BB&T 2011 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2011 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

|

|

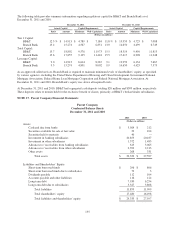

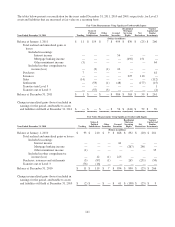

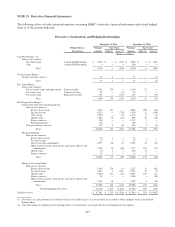

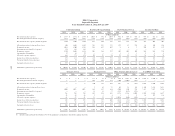

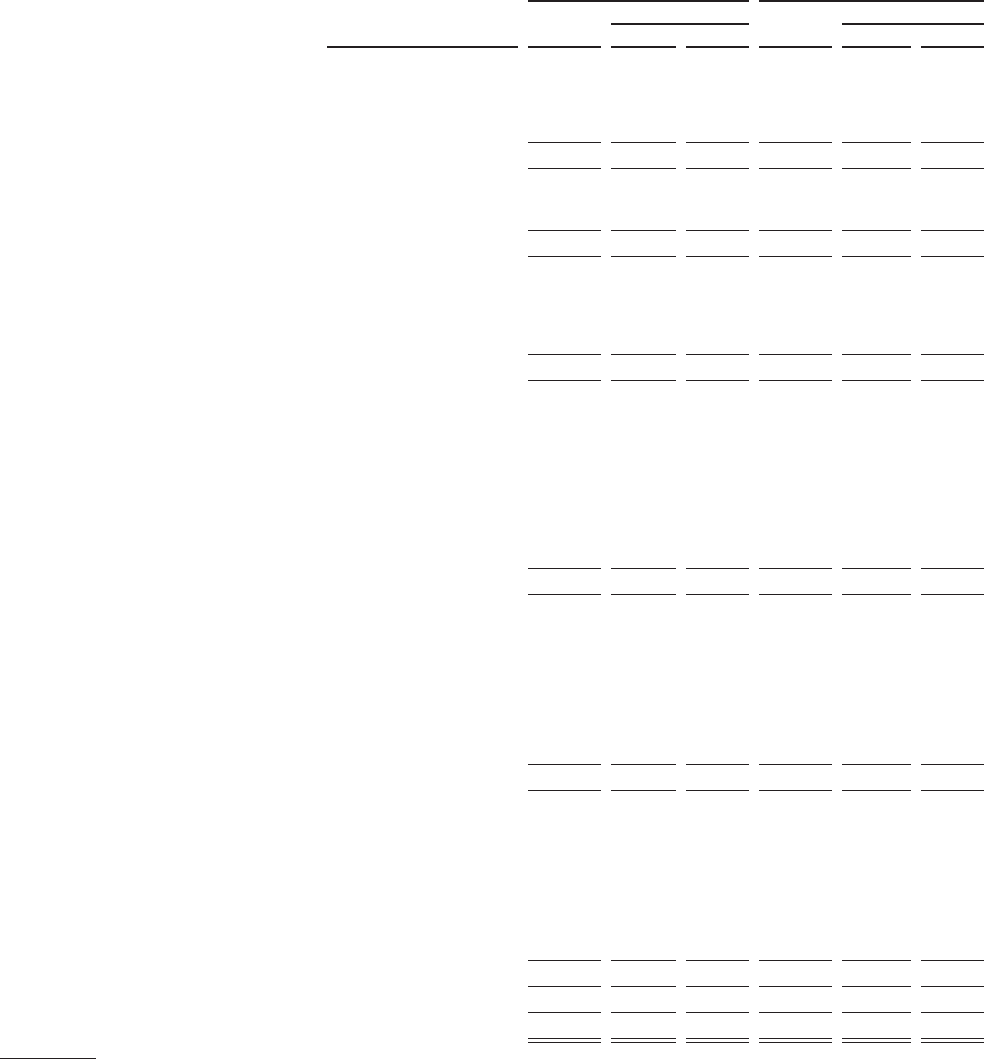

NOTE 19. Derivative Financial Instruments

The following tables set forth certain information concerning BB&T’s derivative financial instruments and related hedged

items as of the periods indicated:

Derivative Classifications and Hedging Relationships

December 31, 2011 December 31, 2010

Hedged Item or Notional Fair Value Notional Fair Value

Transaction Amount Gain (1) Loss (1) Amount Gain (1) Loss (1)

(Dollars in millions)

Cash Flow Hedges: (2)

Interest rate contracts:

Pay fixed swaps 3 month LIBOR funding $ 5,750 $ — $ (307) $ 5,950 $ 6 $ (181)

Caps 3 month LIBOR funding — — — 200 — —

Total 5,750 — (307) 6,150 6 (181)

Net Investment Hedges:

Foreign exchange contracts 73 1 — 73 — (2)

Total 73 1 — 73 — (2)

Fair Value Hedges:

Interest rate contracts:

Receive fixed swaps and option trades Long-term debt 2,556 254 — 1,160 25 —

Pay fixed swaps Commercial loans 98 — (5) 54 — —

Pay fixed swaps Municipal securities 355 — (158) 355 — (75)

Total 3,009 254 (163) 1,569 25 (75)

Not Designated as Hedges:

Client-related and other risk management:

Interest rate contracts:

Receive fixed swaps 9,176 703 — 9,696 496 (10)

Pay fixed swaps 9,255 — (730) 9,514 12 (530)

Other swaps 2,450 — (6) 3,328 2 (3)

Option trades 1,004 38 (40) 897 29 (30)

Futures contracts 240 — — 1,747 1 —

Risk participations 150 — — 180 — —

Foreign exchange contracts 575 6 (8) 436 7 (4)

Total 22,850 747 (784) 25,798 547 (577)

Mortgage Banking:

Interest rate contracts:

Receive fixed swaps 50 1 — 11 — —

Pay fixed swaps 16 — — 35 — —

Interest rate lock commitments 4,977 60 (1) 3,922 12 (37)

When issued securities, forward rate agreements and forward

commitments 7,125 10 (88) 7,717 106 (27)

Option trades 70 5 — 400 11 —

Futures contracts 65 1 — 13 1 —

Total 12,303 77 (89) 12,098 130 (64)

Mortgage Servicing Rights:

Interest rate contracts:

Receive fixed swaps 5,616 154 (1) 3,225 13 (61)

Pay fixed swaps 4,651 1 (111) 2,536 15 (7)

Option trades 9,640 273 (51) 6,095 192 (11)

Futures contracts 38 — — 4,260 — (10)

When issued securities, forward rate agreements and forward

commitments 3,651 18 — 3,582 5 (14)

Total 23,596 446 (163) 19,698 225 (103)

Total nonhedging derivatives 58,749 1,270 (1,036) 57,594 902 (744)

Total Derivatives $ 67,581 $ 1,525 $ (1,506) $ 65,386 $ 933 $ (1,002)

(1) Derivatives in a gain position are recorded as Other assets and derivatives in a loss position are recorded as Other liabilities on the Consolidated

Balance Sheet.

(2) Cash flow hedges are hedging the first unhedged forecasted settlements associated with the listed hedged item descriptions.

145