Regions Bank 2009 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2009 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

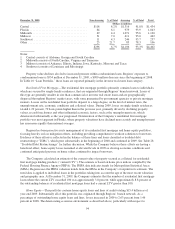

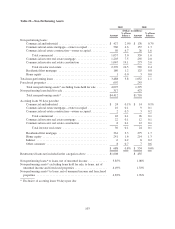

Net charge-offs on home equity rose to 2.63 percent in 2009 versus 1.46 percent in 2008. Losses from

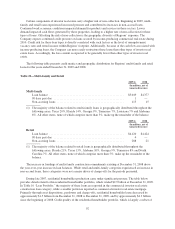

Florida-based credits were again particularly high, as property valuations in certain markets continued to

experience deterioration. These loans and lines represent approximately $5.7 billion of Regions’ total home

equity portfolio at December 31, 2009. Of that balance, approximately $2.2 billion represents first liens; second

liens, which total $3.5 billion, were the main source of losses. Florida second lien losses were 7.01 percent in

2009. Total home equity losses in Florida amounted to 5.41 percent of loans and lines versus 1.05 percent across

the remainder of Regions’ footprint in 2009.

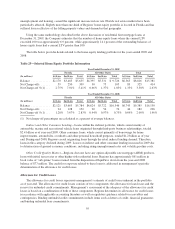

The Company has taken a number of measures to manage the portfolios and mitigate losses, such as

accelerated asset disposition. These strategies have been pursued in the more problematic portfolios, including

the residential homebuilder portfolio, a subset of the commercial investor real estate mortgage and commercial

investor real estate construction loan portfolios, Significant action in the management of the home equity

portfolio has also been taken. The Company has a strong Customer Assistance Program in place, designed to

educate customers about their loans and, as necessary, discuss options and solutions. During 2009, Regions

began to experience deteriorating trends and credit pressure in income-producing commercial real estate loans,

including multi-family and retail. Because of the cash flow associated with the income-producing credits, the

Company can typically more easily restructure these loans. Accordingly, the loss content is expected to be

generally lower than other types of investor real estate loans, such as residential homebuilder loans.

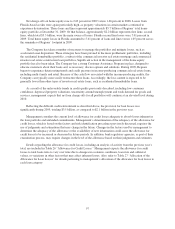

As a result of the unfavorable trends in credit quality previously described, including low consumer

confidence, depressed property valuations, uncertainty around unemployment and weak demand for goods and

services, management expects that net loan charge-offs for all portfolios will continue at an elevated level during

2010.

Reflecting the difficult credit environment as described above, the provision for loan losses rose

significantly during 2009, totaling $3.5 billion, as compared to $2.1 billion in the previous year.

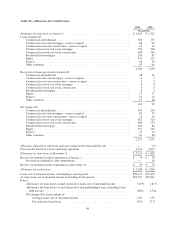

Management considers the current level of allowance for credit losses adequate to absorb losses inherent in

the loan portfolio and unfunded commitments. Management’s determination of the adequacy of the allowance for

credit losses, which is based on the factors and risk identification procedures previously discussed, requires the

use of judgments and estimations that may change in the future. Changes in the factors used by management to

determine the adequacy of the allowance or the availability of new information could cause the allowance for

credit losses to be increased or decreased in future periods. In addition, bank regulatory agencies, as part of their

examination process, may require changes in the level of the allowance based on their judgments and estimates.

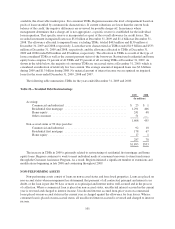

Details regarding the allowance for credit losses, including an analysis of activity from the previous year’s

total, are included in Table 26 “Allowance for Credit Losses.” Management expects the allowance for credit

losses to total loans ratio to vary over time due to changes in economic conditions, loan mix and collateral

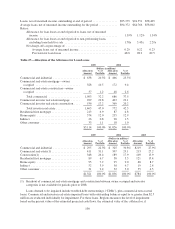

values, or variations in other factors that may affect inherent losses. Also, refer to Table 27 “Allocation of the

Allowance for Loan Losses” for details pertaining to management’s allocation of the allowance for loan losses to

each loan category.

97