BB&T 2011 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2011 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

|

|

tax years 1998-2006. In February 2010, BB&T received an IRS statutory notice of deficiency for tax years 2002-2007

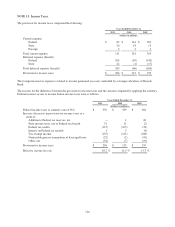

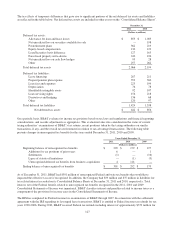

asserting a liability for taxes, penalties and interest of approximately $892 million related to the disallowance of foreign

tax credits and other deductions claimed by a subsidiary in connection with a financing transaction. Management has

consulted with outside counsel and continues to believe that BB&T’s treatment of this transaction was in compliance with

applicable tax laws and regulations. However, as a procedural matter and in order to limit its exposure to incremental

penalties and interest associated with this matter, BB&T paid the disputed tax, penalties and interest in March 2010, and

filed a lawsuit seeking a refund in the U.S. Court of Federal Claims. The Court has scheduled the trial to take place in

March 2013. BB&T recorded a receivable in other assets for the amount of this payment, less the reserve considered

necessary in accordance with applicable income tax accounting guidance. Based on an assessment of the applicable tax

law and the relevant facts and circumstances related to this matter, management has concluded that the amount of this

reserve is adequate, although litigation is still ongoing. Final resolution of this matter is not expected to occur within the

next twelve months. Various years remain subject to examination by state taxing authorities.

NOTE 14. Benefit Plans

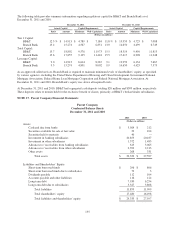

BB&T provides various benefit plans to substantially all employees, including employees of acquired entities. Employees

of acquired entities generally participate in existing BB&T plans after consummation of the business combinations. The

plans of acquired institutions are typically merged into the BB&T plans after consummation of the mergers, and, under

these circumstances, credit is usually given to these employees for years of service at the acquired institution for vesting

and eligibility purposes.

Defined Benefit Retirement Plans

BB&T provides a defined benefit retirement plan qualified under the Internal Revenue Code that covers substantially all

employees. Benefits are based on years of service, age at retirement and the employee’s compensation during the five

highest consecutive years of earnings within the last ten years of employment.

In addition, supplemental retirement benefits are provided to certain key officers under supplemental defined benefit

executive retirement plans, which are not qualified under the Internal Revenue Code. Although technically unfunded

plans, a Rabbi Trust and insurance policies on the lives of the certain covered employees are available to finance future

benefits.

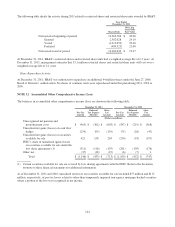

The following are the significant actuarial assumptions that were used to determine net periodic pension costs:

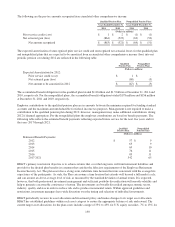

December 31,

2011 2010

Actuarial Assumptions:

Weighted average assumed discount rate 5.52 % 6.16 %

Weighted average expected long-term rate of return on plan assets 8.00 8.00

Assumed long-term rate of annual compensation increases (1) 4.50 4.50

(1) Represents the rate to be achieved by 2015.

The weighted average expected long-term rate of return on plan assets represents the average rate of return expected to be

earned on plan assets over the period the benefits included in the benefit obligation are to be paid. In developing the

expected rate of return, BB&T considers long-term compound annualized returns of historical market data for each asset

category, as well as historical actual returns on the plan assets. Using this reference information, the Company develops

forward-looking return expectations for each asset category and a weighted average expected long-term rate of return for

the plan based on target asset allocations contained in BB&T’s Investment Policy Statement.

128