BB&T 2011 Annual Report Download - page 133

Download and view the complete annual report

Please find page 133 of the 2011 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

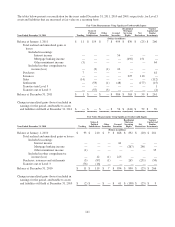

|

|

extending loans to clients and as such, the instruments are collateralized when necessary. As of December 31, 2011 and

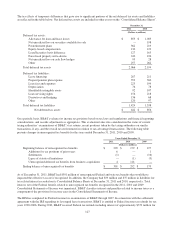

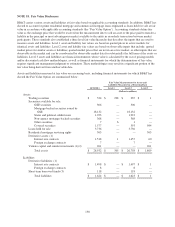

2010, BB&T had issued letters of credit totaling $6.1 billion and $7.3 billion, respectively. The carrying amount of the

liability for such guarantees was $27 million and $41 million at December 31, 2011 and 2010, respectively.

A derivative is a financial instrument that derives its cash flows, and therefore its value, by reference to an underlying

instrument, index or interest rate. For additional disclosures related to BB&T’s derivatives refer to Note 19.

In the ordinary course of business, BB&T indemnifies its officers and directors to the fullest extent permitted by law

against liabilities arising from pending litigation. BB&T also issues standard representation and warranties in

underwriting agreements, merger and acquisition agreements, loan sales, brokerage activities and other similar

arrangements. Counterparties in many of these indemnification arrangements provide similar indemnifications to BB&T.

Although these agreements often do not specify limitations, BB&T does not believe that any payments related to these

guarantees would materially change the financial position or results of operations of BB&T.

Merger and acquisition agreements of businesses other than financial institutions occasionally include additional

incentives to the acquired entities to offset the loss of future cash flows previously received through ownership positions.

Typically, these incentives are based on the acquired entity’s contribution to BB&T’s earnings compared to agreed-upon

amounts. When offered, these incentives are typically issued for terms of three to five years. As certain provisions of these

agreements do not specify dollar limitations, it is not possible to quantify the maximum exposure resulting from these

agreements. However, based on recent payouts and current projections, any payments made in relation to these

agreements are not expected to be material to BB&T’s results of operations, financial position or cash flows.

In connection with the Colonial acquisition, Branch Bank entered into loss sharing agreements with the FDIC related to

certain assets acquired. Pursuant to the terms of these loss sharing agreements, the FDIC’s obligation to reimburse Branch

Bank for losses with respect to certain loans, other real estate owned (“OREO”), certain investment securities and other

assets (collectively, “covered assets”), begins with the first dollar of loss incurred. The terms of the loss sharing agreement

with respect to certain non-agency mortgage-backed securities provides that Branch Bank will be reimbursed by the FDIC

for 95% of any and all losses. All other covered assets are subject to a stated threshold of $5 billion that provides for the

FDIC to reimburse Branch Bank for (1) 80% of losses incurred up to $5 billion and (2) 95% of losses in excess of $5

billion. Gains and recoveries on covered assets will offset losses, or be paid to the FDIC, at the applicable loss share

percentage at the time of recovery. The loss sharing agreement applicable to single family residential mortgage loans

expires in 2019, and provides for FDIC loss sharing and Branch Bank reimbursement to the FDIC. The loss sharing

agreement applicable to commercial loans and other covered assets expires in 2014, however, Branch Bank must

reimburse the FDIC for gains and recoveries through August 2017.

BB&T invests in certain affordable housing and historic building rehabilitation projects throughout its market area as a

means of supporting local communities, and receives tax credits related to these investments. BB&T typically acts as a

limited partner in these investments and does not exert control over the operating or financial policies of the partnerships.

Branch Bank typically provides financing during the construction and development of the properties; however, permanent

financing is generally obtained from independent third parties upon completion of a project. As of December 31, 2011 and

2010, BB&T had investments of $1.2 billion related to these projects, which are included as other assets on the

Consolidated Balance Sheets. BB&T’s outstanding commitments to fund affordable housing investments totaled $394

million and $334 million at December 31, 2011 and 2010, respectively, which are included as other liabilities on the

Consolidated Balance Sheets. As of December 31, 2011 and 2010, BB&T had outstanding loan commitments to these

funds of $178 million and $135 million, respectively. Of these amounts, $76 million and $36 million had been funded at

December 31, 2011 and 2010, respectively, and were included in loans and leases on the Consolidated Balance Sheets.

BB&T’s maximum risk exposure related to these investments totaled $1.4 billion and $1.3 billion at December 31, 2011

and 2010, respectively.

BB&T has sold certain mortgage-related loans that contain recourse provisions. These provisions generally require BB&T

to reimburse the investor for a share of any loss that is incurred after the disposal of the property. BB&T also issues

standard representations and warranties related to mortgage loan sales to government-sponsored entities. Refer to Note 7

for additional disclosures related to these exposures.

BB&T has investments and future funding commitments to certain venture capital funds. As of December 31, 2011 and 2010,

BB&T had investments of $261 million and $266 million related to these ventures, respectively. As of December 31, 2011 and

2010, BB&T had future funding commitments of $129 million and $185 million, respectively. BB&T’s risk exposure relating to

such commitments is generally limited to the amount of investments and future funding commitments made.

133