BB&T 2011 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2011 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

|

|

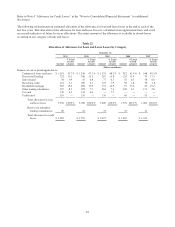

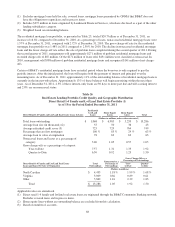

Direct Retail Loan Portfolio

The direct retail loan portfolio primarily consists of a wide variety of loan products offered through BB&T’s branch

network. Various types of secured and unsecured loans are marketed to qualifying existing clients and to other

creditworthy candidates in BB&T’s market area. The vast majority of direct retail loans are secured by first or second

liens on residential real estate, and include both closed-end home equity loans and revolving home equity lines of credit.

Direct retail loans are subject to the same rigorous lending policies and procedures as described above for commercial

loans and are underwritten with note amounts and credit limits that ensure consistency with the Corporation’s risk

philosophy.

Sales Finance Loan Portfolio

The sales finance category primarily includes secured indirect installment loans to consumers for the purchase of new and

used automobiles, boats and recreational vehicles. Such loans are originated through approved franchised and independent

dealers throughout the BB&T market area. These loans are relatively homogenous and no single loan is individually

significant in terms of its size and potential risk of loss. Sales finance loans are subject to the same rigorous lending

policies and procedures as described above for commercial loans and are underwritten with note amounts and credit limits

that ensure consistency with the Corporation’s risk philosophy. In addition to its normal underwriting due diligence,

BB&T uses application systems and “scoring systems” to help underwrite and manage the credit risk in its sales finance

portfolio. Also included in the sales finance category are commercial lines, serviced by the Sales Finance Department, to

finance dealer wholesale inventory (“Floor Plan Lines”) for resale to consumers. Floor Plan Lines are underwritten by

commercial loan officers in compliance with the same rigorous lending policies described above for commercial loans. In

addition, Floor Plan Lines are subject to intensive monitoring and oversight to ensure quality and to mitigate risk from

fraud.

Revolving Credit Loan Portfolio

The revolving credit portfolio comprises the outstanding balances on credit cards and BB&T’s checking account overdraft

protection product, Constant Credit. BB&T markets credit cards to its existing banking client base and does not solicit

cardholders through nationwide programs or other forms of mass marketing. Such balances are generally unsecured and

actively managed by BB&T FSB.

Residential Mortgage Loan Portfolio

Branch Bank offers various types of fixed- and adjustable-rate loans for the purpose of constructing, purchasing or

refinancing residential properties. BB&T primarily originates conforming mortgage loans and higher quality jumbo and

construction-to-permanent loans for owner-occupied properties. Conforming loans are loans that are underwritten in

accordance with the underwriting standards set forth by the Federal National Mortgage Association (“Fannie Mae”) and

the Federal Home Loan Mortgage Corporation (“Freddie Mac”). They are generally collateralized by one-to-four-family

residential real estate, have loan-to-collateral value ratios of 80% or less, and are made to borrowers in good credit

standing.

Risks associated with the mortgage lending function include interest rate risk, which is mitigated through the sale of a

substantial portion of conforming fixed-rate loans in the secondary mortgage market and an effective mortgage servicing

rights hedging process. Borrower risk is lessened through rigorous underwriting procedures and mortgage insurance. The

right to service the loans and receive servicing income is generally retained when conforming loans are sold. Management

believes that the retention of mortgage servicing is a primary relationship driver in retail banking and a vital part of

management’s strategy to establish profitable long-term customer relationships and offer high quality client service.

BB&T also purchases residential mortgage loans from correspondent originators. The loans purchased from third-party

originators are subject to the same underwriting and risk-management criteria as loans originated internally.

Other Lending Subsidiaries Portfolio

BB&T’s other lending subsidiaries portfolio consists of loans originated through six business units that provide specialty

finance alternatives to consumers and businesses including: dealer-based financing of equipment for small businesses and

consumers, commercial equipment leasing and finance, direct and indirect consumer finance, insurance premium finance,

74