Philips 2013 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2013 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

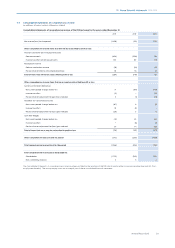

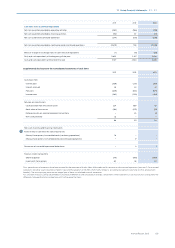

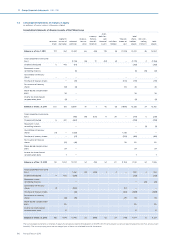

11 Group financial statements 11.9 - 11.9

138 Annual Report 2013

Acquisitions of and adjustments to non-controlling interests

Acquisitions of non-controlling interests are accounted for as transactions

with owners in their capacity as owners and therefore no goodwill is

recognized. Adjustments to non-controlling interests arising from

transactions that do not involve the loss of control are based on a

proportionate amount of the net assets of the subsidiary.

For changes to non-controlling interest without the loss of control, the

dierence between such change and any consideration paid or received is

recognized directly in equity.

Loss of control

Upon the loss of control, the Company derecognizes the assets and

liabilities of the subsidiary, any non-controlling interests and the other

components of equity related to the subsidiary. Any surplus or deficit

arising on the loss of control is recognized in the Statement of income. If

the Company retains any interest in the previous subsidiary, then such

interest is measured at fair value at the date the control is lost.

Subsequently it is accounted for as an equity-accounted investee or as an

available-for-sale financial asset depending on the level of influence

retained.

Investments in associates (equity-accounted investees)

Associates are all entities over which the Company has significant

influence, but not control. Significant influence is presumed with a

shareholding of between 20% and 50% of the voting rights. Investments in

associates are accounted for using the equity method of accounting and

are initially recognized at cost. The group’s investment in associates

includes goodwill identified on acquisition, net of any accumulated

impairment loss.

The Company’s share of the net income of these companies is included in

results relating to associates in the Statement of income, after adjustments

to align the accounting policies with those of the Company, from the date

that significant influence commences until the date that significant

influence ceases. When the Company’s share of losses exceeds its interest

in an associate, the carrying amount of that interest (including any long-

term loans) is reduced to zero and recognition of further losses is

discontinued except to the extent that the Company has incurred legal or

constructive obligations or made payments on behalf of the associate.

Unrealized gains on transactions between the Company and its associates

are eliminated to the extent of the Company’s interest in the associates.

Unrealized losses are also eliminated unless the transaction provides

evidence of an impairment of the asset transferred. Remeasurement

dierences of equity stake resulting from gaining control over the investee

previously recorded as associate are recorded under Results related to

investments in associates.

Investments in associates include loans from the Company to these

investees.

Accounting for capital transactions of a consolidated subsidiary or an

associate

The Company recognizes dilution gains or losses arising from the sale or

issuance of stock by a consolidated subsidiary or an associate in the

Statement of income, unless the Company or the subsidiary either has

reacquired or plans to reacquire such shares. In such instances, the result

of the transaction is recorded directly in equity.

Dilution gains and losses arising in investments in associates are

recognized in the Consolidated statements of income under Results

relating to investments in associates.

Foreign currencies

Foreign currency transactions

The financial statements of all group entities are measured using the

currency of the primary economic environment in which the entity

operates (functional currency). The euro (EUR) is the functional and

presentation currency of the Company. Foreign currency transactions are

translated into the functional currency using the exchange rates prevailing

at the dates of the transactions or valuation where items are remeasured.

Foreign exchange gains and losses resulting from the settlement of such

transactions and from the translation at year-end exchange rates of

monetary assets and liabilities denominated in foreign currencies are

recognized in the Statement of income, except when deferred in Other

comprehensive income as qualifying cash flow hedges and qualifying net

investment hedges.

Foreign currency dierences arising from translation are recognized in

profit or loss, except for available-for-sale equity investments (except on

impairment in which case foreign currency dierences that have been

recognized in Other comprehensive income are reclassified to profit and

loss), which are recognized in Other comprehensive income.

All exchange dierence items are presented as part of Cost of sales, with

the exception of tax items and financial income and expense, which are

recognized in the same line item as they relate in the Statement of income.

Non-monetary assets and liabilities denominated in foreign currencies

that are measured at fair value are retranslated to the functional currency

using the exchange rate at the date the fair value was determined. Non-

monetary items in a foreign currency that are measured based on

historical cost are translated using the exchange rate at the date of

transaction.

Foreign operations

The assets and liabilities of foreign operations, including goodwill and fair

value adjustments arising on acquisition, are translated to euro at

exchange rates at the reporting date. The income and expenses of foreign

operations are translated to euro at exchange rates at the dates of the

transactions.

Foreign currency dierences arising on translation of foreign operations

into the Group’s presentation currency are recognized in Other

comprehensive income, and presented as part of Currency translation

dierences in equity. However, if the operation is a non-wholly owned

subsidiary, then the relevant proportionate share of the translation

dierence is allocated to the non-controlling interests.

When a foreign operation is disposed of such that control, significant

influence or joint control is lost, the cumulative amount in the translation

reserve related to the foreign operation is reclassified to the Statement of

income as part of the gain or loss on disposal. When the Company

disposes of only part of its interest in a subsidiary that includes a foreign

operation while retaining control, the relevant proportion of the

cumulative amount is reattributed to Non-controlling interests. When the

Company disposes of only part of its investment in an associate or joint

venture that includes a foreign operation while retaining significant

influence or joint control, the relevant proportion of the cumulative

amount is reclassified to the Statement of income.

Financial instruments

Non-derivative financial instruments

Non-derivative financial instruments are recognized initially at fair value

when the Company becomes a party to the contractual provisions of the

instrument.

Regular way purchases and sales of financial instruments are accounted

for at the trade date. Dividend and interest income are recognized when

earned. Gains or losses, if any, are recorded in Financial income and

expense.

Non-derivative financial instruments comprise cash and cash equivalents,

receivables, other non-current financial assets and debt and other

financial liabilities that are not designated as hedges.

Cash and cash equivalents

Cash and cash equivalents include all cash balances and short-term

highly liquid investments with an original maturity of three months or less

that are readily convertible into known amounts of cash.

Receivables

Receivables are carried at the lower of amortized cost or the present value

of estimated future cash flows, taking into account discounts given or

agreed. The present value of estimated future cash flows is determined

through the use of value adjustments for uncollectible amounts. As soon

as individual trade accounts receivable can no longer be collected in the

normal way and are expected to result in a loss, they are designated as

doubtful trade accounts receivable and valued at the expected collectible

amounts. They are written o when they are deemed to be uncollectible

because of bankruptcy or other forms of receivership of the debtors. The

allowance for the risk of non-collection of trade accounts receivable takes

into account credit-risk concentration, collective debt risk based on

average historical losses, and specific circumstances such as serious

adverse economic conditions in a specific country or region.