BB&T 2011 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2011 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

|

|

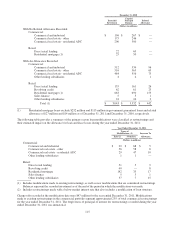

(1) Balances exclude loans serviced for others, with no other continuing involvement.

(2) Includes amounts related to residential mortgage loans held for sale and excludes amounts related to government

guaranteed loans. Refer to Loans and Leases Note for additional disclosures related to past due government

guaranteed loans.

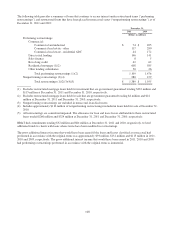

The unpaid principal balances of BB&T’s total residential mortgage servicing portfolio were $91.6 billion, $83.5 billion

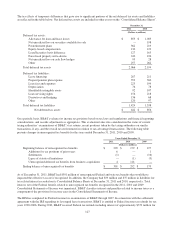

and $73.7 billion at December 31, 2011, 2010 and 2009, respectively. The unpaid principal balances of residential

mortgage loans serviced for others consist primarily of agency conforming fixed-rate mortgage loans and totaled

$67.1 billion, $61.8 billion and $54.6 billion at December 31, 2011, 2010 and 2009, respectively. Mortgage loans serviced

for others are not included in loans and leases on the accompanying Consolidated Balance Sheets.

During 2011, 2010 and 2009, BB&T sold residential mortgage loans from the held for sale portfolio with unpaid principal

balances of $17.2 billion, $19.1 billion and $25.8 billion, respectively, and recognized pre-tax gains of $175 million,

$235 million and $357 million, respectively, including the impact of interest rate lock commitments. These gains are

recorded in noninterest income as a component of mortgage banking income. BB&T retained the related mortgage

servicing rights and receives servicing fees.

At December 31, 2011, 2010 and 2009, the approximate weighted average servicing fee was 0.34%, 0.35% and 0.37%,

respectively, of the outstanding balance of the residential mortgage loans serviced for others. The weighted average

coupon interest rate on the portfolio of mortgage loans serviced for others was 5.02%, 5.26% and 5.57% at December 31,

2011, 2010 and 2009, respectively. BB&T recognized servicing fees of $240 million, $226 million and $190 million

during 2011, 2010 and 2009, respectively, as a component of mortgage banking income.

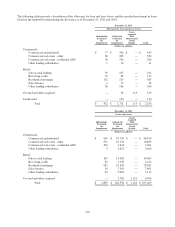

At December 31, 2011 and 2010, BB&T had $1.3 billion and $1.6 billion, respectively, of residential mortgage loans sold with

recourse liability. In the event of nonperformance by the borrower, BB&T has maximum recourse exposure of approximately

$522 million and $597 million as of December 31, 2011 and 2010, respectively. At both December 31, 2011 and 2010, BB&T

has recorded $6 million of reserves related to these recourse exposures. Payments made to date have been immaterial.

BB&T also issues standard representations and warranties related to mortgage loan sales to government-sponsored

entities. Although these agreements often do not specify limitations, BB&T does not believe that any payments related to

these warranties would materially change the financial condition or results of operations of BB&T. BB&T has recorded

$29 million and $15 million of reserves related to potential losses resulting from repurchases of loans sold at

December 31, 2011 and 2010, respectively.

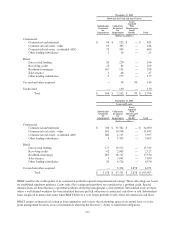

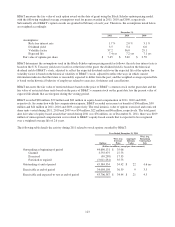

Residential mortgage servicing rights are recorded at fair value with changes in fair value recorded as a component of mortgage

banking income. BB&T uses various derivative instruments to mitigate the income statement effect of changes in fair value due

to changes in valuation inputs and assumptions of its residential mortgage servicing rights. The following is an analysis of the

activity in BB&T’s residential mortgage servicing rights for the years ended December 31, 2011, 2010 and 2009:

Residential Mortgage Servicing Rights

Years Ended December 31,

2011 2010 2009

(Dollars in millions)

Carrying value, January 1, $ 830 $ 832 $ 370

Additions 225 265 398

Increase (decrease) in fair value:

Due to changes in valuation inputs or assumptions (341) (138) 190

Other changes (1) (151) (129) (126)

Carrying value, December 31, $ 563 $ 830 $ 832

(1) Represents the realization of expected net servicing cash flows, expected borrower payments and the passage of time.

During 2011, management revised its servicing costs assumptions in the valuation of residential mortgage servicing rights

due to the expectation of higher costs that are impacting the industry. The impact of these changes resulted in a

$30 million reduction in the value of residential mortgage servicing rights. Management also updated prepayment speed

forecast assumptions primarily due to a decrease in interest rates which caused the fair value of residential mortgage

servicing rights to decrease $293 million.

118