BB&T 2011 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2011 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

|

|

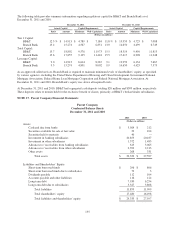

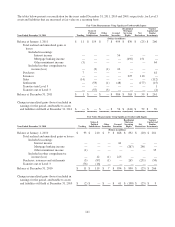

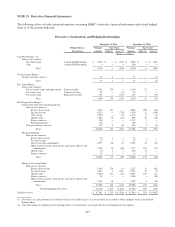

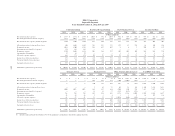

The following table details the fair value and unpaid principal balance of loans held for sale at December 31, 2011 and

2010 that were elected to be carried at fair value.

December 31,

2011 2010

Fair

Value

Aggregate

Unpaid

Principal

Balance

Fair Value

Less

Aggregate

Unpaid

Principal

Balance

Fair

Value

Aggregate

Unpaid

Principal

Balance

Fair Value

Less

Aggregate

Unpaid

Principal

Balance

(Dollars in millions)

Loans held for sale reported at fair value:

Total (1)(2) $ 3,736 $ 3,652 $ 84 $ 3,176 $ 3,192 $ (16)

Nonaccrual loans — — — — — —

Loans 90 days or more past due and still

accruing interest — — — 1 1 —

(1) The change in fair value is reflected in mortgage banking income.

(2) December 31, 2010 balance excludes loans held for sale carried at the lower of cost or market.

BB&T may be required, from time to time, to measure certain other financial assets at fair value on a nonrecurring basis.

Assets measured at fair value on a nonrecurring basis for the years ended December 31, 2011 and 2010 that were still held on

the balance sheet at December 31, 2011 and 2010 totaled $925 million and $2.0 billion, respectively. The December 31, 2011

amount consists of $389 million of impaired loans, excluding covered loans, and $536 million of foreclosed real estate,

excluding covered foreclosed real estate, that were classified as Level 3 assets. The December 31, 2010 amount consists of

$705 million of impaired loans, excluding covered loans, and $1.3 billion of foreclosed real estate, excluding covered

foreclosed real estate, that were classified as Level 3 assets. During the years ended December 31, 2011 and 2010, BB&T

recorded $348 million and $602 million, respectively, in negative valuation adjustments of impaired loans and $550 million

and $496 million, respectively, in negative valuation adjustments of foreclosed real estate.

Additionally, accounting standards require the disclosure of the estimated fair value of financial instruments that are not

recorded at fair value. A financial instrument is defined as cash, evidence of an ownership interest in an entity or a contract

that creates a contractual obligation or right to deliver or receive cash or another financial instrument from a second entity.

For the financial instruments that BB&T does not record at fair value, estimates of fair value are made at a point in time,

based on relevant market data and information about the financial instrument. Fair values are calculated based on the value of

one trading unit without regard to any premium or discount that may result from concentrations of ownership of a financial

instrument, possible tax ramifications, estimated transaction costs that may result from bulk sales or the relationship between

various financial instruments. No readily available market exists for a significant portion of BB&T’s financial instruments.

Fair value estimates for these instruments are based on current economic conditions, currency and interest rate risk

characteristics, loss experience and other factors. Many of these estimates involve uncertainties and matters of significant

judgment and cannot be determined with precision. Therefore, the calculated fair value estimates in many instances cannot be

substantiated by comparison to independent markets and, in many cases, may not be realizable in a current sale of the

instrument. In addition, changes in assumptions could significantly affect these fair value estimates. The following methods

and assumptions were used by BB&T in estimating the fair value of these financial instruments.

Cash and cash equivalents and segregated cash due from banks: For these short-term instruments, the carrying amounts

are a reasonable estimate of fair values.

Securities held to maturity: The fair values of securities held to maturity are based on a market approach using observable

inputs such as benchmark yields and securities, TBA prices, reported trades, issuer spreads, current bids and offers,

monthly payment information and collateral performance.

Loans receivable: The fair values for loans are estimated using discounted cash flow analyses, applying interest rates

currently being offered for loans with similar terms and credit quality, which are deemed to be indicative of orderly

transactions in the current market. For commercial loans and leases, internal credit risk models are used to adjust discount

rates for risk migration and expected losses. For residential mortgage and other consumer loans, internal prepayment risk

models are used to adjust contractual cash flows. Loans are aggregated into pools of similar terms and credit quality and

discounted using a LIBOR based rate. The carrying amounts of accrued interest approximate fair values.

143