Philips 2013 Annual Report Download - page 186

Download and view the complete annual report

Please find page 186 of the 2013 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

11 Group financial statements 11.9 - 11.9

186 Annual Report 2013

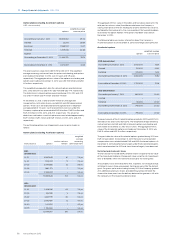

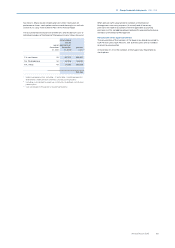

The total net fair value of hedges related to transaction exposure as of

December 31, 2013 was an unrealized asset of EUR 44 million. An

instantaneous 10% increase in the value of the euro against all currencies

would lead to a decrease of EUR 68 million in the value of the derivatives;

including a EUR 58 million decrease related to foreign exchange

transactions of the US dollar against the euro, a EUR 15 million decrease

related to foreign exchange transactions of the Japanese yen against

euro, a EUR 15 million decrease related to foreign exchange transactions

of the Pound sterling, partially oset by a EUR 46 million increase related

to foreign exchange transactions of the euro against the US dollar.

The EUR 68 million decrease includes a loss of EUR 19 million that would

impact the income statement, which would largely oset the opposite

revaluation eect on the underlying accounts receivable and payable, and

the remaining loss of EUR 49 million would be recognized in equity to the

extent that the cash flow hedges were eective.

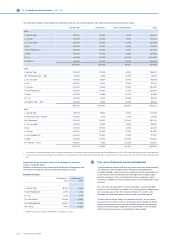

The total net fair value of hedges related to transaction exposure as of

December 31, 2012 was an unrealized asset of EUR 25 million. An

instantaneous 10% increase in the value of the euro against all currencies

would lead to a decrease of EUR 69 million in the value of the derivatives;

including a EUR 96 million decrease related to foreign exchange

transactions of the US dollar against the euro, a EUR 17 million decrease

related to foreign exchange transactions of the Japanese yen against

euro, a EUR 8 million decrease related to foreign exchange transactions of

the Pound sterling, partially oset by a EUR 69 million increase related to

foreign exchange transactions of the euro against the US dollar.

Foreign exchange exposure also arises as a result of inter-company loans

and deposits. Where the Company enters into such arrangements the

financing is generally provided in the functional currency of the subsidiary

entity. The currency of the Company’s external funding and liquid assets is

matched with the required financing of subsidiaries either directly through

external foreign currency loans and deposits, or synthetically by using

foreign exchange derivatives, including cross currency interest rate swaps

and foreign exchange forward contracts. In certain cases where group

companies may also have external foreign currency debt or liquid assets,

these exposures are also hedged through the use of foreign exchange

derivatives. Changes in the fair value of hedges related to this exposure

are either recognized within financial income and expenses in the

statements of income, accounted for as cash flow hedges or where such

loans would be considered part of the net investment in the subsidiary

then net investment hedging would be applied. Translation exposure of

foreign-currency equity invested in consolidated entities may be hedged.

If a hedge is entered into, it is accounted for as a net investment hedge. As

of December 31, 2013 cross currency interest rate swaps and foreign

exchange forward contracts with a fair value liability of EUR 261 million

and external bond funding for a nominal value of USD 4,059 million were

designated as net investment hedges of our financing investments in

foreign operations. During 2013 a total gain of EUR 2 million was

recognized in the income statement as ineectiveness on net investment

hedges. The total net fair value of these financing derivatives as of

December 31, 2013, was a liability of EUR 260 million. An instantaneous

10% increase in the value of the euro against all currencies would lead to

an increase of EUR 245 million in the value of the derivatives, including a

EUR 272 million increase related to the US dollar.

Philips does not currently hedge the foreign exchange exposure arising

from equity interests in non-functional-currency investments in

associates and available-for-sale financial assets.

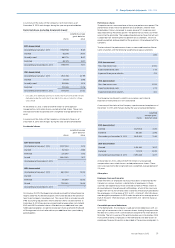

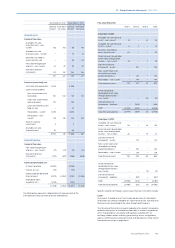

Interest rate risk

Interest rate risk is the risk that the fair value or future cash flows of a

financial instrument will fluctuate because of changes in market interest

rates. Philips had outstanding debt of EUR 3,901 million, which created an

inherent interest rate risk. Failure to eectively hedge this risk could

negatively impact financial results. At year-end, Philips held EUR 2,465

million in cash and cash equivalents, total long-term debt of EUR 3,309

million and total short-term debt of EUR 592 million. At December 31, 2013,

Philips had a ratio of fixed-rate long-term debt to total outstanding debt

of approximately 80%, compared to 72% one year earlier.

A sensitivity analysis conducted as of January 2014 shows that if long-

term interest rates were to decrease instantaneously by 1% from their level

of December 31, 2013, with all other variables (including foreign exchange

rates) held constant, the fair value of the long-term debt would increase

by approximately EUR 317 million. If there was an increase of 1% in long-

term interest rates, this would reduce the market value of the long-term

debt by approximately EUR 251 million.

If interest rates were to increase instantaneously by 1% from their level of

December 31, 2013, with all other variables held constant, the annualized

net interest expense would decrease by approximately EUR 18 million.

This impact was based on the outstanding net cash position at December

31, 2013.

A sensitivity analysis conducted as of January 2013 shows that if long-

term interest rates were to decrease instantaneously by 1% from their level

of December 31, 2012, with all other variables (including foreign exchange

rates) held constant, the fair value of the long-term debt would increase

by approximately EUR 422 million. If there was an increase of 1% in long-

term interest rates, this would reduce the market value of the long-term

debt by approximately EUR 339 million.

If interest rates were to increase instantaneously by 1% from their level of

December 31, 2012, with all other variables held constant, the annualized

net interest expense would decrease by approximately EUR 25 million.

This impact was based on the outstanding net cash position at December

31, 2012.

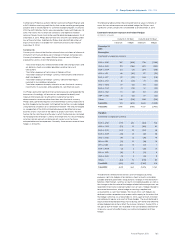

Equity price risk

Equity price risk is the risk that the fair value or future cash flows of a

financial instrument will fluctuate because of changes in equity prices.

Philips is a shareholder in several publicly listed companies, including

Chimei Innolux, Shenyang Neusoft Corporation Ltd, and TPV Technology

Ltd. As a result, Philips is exposed to potential financial loss through

movements in their share prices. The aggregate equity price exposure in its

main available-for-sale financial assets amounted to approximately EUR

65 million at year-end 2013 (2012: EUR 120 million including investments in

associates shares that were sold during 2012) and a further EUR 62 million

that has been reclassified as assets held for sale in relation to the agreed

contribution to the Dutch Pension Fund (please refer to note 36,

Subsequent events). Philips does not hold derivatives in its own stock or in

the above-mentioned listed companies. Philips is also a shareholder in

several privately-owned companies amounting to EUR 50 million. As a

result, Philips is exposed to potential value adjustments.

As part of the sale of shares in NXP to Philips Pension Trustees Limited

there was an arrangement that may entitle Philips to a cash payment from

the UK Pension Fund on or after September 7, 2014 if the value of the NXP

shares has increased by this date to a level in excess of a predetermined

threshold, which at the time of the transaction was substantially above the

transaction price, and the UK Pension Fund is in surplus (on the regulatory

funding basis) on September 7, 2014.

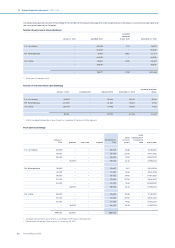

Commodity price risk

Commodity price risk is the risk that the fair value or future cash flows of a

financial instrument will fluctuate because of changes in commodity

prices.

Philips is a purchaser of certain base metals, precious metals and energy.

Philips hedges certain commodity price risks using derivative instruments

to minimize significant, unanticipated earnings fluctuations caused by

commodity price volatility. The commodity price derivatives that Philips

enters into are accounted for as cash flow hedges to oset forecasted

purchases. As of December 2013, a loss of EUR 2.2 million was deferred in

equity as a result of these hedges. A 10% increase in the market price of all

commodities as of December 31, 2013 would increase the fair value of the

derivatives by EUR 1.4 million.

As of December 2012, a loss of EUR 0.3 million was deferred in equity as a

result of these hedges. A 10% increase in the market price of all

commodities as of December 31, 2012 would increase the fair value of the

derivatives by EUR 2 million.

Credit risk

Credit risk represents the loss that would be recognized at the reporting

date, if counterparties failed completely to perform their payment

obligations as contracted. Credit risk is present within Philips trade

receivables. To have better insights into the credit exposures, Philips

performs ongoing evaluations of the financial and non-financial condition

of its customers and adjusts credit limits when appropriate. In instances

where the creditworthiness of a customer is determined not to be

sufficient to grant the credit limit required, there are a number of mitigation

tools that can be utilized to close the gap including reducing payment

terms, cash on delivery, pre-payments and pledges on assets.

Philips invests available cash and cash equivalents with various financial

institutions and is exposed to credit risk with these counterparties. Philips

is also exposed to credit risks in the event of non-performance by financial