Regions Bank 2009 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2009 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

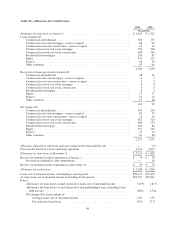

Mortgage servicing rights impairment increased $79 million to $85 million in 2008. The increase was driven

by the effects of changes in the interest rate environment.

FDIC premiums increased $4 million to $15 million in 2008. The increase was driven by a higher insured

deposit base.

Other miscellaneous expenses remained relatively steady, decreasing $4 million to $988 million in 2008;

however, excluding merger charges of $38 million in 2008 and $76 million in 2007, other miscellaneous

expenses increased 4 percent. Included in other miscellaneous expenses were $49 million and $39 million in

write-downs on the investment in two Morgan Keegan mutual funds during 2008 and 2007, respectively. Also in

2008, Regions incurred a $65 million loss on early extinguishment of debt related to the redemption of

subordinated notes. Other miscellaneous expenses benefited from the recognition of a $28 million litigation

expense reduction related to Visa’s IPO in early 2008. Regions had recorded a $52 million expense for Visa

litigation in 2007.

Regions’ 2008 provision for income taxes from continuing operations decreased $994 million to a tax

benefit of $348 million compared to expense of $646 million in 2007, primarily due to lower consolidated

earnings combined with a $275 million benefit from settlement of uncertain tax positions resulting from

resolution with the IRS of the Company’s federal uncertain tax positions for tax years 1999-2006. Therefore,

Regions’ effective tax rate from continuing operations was 5.9 percent in 2008 compared to 31.7 percent in 2007.

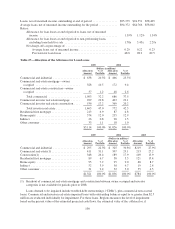

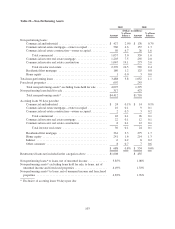

At December 31, 2008, non-performing assets totaled $1.7 billion, or 1.76 percent of ending loans,

compared to $864 million, or 0.90 percent of loans, at December 31, 2007. Non-performing assets, excluding

loans held for sale, increased $431 million to $1.3 billion, or 1.33 percent, compared to $864 million, or 0.90

percent in 2007. The increase in non-performing assets was primarily driven by construction and commercial real

estate loans, including the residential homebuilder portfolio, due to the widespread decline in residential property

values. During 2008, Regions disposed of or designated as held for sale approximately $1.6 billion of loans and

foreclosed properties, partially offsetting the otherwise higher level of non-performing assets.

During 2008, the provision for loan losses from continuing operations was $2.1 billion and net charge-offs

were $1.5 billion. This compares to a provision for loan losses from continuing operations of $555 million and

net charge-offs of $271 million in 2007. Net charge-offs as a percent of average loans were 1.59 percent in 2008

compared to 0.29 percent in 2007. The significant increase in the provision and net charge-offs in 2008 is related

to losses on non-performing loans sold or moved to held for sale. In 2008, these losses accounted for $639

million of the increase in the net charge-offs. The remaining increase in the loan loss provision was primarily due

to an increase in management’s estimate of losses inherent in its residential homebuilder, condominium, home

equity and residential mortgage portfolios, all of which are closely tied to the housing market slowdown. Losses

were also impacted by the disposition of problem loans, as well as generally weaker economic conditions in the

broader economy.

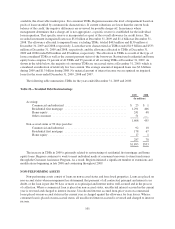

At December 31, 2008, the allowance for credit losses totaled $1.9 billion or 1.95 percent of total loans, net

of unearned income compared to $1.4 billion or 1.45 percent at year-end 2007. The increase in the allowance for

credit loss ratio reflects management’s estimate of the level of inherent losses in the portfolio, which

management believes increased during 2008 due to a slowing economy and a weakening housing market. The

increase in non-performing assets, driven largely by residential homebuilder and condominium loans, was a key

determining dynamic in the assessment of inherent losses and, as a result, was an important factor in determining

the allowance level. Deterioration of the Company’s home equity and residential first mortgage portfolios,

especially Florida-based credits, was also a factor.

108