Regions Bank 2009 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2009 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

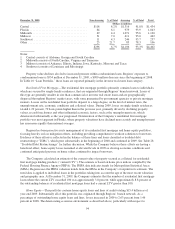

Management Process

Regions employs a credit risk management process with defined policies, accountability and regular

reporting to manage credit risk in the loan portfolio. Credit risk management is guided by credit policies that

provide for a consistent and prudent approach to underwriting and approvals of credits. Within the Credit Policy

department, procedures exist that elevate the approval requirements as credits become larger and more complex.

Generally, consumer credits and smaller commercial credits are centrally underwritten based on custom credit

matrices and policies that are modified as appropriate. Larger commercial and commercial real estate

transactions are individually underwritten, risk-rated, approved and monitored.

Responsibility and accountability for adherence to underwriting policies and accurate risk ratings lies in the

lines of business. For consumer and small business portfolios, the risk management process focuses on managing

customers who become delinquent in their payments and managing performance of the credit scorecards, which

are periodically adjusted based on actual credit performance. Commercial business units are responsible for

underwriting new business and, on an ongoing basis, monitoring the credit of their portfolios, including a

complete review of the borrower semi-annually or more frequently as needed.

To ensure problem commercial credits are identified on a timely basis, several specific portfolio reviews

occur each quarter to assess the larger adversely rated credits for accrual status and, if necessary, to ensure such

individual credits are transferred to Regions’ Special Assets Group, which specializes in managing distressed

credit exposures.

Separate and independent commercial credit and consumer credit risk management organizational groups

exist, which report to the Chief Risk Officer. These organizational units partner with the business line to assist in

the processes described above, including the review and approval of new business and ongoing assessments of

existing loans in the portfolio. Independent commercial and consumer credit risk management provides for more

accurate risk ratings and the timely identification of problem credits, as well as oversight for the Chief Risk

Officer on conditions and trends in the credit portfolios.

Credit quality and trends in the loan portfolio are measured and monitored regularly and detailed reports, by

product, business unit and geography, are reviewed by line of business personnel and the Chief Risk Officer. The

Chief Risk Officer reviews summaries of these credit reports with executive management and the Board of

Directors. Finally, the Credit Review department provides ongoing independent oversight of the credit portfolios

to ensure policies are followed, credits are properly risk-rated and that key credit control processes are

functioning as intended.

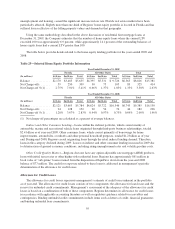

Risk Characteristics of the Loan Portfolio

In order to assess the risk characteristics of the loan portfolio, Regions considers the current U.S. economic

environment and that of its primary banking markets, as well as risk factors within the major categories of loans.

Economic Environment in Regions’ Banking Markets

The largest factor influencing the credit performance of Regions’ loan portfolio is the overall economic

environment in the U.S. and the primary markets in which it operates. The recession that began in late 2007

continued through 2008 and into 2009. Through this recessionary period, the overall output of goods and services

experienced its sharpest decline since the early 1980s. Consumer spending, approximately two-thirds of all

recorded spending, has been adversely impacted by declining inflation-adjusted income, low additional credit

capacity, historically high required monthly debt payments, a negative employment outlook and historically low

consumer confidence. The business sector continues to struggle with weak domestic and foreign demand, and

underutilized operating capacity.

90