BB&T 2011 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2011 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

|

|

Services had strong noninterest income growth in 2011, with assets growing as the result of improved market conditions

and business initiatives. Noninterest income declined by $37 million, or 5.3%, between 2009 and 2010. The revenue

decrease in 2010 was attributable to losses taken on client derivatives, offsetting normalized growth in the various

businesses and the $27 million pre-tax gain on the sale of BB&T’s payroll processing business in the fourth quarter of

2009. Noninterest expense of $583 million incurred by Financial Services increased $49 million, or 9.2%, in 2011, after

declining $9 million in the prior year. The increase in noninterest expense in 2011 was the result of continued efforts to

expand the sales force in the Wealth Division and Corporate Banking.

Total identifiable assets for Financial Services of $7.5 billion increased $1.5 billion, or 24.7%, between 2010 and 2011

due primarily to organic loan growth in Corporate Banking. Comparing 2010 to 2009, total identifiable assets increased

$900 million, or 17.5%.

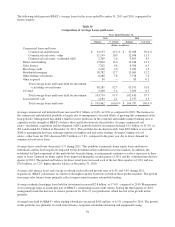

Analysis of Financial Condition

A review of the Company’s major balance sheet categories is presented below.

Investment Activities

BB&T’s investment activities are governed internally by a written, board-approved policy. The investment policy is

carried out by the Corporation’s Market Risk and Liquidity Committee (“MRLC”), which meets regularly to review the

economic environment and establish investment strategies. The MRLC also has much broader responsibilities, which are

discussed in the “Market Risk Management” section in “Management’s Discussion and Analysis of Financial Condition

and Results of Operations” herein.

Investment strategies are reviewed by the MRLC based on the interest rate environment, balance sheet mix, actual and

anticipated loan demand, funding opportunities and the overall interest rate sensitivity of the Corporation. In general, the

investment portfolio is managed in a manner appropriate to the attainment of the following goals: (i) to provide a

sufficient margin of liquid assets to meet unanticipated deposit and loan fluctuations and overall funds management

objectives; (ii) to provide eligible securities to secure public funds, trust deposits as prescribed by law and other

borrowings; and (iii) to earn the maximum return on funds invested that is commensurate with meeting the requirements

of (i) and (ii).

Branch Bank invests in securities as allowable under bank regulations. These securities may include obligations of the

U.S. Treasury, U.S. government agencies, U.S. government-sponsored entities, including mortgage-backed securities,

bank eligible obligations of any state or political subdivision, privately-issued mortgage-backed securities, structured

notes, bank eligible corporate obligations, including corporate debentures, commercial paper, negotiable certificates of

deposit, bankers acceptances, mutual funds and limited types of equity securities. Branch Bank also may deal in securities

subject to the provisions of the Gramm-Leach-Bliley Act. Scott & Stringfellow, LLC, BB&T’s full-service brokerage and

investment banking subsidiary, engages in the underwriting, trading and sales of equity and debt securities subject to the

risk management policies of the Corporation.

49