Philips 2013 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2013 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

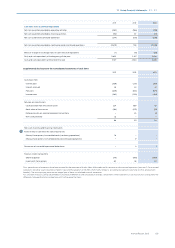

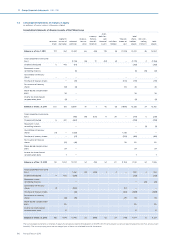

11 Group financial statements 11.9 - 11.9

Annual Report 2013 143

be refundable or deductible. Changes in tax rates are reflected in the

period when the change has been enacted or substantially-enacted by

the reporting date.

Discontinued operations and non-current assets held for sale

Non-current assets (disposal groups comprising assets and liabilities) that

are expected to be recovered primarily through sale rather than through

continuing use are classified as held for sale.

A discontinued operation is a component of an entity that either has been

disposed of, or that is classified as held for sale, and (a) represents a

separate major line of business or geographical area of operations; and (b)

is a part of a single coordinated plan to dispose of a separate major line of

business or geographical area of operations; or (c) is a subsidiary acquired

exclusively with a view to sell. A component that previously was held for

use will have one or more cash-generating units. Generally, the disposal of

a business that previously was part of a single cash-generating unit does

not qualify as a component of an entity and therefore shall not be

classified as a discontinued operation if disposed of.

Non-current assets held for sale and discontinued operations are carried

at the lower of carrying amount or fair value less costs to sell. Any gain or

loss from disposal of a business, together with the results of these

operations until the date of disposal, is reported separately as

discontinued operations. The financial information of discontinued

operations is excluded from the respective captions in the Consolidated

financial statements and related notes for all periods presented.

Comparatives in the balance sheet are not re-presented when a non-

current asset or disposal group is classified as held for sale. Comparatives

are restated for presentation of discontinued operations in the Statement

of cash flow and Statement of income.

Upon classification of a disposal group as held for sale the Company may

agree with the buyer to retain certain assets and liabilities, in which case

such items are not presented as part of assets/liabilities held for sale, even

though the associated item in the Statement of income would be

presented as part of discontinued operations. The presentation of cash

flows relating to such items in that case mirrors the classification in the

Statement of income, i.e. as cash flows from discontinued operations.

Adjustments in the current period to amounts previously presented in

discontinued operations that are directly related to the disposal of a

discontinued operation in a prior period are classified separately in

discontinued operations. Circumstances to which these adjustments may

relate include resolution of uncertainties that arise from the terms of the

disposal transaction, such as the resolution of a purchase price

adjustments and indemnifications, resolution of uncertainties that arise

from and are directly related to the operations of the component before its

disposal, such as environmental and product warranty obligations

retained by the Company, or the settlement of employee benefit plan

obligations provided that the settlement is directly related to the disposal

transaction.

Segments

Operating segments are components of the Company’s business activities

about which separate financial information is available that is evaluated

regularly by the chief operating decision maker (the Board of

Management of the Company). The Board of Management decides how to

allocate resources and assesses performance. Reportable segments

comprise the operating sectors Healthcare, Consumer Lifestyle and

Lighting. Innovation, Group & Services (IG&S) is a sector but not a separate

reportable segment and holds, amongst others, headquarters, overhead

and regional/country organization expenses. Segment accounting

policies are the same as the accounting policies as applied to the Group.

Cash flow statements

Cash flow statements are prepared using the indirect method. Cash flows

in foreign currencies have been translated into euros using the weighted

average rates of exchange for the periods involved. Cash flows from

derivative instruments that are accounted for as fair value hedges or cash

flow hedges are classified in the same category as the cash flows from the

hedged items. Cash flows from other derivative instruments are classified

consistent with the nature of the instrument.

Earnings per share

The Company presents basic and diluted earnings per share (EPS) data for

its common shares. Basic EPS is calculated by dividing the net income

attributable to shareholders of the Company by the weighted average

number of common shares outstanding during the period, adjusted for

own shares held. Diluted EPS is determined by adjusting the Statement of

income attributable to shareholders and the weighted average number of

common shares outstanding, adjusted for own shares held, for the eects

of all dilutive potential common shares, which comprise convertible

personnel debentures, restricted shares, performance shares and share

options granted to employees.

Financial guarantees

The Company recognizes a liability at the fair value of the obligation at the

inception of a financial guarantee contract. The guarantee is subsequently

measured at the higher of the best estimate of the obligation or the

amount initially recognized.

IFRS accounting standards adopted as from 2013

The accounting policies set out above have been applied consistently to

all periods presented in these Consolidated financial statements except as

explained below which addresses changes in accounting policies. In case

of the absence of explicit transition requirements for new accounting

pronouncements, the Company accounts for any change in accounting

principle retrospectively.

The Company has adopted the following new and amended IFRSs as of

January 1, 2013.

Disclosures - Osetting Financial Assets and Liabilities (Amendments to

IFRS 7)

As a result of the amendments to IFRS 7, the Company has expanded its

disclosures about the osetting of financial assets and liabilities. See

note 34, Fair value of financial assets and liabilities.

IFRS 10 Consolidated Financial Statements

IFRS 10 introduces a single control model to determine whether an

investee should be consolidated. The new standard includes guidance on

control with less than half of the voting rights (‘de facto’ control),

participating and protective voting rights and agent/principal

relationships. Based on a reassessment of the control conclusion for the

investees at January 1, 2013, the adoption of IFRS 10 did not have a

material impact on the Company’s Consolidated financial statements.

IFRS 11 Joint Arrangements

Under IFRS 11, the structure of the joint arrangement, although still an

important consideration, is no longer the main factor in determining the

type of joint arrangement and therefore the subsequent accounting.

Instead:

• The Company’s interest in a joint operation, which is an arrangement in

which the parties have rights to the assets and obligations for the

liabilities, will be accounted for on the basis of the Company’s interest

in those assets and liabilities.

• The Company’s interest in a joint venture, which is an arrangement in

which the parties have rights to the net assets, are equity-accounted.

Prior to 2012 the Company accounted for jointly controlled entities using

the equity method. The adoption therefore does not have a material

impact on the Company’s Consolidated financial statements.

IFRS 12 Disclosure of Interests in Other Entities

This standard contains the disclosure requirements for interests in

subsidiaries, joint ventures, associates and other unconsolidated

interests. As a result of IFRS 12, the Company has expanded its disclosures

on interests in other entities. See note 6, Interests in entities.

IFRS 13 Fair Value Measurement

IFRS 13 establishes a single framework for measuring fair value and making

disclosures about fair value measurements, when such measurements are

required or permitted by other IFRSs. More specifically, the definition of

fair value was clarified to be the price at which an orderly transaction to sell

an asset or to transfer a liability would take place between market

participants at the measurement date. The standard also replaces and

expands disclosure requirements about fair value measurements in other

IFRSs, of which some of these are required in interim financial statements

related to financial instruments. The Company therefore has included

additional disclosures in note 34, Fair value of financial assets and

liabilities. IFRS 13 has no material impact on the measurements of the

Company’s assets and liabilities.

Presentation of Items of Other Comprehensive Income (Amendments to

IAS 1)

The new amendment requires separation of items presented in Other

comprehensive income into two groups, based on whether or not they can

be recycled into the Statement of income in the future. Items that will not

be recycled in the future are presented separately from items that may be