Philips 2013 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2013 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

11 Group financial statements 11.9 - 11.9

144 Annual Report 2013

recycled in the future. The application of this amendment impacts

presentation and disclosures only. Comparative information has been re-

presented.

IAS 19 Employee Benefits (2011)

As a result of the introduction of IAS 19 (2011) - or IAS 19R/Revised - the

Company has changed its accounting policy with regard to the accounting

of defined benefit pension plans. The main change impacts the basis of

determining the income or expense for the period related to these pension

plans. Under the new standard the Company determines a net interest

expense (income) by applying the discount rate used to measure the

defined benefit obligation (DBO) at the beginning of the annual period to

the net defined benefit liability (asset) at the beginning of the annual

period, taking into account any changes in the net defined benefit liability

(asset) during the period as a result of contributions and benefit payments.

As a result, this net interest now comprises:

• interest cost on the DBO;

• interest income on plan assets; and

• interest on the eect of the asset ceiling.

Previously, the Company determined interest income on plan assets

based on their long-term rate of expected return. Furthermore, as from

January 1, 2013 the Company presents net interest expenses related to

defined benefits in Financial income and expense rather than Income from

operations.

The new standard no longer allows for accrual of future pension

administration costs as part of the DBO. Such costs should be expensed as

incurred. Previously, for the Dutch pension plan the Company accrued a

surcharge for pension administration costs as part of the service costs into

the DBO. With the adoption of the new standard this accrual was

eliminated, resulting in an exclusion of EUR 216 million from the DBO per

January 1, 2013, thereby improving the funded status. This funded status

improvement is oset by the impact of the asset ceiling test regarding the

Dutch pension plan’s surplus, and hence there is no further impact on the

Company’s balance sheet figures other than the direct recognition of

previously unrecognized past service cost.

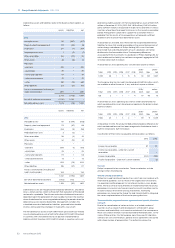

The impact on Equity from the IAS 19 (2011) accounting policy change is as

follows:

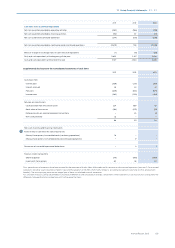

December 31,

2012

Decrease in the net defined benefit obligation

(non-current, after asset ceiling restriction) 13

Increase in deferred tax assets (non-current) (2)

Net increase on equity 11

Split to:

Equity holders of the parent 11

Non-controlling interest –

The limited impact on the balance sheet mainly relates to some

unrecognized past service cost gains and losses which must be recognized

immediately under IAS 19 (2011). The limited impact is explained by the

fact that the Company already applied immediate recognition of actuarial

gains and losses in Other comprehensive income.

The negative impact of IAS 19 (2011) for post-employment defined benefit

plans on Income from operations, Income before taxes and Basic and

Diluted earnings per share is as follows:

2011 2012

Income from operations (124) (260)

Financial income and expenses (92) (85)

Income before taxes (216) (345)

Basic earnings per share (0.17) (0.28)

Diluted earnings per share (0.17) (0.28)

Recoverable Amount Disclosures for Non-Financial Assets

(Amendments to IAS 36) (2013)

The amendment to IAS 36 Impairment of Assets was introduced following

the introduction of IFRS 13 Fair Value Measurement, to reduce the

circumstances in which the recoverable amount of assets or cash-

generating units is required to be disclosed, clarify the disclosures

required, and to introduce an explicit requirement to disclose the discount

rate used in determining impairment (or reversals) where recoverable

amount (based on fair value less costs of disposal) is determined using a

present value technique. As the amendment is basically to avoid

unintended disclosure requirements from the introduction of IFRS 13, it

was early adopted by the Company. The amendment has no material

impact.

Defined Benefit Plans: Employee Contributions (Amendments to IAS 19)

Initially the abovementioned IAS 19 (2011) adjustments required that

employee contributions basically would have to be incorporated in the

measurement of the defined benefit obligation. This amendment allows a

practical expedient to continue to recognize employee contributions in

the Statement of income when certain conditions are met. The Company

early adopted this amendment and as a result there is no change in the

way how employee contributions are currently treated compared to the

treatment prior to the IAS 19 (2011) adoption. Up to 2013 the Company has

very limited employee contributions in their pension plans.

IFRS accounting standards adopted as from 2014 and onwards

A number of new standards and amendments to existing standards have

been published and are mandatory for the Company beginning on or after

January 1, 2014 or later periods, and the Company has not yet early

adopted them. Those which may be the most relevant to the Company are

set out below.

IFRIC 21 Levies

IFRIC 21 provides guidance on the accounting for certain outflows

imposed on entities by governments in accordance with laws and/or

regulations (levies). The Interpretation identifies the obligating event for

the recognition of a liability as the activity that triggers the payment of the

levy in accordance with the relevant legislation. This Interpretation does

not have a material impact on the financial statements.

Changes to other standards, following from Amendments and the Annual

Improvement Cycles, do not have a material impact on the Company’s

financial statements.