Philips 2013 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2013 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

|

|

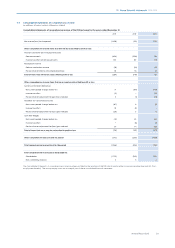

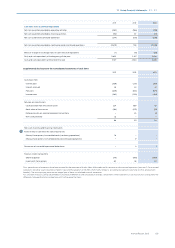

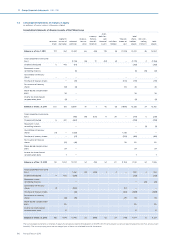

11 Group financial statements 11.9 - 11.9

Annual Report 2013 139

In the event of sale of receivables and factoring, the Company

derecognizes receivables when the Company has given up control or

continuing involvement, which is deemed to have occurred when:

• the Company has transferred its rights to receive cash flows from the

receivables or has assumed an obligation to pay the received cash

flows in full without any material delay to a third party under a ‘pass-

through’ arrangement; and

• either (a) the Company has transferred substantially all of the risks and

rewards of the ownership of the receivables, or (b) the Company has

neither transferred nor retained substantially all of the risks and

rewards, but has transferred control of the assets.

However, in case the Company neither transfers nor retains substantially

all the risks and rewards of ownership of the receivables nor transfers

control of the receivables, the receivable is recognized to the extent of the

Company’s continuing involvement in the assets. In this case, the

Company also recognizes an associated liability. The transferred

receivable and associated liability are measured on a basis that reflects

the rights and obligations that the Company has retained.

Other non-current financial assets

Other non-current financial assets include held-to-maturity investments,

loans and available-for-sale financial assets and financial assets at fair

value through profit or loss.

Held-to-maturity investments are those debt securities which the

Company has the ability and intent to hold until maturity. Held-to-

maturity debt investments are recorded at amortized cost, adjusted for the

amortization or accretion of premiums or discounts using the eective

interest method.

Loans receivable are stated at amortized cost, less impairment.

Available-for-sale financial assets are non-derivative financial assets that

are designated as available-for-sale and that are not classified in any of

the other categories of financial assets. Subsequent to initial recognition,

they are measured at fair value and changes therein, other than

impairment losses and foreign currency dierences on available for sale-

debt instruments are recognized in Other comprehensive income and

presented in the fair value reserve in equity. When an investment is

derecognized, the gain or loss accumulated in equity is reclassified to the

Statement of income.

Available-for-sale financial assets including investments in privately-held

companies that are not associates, and do not have a quoted market price

in an active market and whose fair value could not be reliably determined,

are carried at cost.

A financial asset is classified as fair value through profit or loss if it is

classified as held for trading or is designated as such upon initial

recognition. Financial assets are designated as fair value through profit or

loss if the Company manages such investments and makes purchase and

sale decisions based on their fair value in accordance with the Company-

documented risk management or investment strategy. Attributable

transaction costs are recognized in the Statement of income as incurred.

Financial assets at fair value through profit or loss are measured at fair

value, and changes therein are recognized in profit or loss.

Equity

Common shares are classified as equity. Incremental costs directly

attributable to the issuance of shares are recognized as a deduction from

equity. Where the Company purchases the Company’s equity share

capital (treasury shares), the consideration paid, including any directly

attributable incremental costs (net of income taxes) is deducted from

equity attributable to the Company’s equity holders until the shares are

cancelled or reissued. Where such ordinary shares are subsequently

reissued, any consideration received, net of any directly attributable

incremental transaction costs and the related income tax eects, is

included in equity attributable to the Company’s equity holders.

Dividends are recognized as a liability in the period in which they are

declared. The income tax consequences of dividends are recognized

when a liability to pay the dividend is recognized.

Debt and other liabilities

Debt and liabilities other than provisions are stated at amortized cost.

However, loans that are hedged under a fair value hedge are remeasured

for the changes in the fair value that are attributable to the risk that is being

hedged.

Derivative financial instruments, including hedge accounting

The Company uses derivative financial instruments principally to manage

its foreign currency risks and, to a more limited extent, for managing

interest rate and commodity price risks. All derivative financial instruments

are classified as current assets or liabilities and are accounted for at the

trade date. Embedded derivatives are separated from the host contract

and accounted for separately if the economic characteristics and risks of

the host contract and the embedded derivative are not closely related.

The Company measures all derivative financial instruments at fair value

derived from market prices of the instruments, or calculated as the present

value of the estimated future cash flows based on observable interest

yield curves, basis spread, credit spreads and foreign exchange rates, or

from option pricing models, as appropriate. Gains or losses arising from

changes in fair value of derivatives are recognized in the Statement of

income, except for derivatives that are highly eective and qualify for cash

flow or net investment hedge accounting.

Changes in the fair value of derivatives that are designated and qualify as

fair value hedges are recorded in the Statement of income, together with

any changes in the fair value of the hedged asset or liability that are

attributable to the hedged risk. For interest rate swaps designated as a fair

value hedge of an interest bearing asset or liability that are unwound, the

amount of the fair value adjustment to the asset or liability for the risk

being hedged is released to the Statement of income over the remaining

life of the asset or liability based on the recalculated eective yield.

Changes in the fair value of a derivative that is highly eective and that is

designated and qualifies as a cash flow hedge, are recorded in Other

comprehensive income, until the Statement of income is aected by the

variability in cash flows of the designated hedged item. To the extent that

the hedge is ineective, changes in the fair value are recognized in the

Statement of income.

The Company formally assesses, both at the hedge’s inception and on an

ongoing basis, whether the derivatives that are used in hedging

transactions are highly eective in osetting changes in fair values or cash

flows of hedged items. When it is established that a derivative is not highly

eective as a hedge or that it has ceased to be a highly eective hedge, the

Company discontinues hedge accounting prospectively. When hedge

accounting is discontinued because it is expected that a forecasted

transaction will not occur, the Company continues to carry the derivative

on the Balance sheet at its fair value, and gains and losses that were

accumulated in equity are recognized immediately in the Statement of

income. If there is a delay and it is expected that the transaction will still

occur, the amount in equity remains there until the forecasted transaction

aects income. In all other situations in which hedge accounting is

discontinued, the Company continues to carry the derivative at its fair

value on the Balance sheet, and recognizes any changes in its fair value in

the Statement of income.

Foreign currency dierences arising on the retranslation of financial

instruments designated as a hedge of a net investment in a foreign

operation are recognized directly as a separate component of equity

through Other comprehensive income, to the extent that the hedge is

eective. To the extent that the hedge is ineective, such dierences are

recognized in the Statement of income.

Osetting and master netting agreements

The Company presents financial assets and financial liabilities on a gross

basis as separate line items in the Consolidated balance sheet.

Master netting agreements may be entered into when the Company

undertakes a number of financial instrument transactions with a single

counterparty. Such an agreement provides for a net settlement of all

financial instruments covered by the agreement in the event of default or

certain termination events on any of the transactions. A master netting

agreement may create a right of oset that becomes enforceable and

aects the realization or settlement of individual financial assets and

financial liabilities only following a specified termination event. However,

if this contractual right is subject to certain limitations then it does not

necessarily provide a basis for osetting unless both of the osetting

criteria are met, i.e. there is a legally enforceable right and an intention to

settle net or simultaneously.

Property, plant and equipment

Items of property, plant and equipment are measured at cost less

accumulated depreciation and accumulated impairment losses. The

useful lives and residual values are evaluated annually.