BB&T 2011 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2011 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

|

|

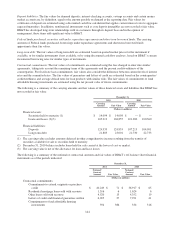

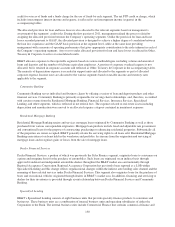

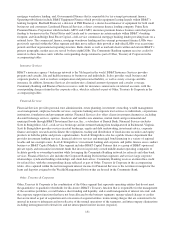

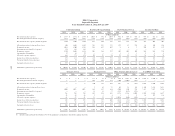

credit for sources of funds and a funds charge for the use of funds by each segment. The net FTP credit or charge, which

includes intercompany interest income and expense, is reflected as net intersegment income (expense) in the

accompanying tables.

The allocated provision for loan and lease losses is also allocated to the relevant segments based on management’s

assessment of the segments’ credit risks. During the first quarter of 2011, management refined the process related to

assigning the allocated provision between the Company’s operating segments. Unlike the provision for loan and lease

losses recorded pursuant to GAAP, the allocated provision is designed to achieve a higher degree of correlation between

the loan loss experience and the GAAP basis provision at the segment level, while at the same time providing

management with a measure of operating performance that gives appropriate consideration to the risks inherent in each of

the Company’s operating segments. Any over or under allocated provision for loan and lease losses is reflected in Other,

Treasury & Corporate to arrive at consolidated results.

BB&T allocates expenses to the reportable segments based on various methodologies, including volume and amount of

loans and deposits and the number of full-time equivalent employees. A portion of corporate overhead expense is not

allocated, but is retained in corporate accounts and reflected as Other, Treasury & Corporate in the accompanying tables.

The majority of depreciation expense is recorded in support units and allocated to the segments as part of allocated

corporate expense. Income taxes are allocated to the various segments based on taxable income and statutory rates

applicable to the segment.

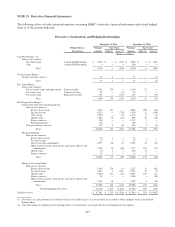

Community Banking

Community Banking serves individual and business clients by offering a variety of loan and deposit products and other

financial services. Community Banking is primarily responsible for serving client relationships, and, therefore, is credited

with certain revenue from the Residential Mortgage Banking, Financial Services, Insurance Services, Specialized

Lending, and other segments, which is reflected in net referral fees. The expenses related to real estate assets including

depreciation and amortization were moved to an allocated expense category contained in noninterest expenses.

Residential Mortgage Banking

Residential Mortgage Banking retains and services mortgage loans originated by Community Banking as well as those

purchased from various correspondent originators. Mortgage loan products include fixed and adjustable rate government

and conventional loans for the purpose of constructing, purchasing or refinancing residential properties. Substantially all

of the properties are owner occupied. BB&T generally retains the servicing rights to all loans sold. Residential Mortgage

Banking earns interest on loans held in the warehouse and portfolio, fee income from the origination and servicing of

mortgage loans and recognizes gains or losses from the sale of mortgage loans.

Dealer Financial Services

Dealer Financial Services, a portion of which was previously the Sales Finance segment, originates loans to consumers on

a prime and nonprime basis for the purchase of automobiles. Such loans are originated on an indirect basis through

approved franchised and independent automobile dealers throughout the BB&T market area and nationally through

Regional Acceptance Corporation. Regional Acceptance Corporation has previously been reported as a LOB within

Specialized Lending and this change reflects organizational changes within the indirect auto lending sales channel and the

renaming of these related services under Dealer Financial Services. This segment also originates loans for the purchase of

boats and recreational vehicles originated through dealers in BB&T’s market area. In addition, financing and servicing to

dealers for their inventories is provided through a joint relationship between Dealer Financial Services and Community

Banking.

Specialized Lending

BB&T’s Specialized Lending consists of eight business units that provide specialty finance products to consumers and

businesses. These business units are a combination of internal business units and operating subsidiaries of either the

Corporation or the Bank. The internal business units include Commercial Finance that contains commercial finance and

150