Philips 2013 Annual Report Download - page 174

Download and view the complete annual report

Please find page 174 of the 2013 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

31 11 Group financial statements 11.9 - 11.9

174 Annual Report 2013

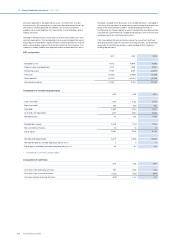

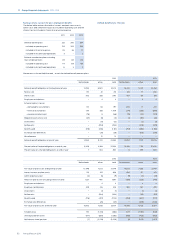

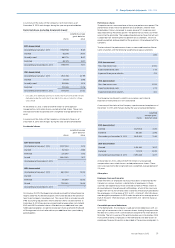

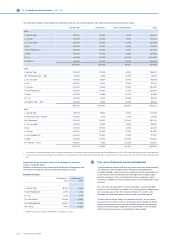

The weighted average assumptions used to calculate the defined benefit

obligations for retiree medical plans as of December 31 were as follows:

2012 2013

Discount rate 4.5% 4.8%

Compensation increase (where applicable) − −

Assumed healthcare cost trend rates at December 31:

2012 2013

Healthcare cost trend rate assumed for next year 7.5% 7.5%

Rate that the cost trend rate will gradually reach 5.2% 5.2%

Year of reaching the rate at which it is assumed to

remain 2019 2019

The average duration of the DBO of the retiree medical plans is 9 years

(2012: 8 years).

Investment policy in our largest pension plans

It must be acknowledged that trustees of the Philips pension plans are

responsible for and have full discretion over the investment strategy of the

plan assets.

The objective of the liability hedging portfolio of the Philips pension plan

in the Netherlands is to match part of the interest rate sensitivity of the

plan’s inflation-linked pension liabilities (based on a 2% inflation

assumption). The liability hedging portfolio is mainly invested in euro-

denominated government bonds, investment grade debt securities and

long-duration interest rate swaps. The size of the liability hedging

portfolio is targeted to be at least 64% of the fair value of the plan’s

inflation-linked pension liabilities. The objective of the return portfolio is

to maximize investment returns within well-specified risk constraints.

The Philips pension plan in the United Kingdom operates a fixed income

portfolio that aims to fully hedge the interest rate and inflation rate

sensitivities of the fair value of the plan’s pension liabilities. Part of the

portfolio is invested in a buy-in policy, in which an insurance company

guarantees all future benefit payments to the plan, thereby matching the

investment and longevity risks of the pension liabilities covered in the

buy-in policy.

The plan assets of the Philips pension plan in the United States are

invested in a well diversified portfolio. The interest rate sensitivity of the

fixed income portfolio is closely aligned to that of the plan’s pension

liabilities. Any contributions from the sponsoring company are used to

further increase the fixed income part of the assets. As part of the

investment strategy, any additional investment returns of the return

portfolio are used to further decrease the interest rate mismatch between

the plan assets and the pension liabilities.

Cash flows and costs in 2014

Philips expects considerable cash outflows in relation to employee

benefits which are estimated to amount to EUR 626 million in 2014,

consisting of EUR 417 million employer contributions to defined benefit

pension plans, EUR 140 million employer contributions to defined

contribution pension plans, EUR 52 million expected cash outflows in

relation to unfunded pension plans and EUR 17 million in relation to

unfunded retiree medical plans. The employer contributions to defined

benefit pension plans are expected to amount to EUR 223 million for the

Netherlands and EUR 194 million for other countries. The Company

continues to fund a part of the existing deficit in the US pension plan in

2014, which amount is included in the amounts aforementioned. For the

funding of the deficit in the US plan the Group adheres to the minimum

funding requirements of the US Pension Protection Act. The UK plan is

currently in a surplus on a regulatory basis and does not require any

funding in 2014 other than the agreed administration cost.

The funding of the pension fund in the Netherlands for 2014 consists of a

fixed percentage of payroll which applies for a period of 5 years. The

additional contribution to the pension fund for the Netherlands is not

included in the above figures. For further details we refer to note 36,

Subsequent events. It is noted that the (majority of the) contribution will

need to be written o through Other comprehensive income due to the

asset ceiling restrictions in the pension plan in the Netherlands.

The service and administration cost for 2014 is expected to amount to EUR

256 million, consisting of EUR 255 million for defined-benefit pension

plans and EUR 1 million for defined-benefit retiree medical plans. The net

interest expense for 2014 is expected to amount to EUR 54 million,

consisting of EUR 43 million for defined-benefit pension plans and EUR 11

million for defined-benefit retiree medical plans. The cost for defined-

contribution pension plans in 2014 is expected to amount to EUR 140

million.

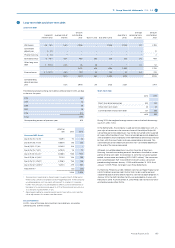

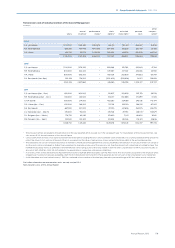

Sensitivity analysis

The table below illustrates the approximate impact on the defined-benefit

obligation if the Company were to change key assumptions. The DBO was

recalculated using a change in the assumptions of 1% which overall is

considered a reasonably possible change. The impact on the DBO

because of changes in discount rate is normally accompanied by

osetting movements in plan assets, especially when using matching

strategies.

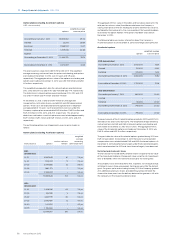

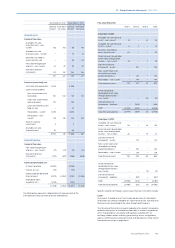

Defined benefit obligation

2013

Pension

Netherlands

Pension

other

Retiree

medical

Increase

Discount rate (1%

movement) (1,708) (822) (12)

Wage increase (1%

movement) 165 28 −

Inflation (1% movement) 979 461 −

Longevity (see explanation) 355 232 7

Medical benefit level (1%

price increase) − − 12

Decrease

Discount rate (1%

movement) 2,158 962 16

Wage increase (1%

movement) (147) (26) −

Inflation (1% movement) (876) (418) −

Longevity also impacts post-employment benefit liabilities. The above

sensitivity table illustrates the impact on the defined-benefit obligation of

a further 10% decrease in the assumed rates of mortality for the

Company’s major schemes. A 10% decrease in assumed mortality rates

equals improvement of life expectancy by 0.5 - 1 year.

Changes in assumed health care cost trend rates can have a significant

eect on the amounts reported for the retiree medical plans. A one

percentage-point increase in medical benefit level is therefore included in

above table as a likely scenario.

Philips Pension Fund in the Netherlands

In relation to the fraud in the Dutch real estate sector uncovered in 2007,

Philips and the Philips Pension Fund in the Netherlands have jointly and

amicably assessed any residual damages in 2013. In view of the new

pension agreement, which includes a new funding structure, eective as of

January 1, 2014, Philips decided to make a special cash contribution in

2013 to ensure that any potential financial issues from the past, including

this real estate fraud, were cleared. As a result of this special contribution

the real estate case has been closed.

31 Share-based compensation

The purpose of the share-based compensation plans is to align the

interests of management with those of shareholders by providing

incentives to improve the Company’s performance on a long-term basis,

thereby increasing shareholder value.

The Company has the following plans:

• options on its common shares;

• rights to receive common shares in the future based on a service

condition (restricted shares);

• rights to receive common shares in the future based on performance

and service conditions (performance shares).