Regions Bank 2009 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2009 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

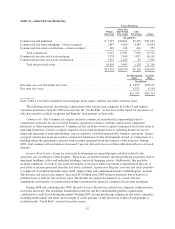

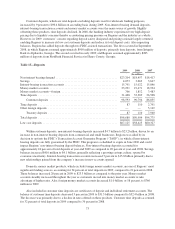

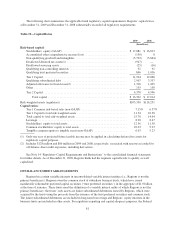

Customer deposits, which are total deposits excluding deposits used for wholesale funding purposes,

increased by 9 percent to $98.6 billion on an ending basis during 2009. Non-interest bearing demand deposits,

interest-bearing transaction accounts and money market accounts were the main source of growth. Slightly

offsetting these products, time deposits declined. In 2008, the banking industry experienced very high deposit

pricing due to liquidity concerns thereby accentuating pricing pressure on Regions and the industry as a whole.

However, in 2009, customers’ concern regarding deposit safety dissipated and pricing rationale largely returned,

enabling Regions to increase its low cost customer deposits and reduce its total deposit costs. Also impacting

balances, Regions has added deposits through two FDIC-assisted transactions. The first occurred in September

2008, in which Regions assumed approximately $900 million of deposits, primarily time deposits, from Integrity

Bank in Alpharetta, Georgia. The second occurred in early 2009, and Regions assumed approximately $285

million of deposits from FirstBank Financial Services in Henry County, Georgia.

Table 15—Deposits

2009 2008 2007

(In millions)

Non-interest bearing demand .......................................... $23,204 $18,457 $18,417

Savings ........................................................... 4,073 3,663 3,647

Interest-bearing transaction accounts .................................... 15,791 15,022 15,846

Money market accounts .............................................. 23,291 19,471 18,934

Money market accounts—foreign ...................................... 766 1,812 3,483

Time deposits ...................................................... 31,468 32,369 26,508

Customer deposits .............................................. 98,593 90,794 86,835

Time deposits ...................................................... 87 110 2,791

Other foreign deposits ............................................... — — 5,149

Treasury deposits ............................................... 87 110 7,940

Total deposits ...................................................... $98,680 $90,904 $94,775

Low cost deposits ................................................... $67,125 $58,425 $60,327

Within customer deposits, non-interest-bearing deposits increased $4.7 billion to $23.2 billion, driven by an

increase in non-interest bearing deposits from commercial and small businesses. Regions was aided by its

decision to opt into the FDIC’s Transaction Account Guarantee Program (“TAGP”), in which all non-interest

bearing deposits are fully guaranteed by the FDIC. This program is scheduled to expire in June 2010 and could

impact Regions’ non-interest bearing deposit balances. Non-interest-bearing deposits accounted for

approximately 24 percent of total deposits at year-end 2009 as compared to 20 percent at year-end 2008. Savings

balances increased $410 million to $4.1 billion, generally reflecting a growing savings culture, spurred by

economic uncertainty. Interest-bearing transaction accounts increased 5 percent to $15.8 billion primarily due to

new relationships gained from the company’s increase in new accounts opened.

Domestic money market products, which exclude foreign money market accounts, are one of Regions’ most

significant funding sources, accounting for 24 percent of total deposits in 2009, compared to 21 percent in 2008.

These balances increased 20 percent in 2009 to $23.3 billion as compared to the prior year. Money market

accounts steadily increased throughout the year as customers moved into money market accounts to take

advantage of higher rates. Also, foreign money market accounts decreased $1.0 billion, or 58 percent, to $766

million in 2009.

Also included in customer time deposits are certificates of deposit and individual retirement accounts. The

balance of customer time deposits decreased 3 percent in 2009 to $31.5 billion compared to $32.4 billion in 2008.

The decrease was primarily due to a decline in rates offered on these products. Customer time deposits accounted

for 32 percent of total deposits in 2009 compared to 36 percent in 2008.

73