Philips 2013 Annual Report Download - page 171

Download and view the complete annual report

Please find page 171 of the 2013 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

11 Group financial statements 11.9 - 11.9 27 28 29 30

Annual Report 2013 171

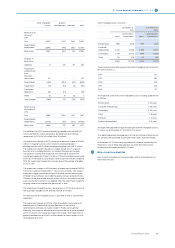

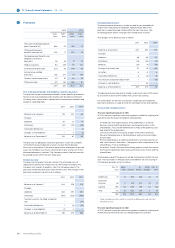

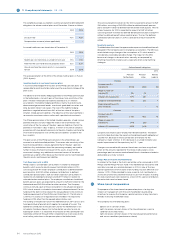

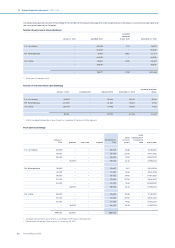

27 Cash from (used for) derivatives and current financial

assets

A total of EUR 93 million cash was paid with respect to foreign exchange

derivative contracts related to financing activities (2012: EUR 47 million

outflow; 2011: EUR 25 million inflow).

A total of EUR 8 million was paid with respect to current financial assets

(2012: EUR 1 million inflow; 2011: EUR 1 million inflow).

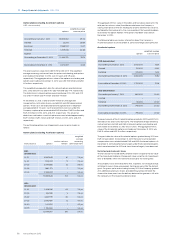

28 Purchase and proceeds from non-current financial

assets

In 2013, there were no significant cash flows resulting from investing

activities.

In 2012, the cash outflow was mainly due to loans provided to TPV

Technology Limited and TP Vision venture in connection with the

divestment of the Television business (EUR 151 million in aggregate).

In 2011, the sale of Philips’ interest in TCL Corporation (TCL) and Digimarc

generated cash totaling EUR 79 million.

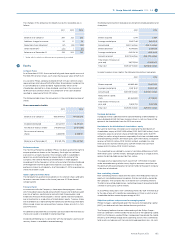

29 Assets in lieu of cash from sale of businesses

In 2013, there were no transactions related to the sale of businesses that

involved assets in lieu of cash.

In 2012, Philips received certain financial instruments in exchange for the

transfer of its television business. At the date of this transaction the fair

value of these financial instruments involved an amount of EUR 17 million.

In 2011, the Company entered into four transactions with dierent venture

capital partners where certain incubator activities were transferred in

exchange for shares in separately established investment entities. The

investment entities represented a value of EUR 18 million at the date that

these transactions were closed.

30 Post-employment benefits

Employee post-employment plans have been established in many

countries in accordance with the legal requirements, customs and the

local practice in the countries involved.

The Company sponsors a number of defined-benefit pension plans. The

benefits provided by these plans are based on employees’ years of service

and compensation levels. The Company also sponsors a limited number of

defined-benefit retiree medical plans. The benefits provided by these

plans are typically covering a part of the healthcare insurance costs after

retirement. Most employees that take part in a Company pension plan

however are covered by defined-contribution (DC) pension plans.

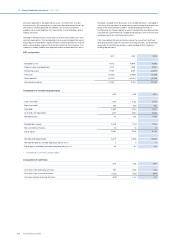

The largest defined-benefit pension plans are in;

• The Netherlands,

• The United Kingdom (UK) and

• The United States (US).

Together these plans account for more than 90% of the total defined-

benefit obligation and plan assets.

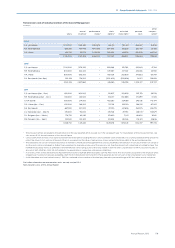

The Netherlands

The pension plan in the Netherlands is of a defined-benefit nature. The

annual accrual rate in this career average pay plan that covers all

employees covered under the Collective Labour Agreement is 1.85% of the

pension salary. Executives are in a ‘hybrid plan’ with an accrual rate of

1.25% per service year next to a DC contribution, the level of which

depends on the executive grade. Both plans are executed by the

Company Pension Fund.

Indexation of benefits is conditional and depends among others on the

statutory and regulatory funding ratio of the Fund. The Company is

required to fund the annual service cost plus surcharges for solvency

requirements, costs and a contribution for indexation. The Company is

required to pay additional surcharges in case the funded status of the

Company Pension Fund drops below an agreed level. The Company is

entitled to discounts and refunds if the funded status of the Company

Pension Fund exceeds an agreed surplus level.

Following the new Collective Labour Agreement with the respective trade

unions in 2013 a new funding agreement has been agreed with the

Trustees of the Company Pension Fund. Under the new funding

agreement, which becomes eective January 1, 2014, the Company has no

further financial obligation to the Pension Fund other than to pay an

agreed fixed contribution for the annual accrual of active members.

Although the new funding agreement will de-risk the plan, the annual

premium can be subject to variability after five years due to potential

discounts and as a result, the plan continues to be accounted for as a

defined benefit plan. The other changes in the plan are a new pensionable

age of 67 (was 65) and the introduction of an employee contribution.

These changes had practically no impact on the existing defined benefit

obligation. For further details we refer to note 36, Subsequent events.

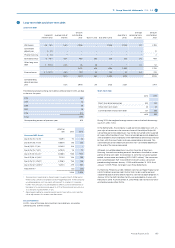

United Kingdom

The UK plan is executed by a Company Pension Fund. In the UK plan the

accrual of new benefits ceased in 2011. A legally mandatory indexation for

accrued benefits still applies. The Company does not pay regular

contributions, other than an agreed portion of the administration costs.

The UK plan assets until September 2013 contained a high concentration

of NXP shares. The NXP shares were transferred to the Fund by the

Company in 2010 as part of a recovery plan and have by now all been sold

by the UK Fund. In 2013 the Trustee of the UK Fund entered into a bulk

insurance contract - a buy-in - which provides for payment in respect of a

part of the Fund’s pensioners. The asset value related to this buy-in

included in the UK plan assets equals the defined-benefit obligation of the

related pensioners and is EUR 508 million per December 31, 2013.

United States

The US defined-benefit plan covers certain hourly workers and salaried

workers hired before January 1, 2005.

The accrual for salaried workers in the US plan will end per December 31,

2015. The announcement in 2013 of this delayed freeze in the US plan

triggered a past service cost gain of EUR 78 million. In the same US plan in

2013 a large group of terminated vested employees accepted a lump-sum

oering thus lowering the plan assets and liabilities. The related

settlement result was a loss of EUR 31 million.

Indexation of benefits is not mandatory. The Company pays contributions

for the annual service costs as well as additional contributions to cover a

deficit. The assets of the US plan are in a Trust governed by Trustees.

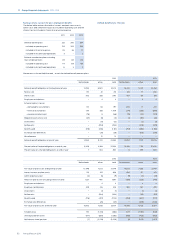

Risks related to defined-benefit plans

These defined-benefit plans expose the Company to various

demographic and economic risks such as longevity risk, investment risks,

currency and interest rate risk and in some cases inflation risk. The latter

plays a role in the assumed wage increase and in the UK plan where

indexation is mandatory. Pension fund Trustees are responsible for and

have full discretion over the investment strategy of the plan assets. In

general Trustees manage pension fund risks by diversifying the

investments of plan assets and by (partially) matching interest rate risk of

liabilities.

The Company has an active derisking strategy in which it constantly looks

for opportunities to reduce the risks associated with its defined benefit

plans. Liability driven investment strategies, lump sum cash-out options,

buy-ins, buy-outs and the above mentioned change in the funding of the

Dutch plan are examples of that strategy. The larger plans are either

governed by independent Boards or by Trustees who have a legal

obligation to evenly balance the interests of all stakeholders and operate

under the local regulatory framework.

Balance sheet positions

The net balance sheet position presented in this note can be explained as

follows:

• The surpluses in our plans in The Netherlands, UK as well some other

countries are not recognized as a net defined benefit asset because in

The Netherlands the current surplus will not bring sufficient future

economic benefits to the Company (asset ceiling restrictions) whereas

the regulatory framework in the other countries involved explicitly

prohibits refunds to the employer.

• The deficit of the US defined-benefit plan presented under other

liabilities and the provisions of the unfunded plans therefore count for

the largest part of the net balance sheet position.

The measurement date for all defined-benefit plans is December 31.