options written and purchased. A derivative is a financial instrument that

derives its cash flows, and therefore its value, by reference to an underlying instrument, index or referenced interest rate.

There are five areas of risk management: balance sheet management, mortgage banking operations, mortgage servicing

rights, net investment in a foreign subsidiary and client-related and other risk management activities. No portion of the

change in fair value of the derivative has been excluded from effectiveness testing. The ineffective portion was immaterial

for all years presented.

Cash Flow Hedges

BB&T’s floating rate business loans, overnight funding, FHLB advances, medium-term bank notes and long-term debt

expose it to variability in cash flows for interest payments. The risk management objective for these floating rate assets

and liabilities is to hedge the variability in the interest payments and receipts on future cash flows for forecasted

transactions. These forecasted transactions include interest receipts on commercial loans and interest payments on 3

month LIBOR funding. All of BB&T’s current cash flow hedges are hedging exposure to variability in future cash flows

for forecasted transactions related to the payment of variable interest on then existing financial instruments.

146