BB&T 2011 Annual Report Download - page 148

Download and view the complete annual report

Please find page 148 of the 2011 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

-

160

-

161

-

162

-

163

|

|

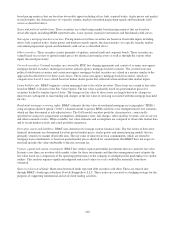

Net Investment Hedges

In connection with a long-term investment in a foreign subsidiary, BB&T is exposed to changes in the carrying value of

its investment as a result of changes in the related foreign exchange rate. At December 31, 2011 and 2010, BB&T used

derivatives to hedge the variability in the value of its $73 million investment. For net investment hedges, changes in value

of qualifying hedges are deferred in other comprehensive income (loss) when the terms of the derivative match the

notional and currency risk being hedged. At December 31, 2011 and 2010, accumulated other comprehensive income

(loss) reflected unrecognized after-tax losses totaling $11 million, related to cumulative changes in the fair value of

BB&T’s net investment hedge.

Derivatives Credit Risk

Credit risk related to derivatives arises when amounts receivable from a counterparty exceed those payable to the same

counterparty. BB&T addresses the risk of loss by subjecting counterparties to credit reviews and approvals similar to

those used in making loans or other extensions of credit and by requiring collateral. Dealer counterparties operate under

agreements to provide cash and/or liquid collateral when unsecured loss positions exceed certain negotiated limits.

As of December 31, 2011, BB&T had received cash collateral totaling $82 million related to derivatives in a gain position

totaling $80 million and had posted collateral totaling $790 million including initial margin required by exchanges related

to derivatives in a loss position totaling $730 million. As of December 31, 2010, BB&T had received cash collateral

totaling $33 million to cover derivatives in a gain position of similar value and had posted collateral totaling $605 million

related to derivatives in a loss position totaling $612 million. In the event that BB&T’s credit ratings had been

downgraded below investment grade, the amount of collateral posted would have increased by $30 million and $10

million as of December 31, 2011 and 2010, respectively.

After collateral postings are considered, BB&T had $6 million of unsecured positions in a gain with derivative dealers at

December 31, 2011 and had collateral sufficient to secure derivatives in a gain at December 31, 2010. All of the derivative

contracts to which BB&T is a party settle monthly, quarterly or semiannually. In the case of contracts with derivative

dealers, BB&T only transacts with dealers that are national market makers with strong credit ratings. Further, BB&T has

netting agreements with the dealers with which it does business. Because of these factors, BB&T’s credit risk exposure

related to derivative dealers at December 31, 2011 and 2010 was not material.

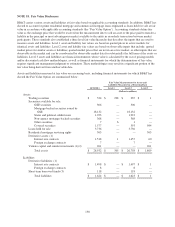

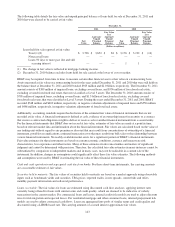

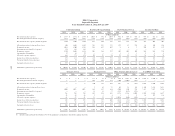

NOTE 20. Computation of Earnings Per Share

BB&T’s basic and diluted earnings per share calculations are presented in the following table:

Years Ended December 31,

2011 2010 2009

(Dollars in millions, except per share data,

shares in thousands)

Basic Earnings Per Share:

Net income available to common shareholders $ 1,289 $ 816 $ 729

Weighted average number of common shares 696,532 692,489 629,583

Basic earnings per share $ 1.85 $ 1.18 $ 1.16

Diluted Earnings Per Share:

Net income available to common shareholders $ 1,289 $ 816 $ 729

Weighted average number of common shares 696,532 692,489 629,583

Add:

Effect of dilutive outstanding equity-based awards 8,636 8,550 6,036

Weighted average number of diluted common shares 705,168 701,039 635,619

Diluted earnings per share $ 1.83 $ 1.16 $ 1.15

148