Regions Bank 2009 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2009 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

borrowers may repay their loans or securities earlier than at their stated maturities. Liquidity risk relates to

Regions’ ability to fund present and future obligations. The Company, through Morgan Keegan, is also subject to

various market-related risks associated with its brokerage and market-related activities. Counterparty risk

represents the risk that a counterparty will not comply with its contractual obligations.

Management follows a formal policy to evaluate and document the key risks facing each line of business,

how those risks can be controlled or mitigated, and how management monitors the controls to ensure that they

are effective. Separate from risk acceptance, the Chief Risk Officer (CRO) oversees an independent risk

assessment and reporting program. To ensure that risks within the company are presented and appropriately

addressed, the Board has designated a Risk Committee of outside directors. The Risk Committee’s focus is on

Regions’ overall risk profile and the CRO reports to this committee quarterly. Additionally, Regions’ Internal

Audit Division performs ongoing, independent reviews of the risk management process which are reported to the

Audit Committee of the Board of Directors.

Some of the more significant processes used to manage and control these and other risks are described in the

remainder of this report. External factors beyond management’s control may result in losses despite risk

management efforts.

INTEREST RATE RISK

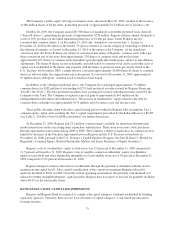

Regions’ primary market risk is interest rate risk, including uncertainty with respect to absolute interest rate

levels as well as uncertainty with respect to relative interest rate levels, which is impacted by both the shape and

the slope of the various yield curves that affect the financial products and services that the Company offers. To

quantify this risk, Regions measures the change in its net interest income in various interest rate scenarios

compared to a base case scenario. Net interest income sensitivity is a useful short-term indicator of Regions’

interest rate risk.

Sensitivity Measurement—Financial simulation models are Regions’ primary tools used to measure interest

rate exposure. Using a wide range of sophisticated simulation techniques provides management with extensive

information on the potential impact to net interest income caused by changes in interest rates. Models are

structured to simulate cash flows and accrual characteristics of Regions’ balance sheet. Assumptions are made

about the direction and volatility of interest rates, the slope of the yield curve, and the changing composition of

the balance sheet that result from both strategic plans and from customer behavior. Among the assumptions are

expectations of balance sheet growth and composition, the pricing and maturity characteristics of existing

business and the characteristics of future business. Interest rate-related risks are expressly considered, such as

pricing spreads, the lag time in pricing administered rate accounts, prepayments and other option risks. Regions

considers these factors, as well as the degree of certainty or uncertainty surrounding their future behavior.

Historically, Regions’ balance sheet has consisted of a relatively rate-sensitive deposit base that funds a

predominantly floating rate commercial and consumer loan portfolio. This mix of Regions’ core business

activities creates a naturally asset sensitive balance sheet, meaning that increases (decreases) in interest rates

would likely have a positive (negative) cumulative impact on Regions’ net interest income. To manage the

balance sheet’s interest rate risk, Regions maintains a portfolio of largely fixed-rate discretionary investments,

loans and derivatives. The market risk of these discretionary instruments attributable to variation in interest rates

is fully incorporated into the simulation results in the same manner as all other balance sheet instruments.

The primary objective of asset/liability management at Regions is to coordinate balance sheet composition

with interest rate risk management to sustain a reasonable and stable net interest income throughout various

interest rate cycles. In computing interest rate sensitivity for measurement, Regions compares a set of alternative

interest rate scenarios to the results of a base case scenario based on “market forward rates.” The standard set of

interest rate scenarios includes the traditional instantaneous parallel rate shifts of plus 100, 200 and 300 basis

points. Regions also prepares a minus 100 basis points scenario; a minus 200 basis point scenario is not

considered realistic in the current rate environment. Up-rate scenarios of greater magnitude are also analyzed,

83